Small business owner reviewing loan application documents at office desk

Business Loan Requirements Guide

Content

Getting money for your business isn't about filling out forms and hoping for the best. Last month, I watched a friend submit his third loan application—each time missing critical documents, each time getting rejected. He finally succeeded on attempt four, but only after spending six months fixing problems he could've addressed upfront.

Here's what nobody tells you: having one spectacular number doesn't fix everything else. Your company might pull in $80,000 every month like clockwork, but show up without three years of tax returns and you're walking out empty-handed. Or maybe your personal credit score sits at 790—sounds perfect, right?—except your business opened last Tuesday. Banks don't care about your best qualities when the fundamentals aren't there.

You need everything lined up before you walk through that door.

What Lenders Look for When Evaluating Business Loans

Banks use something they call the Five Cs. Think of it as their checklist for deciding whether you're getting funded or getting ignored.

Author: Matthew Redford;

Source: nayiyojna.com

Capacity means proving your business makes enough to pay them back without choking your operations. They'll dig through your cash flow statements looking for breathing room. Here's their magic number: 1.25 times your proposed payment. If you're borrowing money requiring $4,000 monthly payments, they want to see at least $5,000 available after covering everything else. Anything less and you're cutting things too close.

Capital shows them how much of your own money you've put at risk. Invested $80,000 of personal savings into your restaurant? That matters. It tells them you won't disappear when business gets tough—you've got too much to lose. Traditional banks want to see owners personally funding at least 10-20% of what the business is worth.

Collateral gives banks something to grab if things go wrong. Your warehouse, delivery trucks, even those unpaid customer invoices—all potential security. Don't expect them to lend against full value, though. Most institutions will only advance 70-80% of what your assets are actually worth.

Conditions covers why you need the money and whether your industry is currently thriving or dying. Buying a $150,000 commercial oven that holds its value? Much different than asking for cash to cover "general expenses" you can't specify. Timing matters too—try getting restaurant funding during 2020 lockdowns versus applying today. Completely different worlds.

Character is them investigating whether you're trustworthy. Ever successfully paid off a loan before? Any bankruptcies hiding in your past? Currently fighting lawsuits? Owe back taxes to the IRS? They'll find it all.

Business owners walk in here constantly thinking their 780 credit score erases twelve months of declining sales. It absolutely does not work that way. We need strength across multiple categories. Your one amazing metric can't carry fundamental problems everywhere else

— Sarah Mitchell

Banks also want to see you've actually thought this through. Tell a loan officer you need money for "working capital" and watch their eyes glaze over. Instead, say something like: "We're buying two cargo vans at $38,000 each to expand our delivery range by fifty miles, and our demographic research shows that area should generate another $9,000 monthly"—that gets their attention.

Time in Business and Revenue Requirements

New businesses scare lenders, and the statistics back them up—lots of startups never make it past year two. Your operating history proves you've figured out how to survive.

Traditional banks want at least two years of operations on your record, preferably three. They need multiple years of filed tax returns showing steady or growing performance. These institutions like predictability—they fund businesses with established patterns.

SBA loans include government backing, but don't mistake that for easy approval. Their popular 7(a) program technically accepts businesses operating just one year, assuming you bring serious industry expertise. But "operational" means actually making sales and serving customers, not just filing incorporation papers and ordering business cards.

Online lenders operate differently. Some will work with six-month-old businesses. Certain revenue-based financing companies even fund three-month-old operations, provided your monthly sales look strong and consistent.

Here's how minimum standards compare:

| Who's Lending | How Long You've Operated | Minimum Annual Sales | Personal Credit Score |

| Traditional Banks | 2-3 years | $250,000-$500,000 | 680-700+ |

| SBA 7(a) Programs | 1-2 years | $100,000-$250,000 | 640-680 |

| Online Lenders | 6-12 months | $50,000-$100,000 | 600-650 |

| Alternative Financing | 3-6 months | $25,000-$50,000 | 550-600 |

Revenue thresholds shift dramatically depending on who you're asking and how much you want. Traditional banks extending $400,000 term loans typically want annual sales hitting at least $800,000—they're looking for roughly a 2:1 ratio.

For younger companies, your monthly revenue pattern matters more than your annual total. A business running nine months with steady $25,000 monthly deposits looks way better than one bouncing between $3,000 and $60,000 each month. Unpredictability keeps lenders up at night.

Revenue alone isn't enough—they care whether you're actually making money. Generating $600,000 in annual sales while bleeding cash every quarter raises major questions about whether you'll survive long-term. Banks want positive profits or at minimum, a realistic plan showing when you'll get there.

