Student reviewing tuition bills and student loan documents at a desk

What Is a Student Loan and How Does It Work

Content

College costs have skyrocketed. A degree that your parents might have funded with a summer job now requires most families to take on significant debt. Student loans fill this financial gap for over 43 million Americans, but signing those documents without understanding the fine print can lock you into payment plans that strain your budget for decades.

Student Loan Meaning and Purpose

Think of a student loan as money you borrow specifically for education expenses—everything from tuition bills to textbooks, dorm fees to off-campus rent. Here's the catch that separates loans from scholarships: you're paying back every penny, plus interest charges that start adding up faster than you might expect.

When students borrow for college, they're betting on their future. The logic makes sense on paper: invest in education now, earn more later, pay off the debt from that higher income. But the numbers get real quickly. In-state public universities average $28,000 per year in 2026, while private colleges can hit $60,000 or more. Few families can write those checks from their checking account.

Three elements form the backbone of every student loan. You've got the principal—that's the actual cash you receive for school. Then there's interest, which is basically the lender's fee for letting you use their money, calculated as a percentage that compounds daily. Finally, you've got your repayment timeline, usually spanning a decade to a quarter-century based on which payment plan you pick.

Here's a real-world scenario: borrow $35,000 at 5% interest on a 10-year plan. Your monthly bill? About $371. Total paid by the end? Roughly $44,500. You just spent $9,500 on interest alone—money that bought you nothing except the privilege of borrowing.

Author: Brandon Ellery;

Source: nayiyojna.com

How Student Loans Work

You'll apply for loans before each school year starts, requesting whatever amount your budget requires for that period. Schools don't hand you a check—they receive funds directly through disbursement, splitting it between terms. Your college grabs what you owe for tuition and mandatory fees first, then passes along anything left over for your rent, food, and other costs.

Most federal loans (and plenty of private ones) give you a grace period. That's typically six months after you graduate or drop below half-time student status before bills start arriving. It's meant to let you land a job and get your first few paychecks before payments kick in.

Here's what trips up countless borrowers: interest doesn't wait for graduation. On unsubsidized federal loans and nearly every private loan, interest starts piling up the instant money hits your school's account. You're still pulling all-nighters studying, but your loan balance is growing. When repayment starts, that accumulated interest gets capitalized—fancy term for adding it to what you owe. Now you're paying interest on interest. Take $20,000 borrowed as a freshman. By graduation four years later, you could be looking at $24,000 before making a single payment.

Loan servicers handle the nuts and bolts after you borrow. They send bills, process what you pay, answer your panicked calls, and manage requests to change payment plans. For federal loans, the Department of Education contracts with several servicing companies. Private lenders either manage their own servicing or hire outside firms. Don't be shocked if your servicer switches midstream—happens all the time and doesn't change your actual loan terms, just who you're mailing payments to.

Author: Brandon Ellery;

Source: nayiyojna.com

Federal vs Private Student Loans

Federal versus private student loans? This choice shapes everything about your borrowing experience, from your application to your last payment years down the road.

Federal loans come from the U.S. Department of Education with terms Congress sets. You'll need to complete the FAFSA, but most undergrads don't face credit checks or income requirements. Interest rates get fixed by federal law each year and apply equally to everyone borrowing during that period. For 2025-2026, undergraduates are looking at 5.50% on direct subsidized and unsubsidized loans.

Private loans flow from banks, credit unions, and online lenders competing in the open market. Your credit score (or more likely, your cosigner's score) determines whether you're approved and what rate you'll pay. Rates swing wildly from about 4% to 14% in 2026 depending on creditworthiness and market conditions. You can pick fixed or variable rates—variable might start lower but could climb over time.

Check out these critical differences:

| Feature | Federal Student Loans | Private Student Loans |

| Interest Rates | Fixed by Congress annually (5.50% for undergrads in 2025-26) | Market-based rates from 4-14%; varies with credit scores |

| Credit Check | None for most undergraduate borrowers | Always required; strong credit or cosigner essential |

| Repayment Options | Income-driven plans, extended terms, multiple flexible choices | Standard 10-15 year plans; flexibility varies dramatically by lender |

| Borrower Protections | Extensive deferment, forbearance, discharge provisions | Limited protection; depends entirely on individual lender policies |

| Cosigner Requirements | Never needed | Usually mandatory for students with limited credit history |

| Loan Forgiveness Eligibility | Multiple programs including Public Service Loan Forgiveness | No forgiveness programs available |

Federal Student Loan Types

Direct Subsidized Loans go to undergraduates who demonstrate financial need. The big perk? The government covers your interest while you're in school at least half-time, during your grace period, and if you qualify for deferment later. You can borrow $3,500 to $5,500 yearly depending on your class standing, maxing out at $23,000 total for dependent undergrads.

Direct Unsubsidized Loans skip the financial need requirement. Undergrads and graduate students both qualify. Interest starts accruing immediately, no breaks. Graduate students can borrow up to $20,500 per year, with lifetime limits hitting $57,500 for undergrads and $138,500 for graduate or professional students (that second number includes any undergrad loans).

Direct PLUS Loans target two groups: graduate students and parents of dependent undergraduates. You'll face a credit check, though the standards aren't as strict as private lenders demand. Borrowing caps? The full cost of attendance minus whatever other aid you're receiving. The 2025-2026 PLUS loan rate sits at 8.05%.

Author: Brandon Ellery;

Source: nayiyojna.com

Private Student Loan Features

Private lenders step in when federal loans don't cover your full costs or when you've hit federal borrowing limits. They advertise lower rates than federal options, but that's only true for borrowers with exceptional credit—typically scores above 750.

Most private loans demand immediate repayment or payments while you're still enrolled. Many lenders offer interest-only or deferred options during school, but you'll pay extra for that flexibility. Federal loans come standardized. Private loans? Terms bounce all over the map depending on your lender. Some throw in unemployment protection or let your cosigner off the hook after consecutive on-time payments. Others offer zero flexibility.

Student Loan Repayment Basics

Six months after you graduate, leave school, or drop below half-time enrollment, repayment begins. Federal loans automatically drop you into a standard 10-year plan unless you actively select something different. That plan spreads identical payments across 120 months, structured to eliminate your debt completely within ten years.

Income-driven plans flip the script—your monthly bill depends on what you earn and your family size, not your total debt. Federal borrowers can choose from four major programs: Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR). Your payments typically run 10% to 20% of discretionary income. Whatever balance remains after 20 or 25 years of qualifying payments gets wiped clean. The painful surprise: that forgiven amount might count as taxable income, potentially sticking you with a massive tax bill.

Deferment and forbearance both pause your payments temporarily, but the differences matter. Deferment stops payments and, for subsidized loans, prevents interest from growing. Common reasons include unemployment, economic hardship, or enrolling in graduate programs. Forbearance also halts payments but interest keeps accumulating on every loan type. Lenders approve forbearance more easily than deferment, yet the long-term cost runs higher because that unpaid interest eventually gets added to your principal.

The biggest mistake I see borrowers make is treating student loans like an abstract problem they'll deal with laterюUnderstanding your repayment options before that first bill arrives—and choosing the right plan for your career trajectory—can save tens of thousands of dollars over the life of your loans