Seasonal businesses face extra challenges. Take a landscaping company earning eighty percent of yearly revenue between April and October. Lenders familiar with seasonal patterns will account for these cycles, but you'll need enough cash reserves to cover loan payments during your slow winter months.

Author: Matthew Redford;

Source: nayiyojna.com

Credit Score and Financial Health Factors

Credit scores give lenders a quick snapshot of your financial responsibility. They'll check both personal and business credit, though for small companies and startups, your personal score dominates everything.

Traditional banks typically won't consider personal credit scores below 680. SBA programs might accept 640, especially when you've got strong revenue, solid collateral, or deep industry experience. Online lenders occasionally approve scores from 550-600, but fair warning—interest rates explode when scores drop below 650.

Business credit uses different scoring models than personal credit. Dun & Bradstreet scores run from 1 to 100, with anything above 80 considered excellent. Experian's business system also spans 1 to 100. Equifax uses a 101-992 scale. Many small businesses barely exist in business credit systems, which explains why lenders emphasize personal scores for companies under five years old.

Looking at credit factors for business borrowing goes beyond simple score numbers. Banks calculate something called your debt-to-income ratio—they add every monthly debt payment you make, then divide that by your gross monthly income. Traditional lenders prefer seeing results under 36%. Some online lenders will tolerate 50% when cash flow looks robust.

Your existing debt load significantly impacts decisions. Already carrying substantial obligations? Lenders question whether you can handle another payment. They'll examine current loan balances, credit card debt, active credit lines, equipment leases—every financial commitment on your books. Some lenders enforce hard limits, like automatically rejecting any applicant already carrying more than $150,000 in total debt regardless of revenue.

Personal finances enter the equation because lenders typically require personal guarantees from business owners, making your individual assets and liabilities relevant to business lending decisions. Recent bankruptcies, foreclosures, or major tax liens severely hurt approval odds. Most lenders prefer seeing at least two to three years of clean financial history since any serious credit incident.

Cash reserves provide essential cushioning. Lenders prefer businesses maintaining three to six months of operating expenses in accessible accounts. This shows you can weather temporary revenue disruptions without defaulting.

To figure out your payment capacity, lenders use a formula: take your net operating income and divide it by your total debt service requirements. A result of 1.0 means you're generating exactly enough to meet obligations—which banks consider inadequate. They want 1.25 or higher, providing a 25% safety margin.

Documents Needed to Apply for a Business Loan

Documentation requirements shift based on lender type and loan size, but expect to provide extensive financial records. Incomplete applications either sit forever or get rejected immediately—gather everything before starting.

Author: Matthew Redford;