— Michael Chen

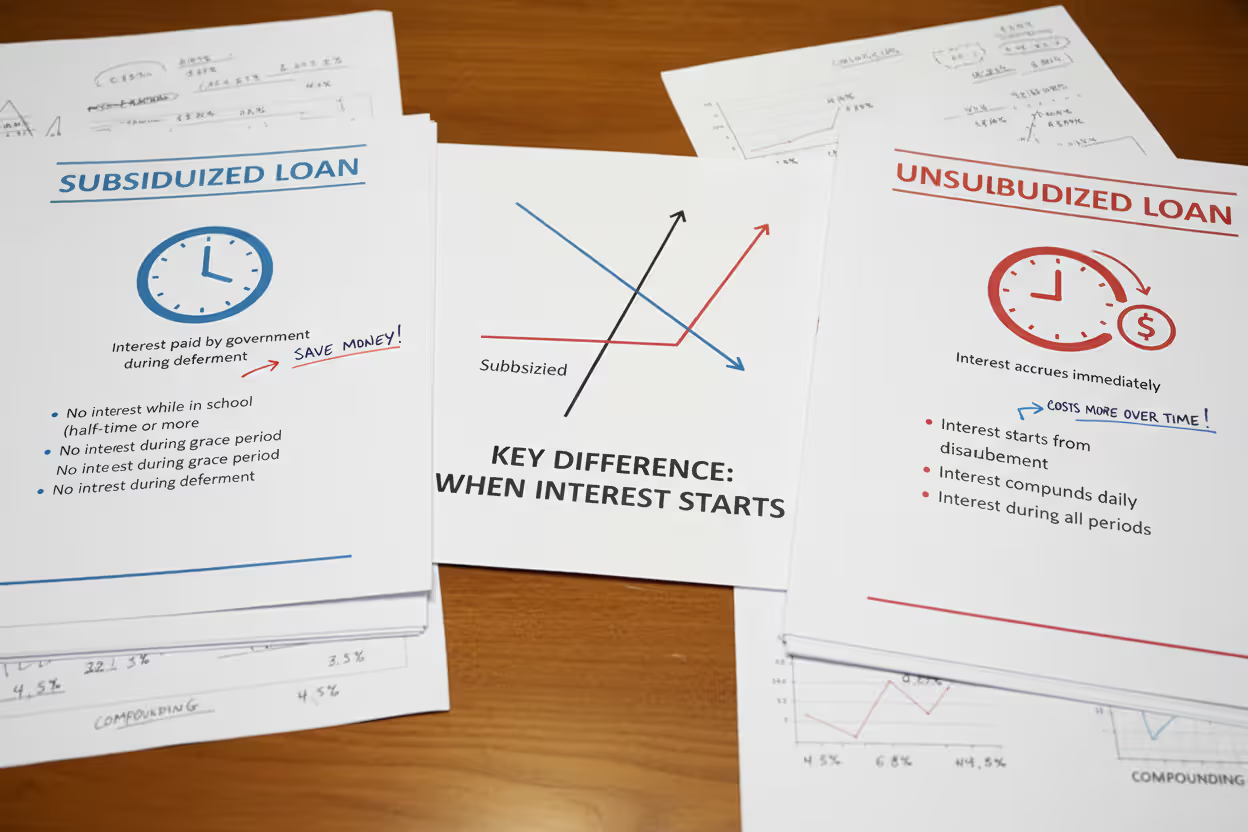

Key Differences Between Subsidized and Unsubsidized Loans

Subsidized versus unsubsidized matters exclusively for federal Direct Loans, and the financial gap between them adds up fast. With subsidized loans, the government picks up your interest tab during specific windows: while you're enrolled at least half-time, throughout your six-month grace period, and during any approved deferment. For a typical four-year degree, this benefit alone can save thousands.

Qualifying for subsidized loans requires showing financial need through the FAFSA. Your school compares what your family can reasonably contribute to their total cost of attendance. Only undergraduates get subsidized loans—graduate and professional students are stuck with unsubsidized federal options exclusively.

Subsidized borrowing caps run lower than unsubsidized limits. First-year dependent undergrads max out at $3,500 in subsidized loans but can borrow $5,500 total combining both subsidized and unsubsidized. By senior year, your subsidized limit reaches just $5,500 annually. Most students burn through subsidized eligibility and lean on unsubsidized loans for additional federal borrowing.

Interest timing creates wildly different total costs. Borrow $15,000 in subsidized loans across four years of college, and you owe exactly $15,000 when repayment starts. That identical amount in unsubsidized loans at 5.50% interest balloons to roughly $18,200 by graduation if you made no payments during school. That's a $3,200 penalty before you've even begun chipping away at principal.

Author: Brandon Ellery;

Source: nayiyojna.com

Common Student Loan Mistakes to Avoid

Overborrowing tops the list of destructive mistakes. Students accept whatever loan amount gets offered without calculating actual need or thinking through future payment obligations. Try this guideline: your total student debt at graduation shouldn't exceed what you expect to earn in your first year working. Planning to teach with a $45,000 starting salary? Think hard before accumulating $80,000 in loans.

Ignoring loan terms until bills start showing up leaves you unprepared and eliminates options. Actually read your Master Promissory Note. Know your interest rate, whether it's locked or variable, who's servicing your loan, and which repayment plans you can access. This information should directly influence whether you borrow more in following years.

Missing payments unleashes consequences that cascade fast. Federal loans hit delinquent status after one skipped payment and default after 270 days of non-payment. Default obliterates your credit score, triggers wage garnishment, lets the government seize tax refunds, and eliminates your eligibility for deferment, forbearance, and income-driven plans. Private loans default even faster, often at just 90 days.

Skipping federal options and jumping straight to private loans costs you access to vastly superior protections and flexibility. Always max out federal loans before even considering private alternatives. Income-driven repayment, Public Service Loan Forgiveness potential, and more generous deferment options exist only through federal programs—you'll find no equivalent safety net with private loans.

Refusing to communicate with servicers when trouble hits makes problems exponentially worse. Struggling financially? Call your servicer immediately to discuss options. They can walk you through deferment and forbearance, help you switch repayment plans, or adjust your payment due date. Ignoring the situation guarantees outcomes worse than any solution they could offer.

Author: Brandon Ellery;

Source: nayiyojna.com

Frequently Asked Questions About Student Loans

Student loans unlock access to higher education, but they demand careful thought and strategic planning. How much you borrow, which loan types you accept, and how you manage repayment will ripple through your financial life for years or potentially decades.

Start by slashing the amount you need to borrow. Choose a less expensive school, work part-time during semesters, hunt aggressively for scholarships, or knock out general education requirements at community college before transferring. Every dollar you avoid borrowing saves roughly $1.30 in total repayment over a 10-year term at typical interest rates.

Make federal loans your priority over private options for their superior flexibility and protections. Within federal loans, grab subsidized loans first, then unsubsidized, and consider PLUS loans only when absolutely necessary. Track your cumulative borrowing across all school years and compare it realistically to entry-level salaries in your chosen field.

Stay organized throughout the process. Keep copies of every promissory note, know your servicers, understand your grace periods, and calendar when repayment begins. Create a login for the National Student Loan Data System (NSLDS) to view all your federal loans in one centralized place.

Student debt affects millions of Americans, but informed borrowers who truly understand their loans, explore all repayment options, and communicate proactively with servicers navigate this challenge far more successfully than those who sign documents without reading them or toss statements in a drawer until problems spiral out of control. Your education represents an investment in your future—make certain the debt you take on to fund it supports rather than sabotages that goal.