Source: nayiyojna.com

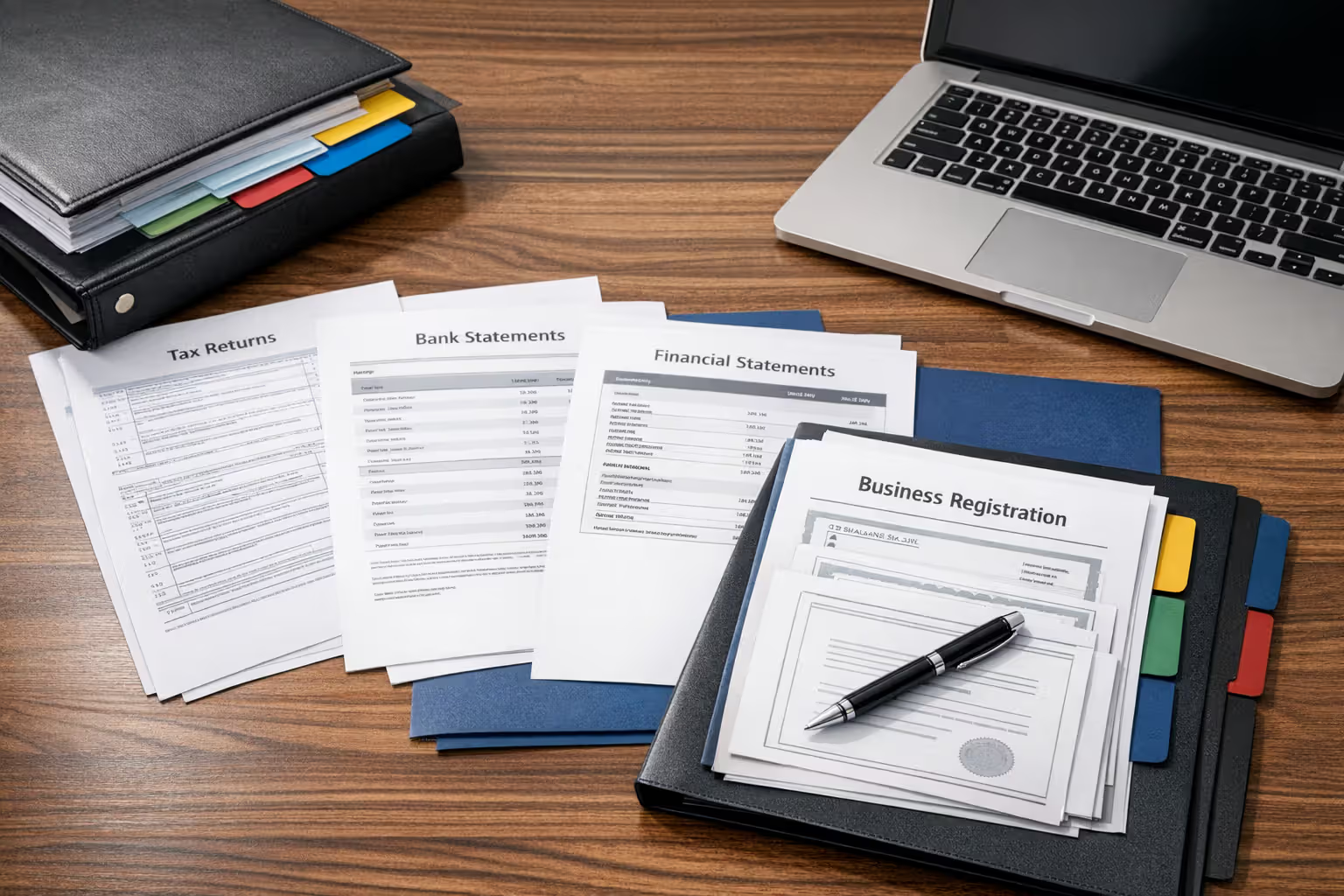

Business tax returns covering the previous 2-3 years show revenue trends and profitability patterns. Lenders want seeing consistent or growing income. If last year's results dropped significantly compared to prior years, prepare a written explanation covering what happened and your corrective actions.

Personal tax returns for any owner controlling 20% or more of the business need to span that same 2-3 year window. Lenders compare personal income against business distributions, making sure you're taking reasonable owner compensation.

Bank statements covering the most recent 3-6 months reveal cash flow patterns and account management. Lenders scan for consistent deposits, adequate balances, absence of frequent overdrafts or bounced check fees. Some online lenders build entire decisions around bank statement analysis, studying daily balances and transaction patterns rather than obsessing over credit scores.

Profit and loss statements detail revenue sources and expense categories. Year-to-date P&Ls should reflect current results within 30-60 days of submission. Applying in April with statements through February? Acceptable. Submitting one ending in October? Unacceptable.

Balance sheets capture assets, liabilities, and equity at a specific moment. Lenders use these to evaluate net worth and identify potential collateral sources.

Business debt schedule lists every loan, credit line, and lease you maintain—showing current balances, monthly payment amounts, and maturity dates. This feeds directly into their payment capacity calculations.

Accounts receivable aging report (for B2B companies) breaks down outstanding invoices by age categories. Lenders view receivables under sixty days as reasonably liquid assets. Invoices exceeding ninety days? Those raise collection concerns.

Business licenses and registrations confirm you're legally authorized to operate. Lenders want current licenses free of violations or unresolved compliance problems.

Articles of incorporation or organization establish your business structure and ownership distribution. LLCs need operating agreements. Corporations need articles of incorporation and corporate bylaws.

Commercial lease agreement (for businesses renting space) verifies your location and demonstrates stable occupancy. Lenders examine lease terms—one expiring in six months prompts questions about your future operating location.

Business plan requirements fluctuate wildly. Traditional banks and SBA lenders typically demand comprehensive plans covering market analysis, competitive positioning, management team credentials, and financial projections. Online lenders might only request a brief summary.

Personal financial statement discloses your individual assets and liabilities. This becomes critical when you're providing personal guarantees.

Legal documents might include franchise agreements, partnership agreements, or intellectual property documentation, depending on your business structure and industry.

Startups face additional documentation challenges. Without business tax returns, lenders rely more heavily on business plans, personal financial strength, and industry experience. Expect to provide detailed revenue projections supported by clear, reasonable assumptions.

Industry-Specific and Collateral Requirements

Author: Matthew Redford;

Source: nayiyojna.com

Lenders sort industries by risk level, adjusting standards accordingly. Stable, mature sectors with predictable cash flows—accounting firms, medical practices, established retail operations—face fewer approval obstacles than volatile or emerging industries.

Restaurants and food service businesses get extra scrutiny because of high failure rates. Lenders typically demand larger down payments (25-30% versus 10-20% for lower-risk industries), longer operating histories, and impose more conservative loan-to-value ratios on equipment and property.

Construction companies face unique challenges because of project-based revenue structures. Lenders want seeing substantial backlog of actually contracted work, not merely proposals or outstanding bids. They'll review bonding capacity and might require assignment of contract proceeds as supplementary security.

Professional service firms—consultants, marketing agencies, law practices—often lack tangible assets for collateral purposes. Lenders focus more intensely on accounts receivable quality, client contract terms, and owner credentials. Some lenders offer specialized accounts receivable financing advancing 70-85% of outstanding invoice values.

Franchise businesses benefit from brand recognition and validated business models. Lenders view franchises more favorably than independent startups, though they'll verify the franchisor's reputation and examine franchise disclosure documents. Some lenders maintain approved franchise lists offering expedited approval and improved terms.

Collateral fundamentally alters the lending equation. Secured loans—backed by specific assets—carry lower interest rates and get approved more frequently than unsecured loans. Common collateral categories include:

Real estate offers the strongest security. Commercial property loans typically advance 70-80% of appraised value with 15-25 year repayment terms. Lenders record mortgages or deeds of trust, establishing legal claims if you default.

Equipment secures loans for machinery, vehicles, or technology purchases. Lenders advance 80-90% of equipment value for new purchases, less for used equipment. They file UCC-1 financing statements establishing their security interest.

Inventory works for wholesale, retail, and distribution operations. Lenders typically advance 50-60% of inventory value because of obsolescence risks and liquidation challenges.

Accounts receivable secure credit lines and factoring arrangements. Lenders advance 70-85% of receivables under sixty days, excluding invoices from customers with documented payment problems.

Cash savings or certificates of deposit can secure loans at favorable rates. Some lenders offer "passbook loans" at rates just 2-3 percentage points above what your savings earn.

Unsecured loans—without specific collateral—rely entirely on cash flow strength and creditworthiness. These carry substantially higher rates (often 10-30%+ annually) and shorter terms (six months to five years). Personal guarantees are standard, making business owners personally liable when the company can't repay.

Author: Matthew Redford;

Source: nayiyojna.com

Blanket liens grant lenders security interest in all business assets—present and future. Common with SBA loans and certain traditional bank loans. You continue using assets during normal operations, but lenders can seize them following default.

Common Reasons Business Loan Applications Get Denied

Understanding rejection reasons helps you avoid repeating mistakes. Many denials stem from correctable errors rather than fundamental business problems.

Insufficient cash flow tops the rejection list. Lenders need confidence your business generates adequate funds covering loan payments plus operating expenses. Profit and loss statements showing minimal net income? Bank statements revealing chronically low balances? These signal payment capacity concerns. Before submitting applications, run your own numbers—results below 1.25 mean either waiting until revenue improves or requesting smaller amounts.

Poor credit history creates immediate obstacles. Late payments, charge-offs, collection accounts, maxed-out credit cards—all indicate financial mismanagement. Check your personal and business credit reports a few months before you plan to apply. Dispute inaccuracies and address legitimate problems where possible—reducing credit card balances below thirty percent of limits can improve scores within weeks.

Inadequate documentation frustrates underwriters and delays decisions. Missing tax returns, incomplete financial statements, outdated bank statements force lenders to repeatedly request additional information, dragging the process indefinitely. Some applicants never provide requested items, leading to automatic denial. Create a comprehensive checklist and gather everything upfront.

Weak business plan or unclear use of funds creates doubts about how you'll deploy borrowed capital. Generic descriptions like "operating expenses" or "working capital" prove insufficient. Lenders demand specifics: "Purchasing $85,000 in inventory for the holiday season, historically our strongest quarter generating forty-five percent of annual revenue." Vague plans suggest inadequate strategic thinking about the investment's return.

Too much existing debt restricts capacity for additional borrowing. Already stretched thin servicing current obligations? Lenders won't add more burden. Review your existing debt load and consider paying down balances before seeking new financing.

Insufficient operating history particularly damages startups. Operating less than twelve months? Traditional lenders will likely decline. Consider alternative lenders working with newer businesses, or delay applying until you've established longer track record.

Industry concerns affect businesses in sectors lenders classify as high-risk. Cannabis-related businesses encounter federal banking restrictions. Cryptocurrency ventures face institutional skepticism. Adult entertainment finds limited financing options. If you operate in a challenging sector, seek lenders specializing in your industry.

Legal or compliance issues trigger immediate red flags. Tax liens, pending litigation, licensing violations, regulatory problems—all signal elevated risk. Resolve these before applying—lenders won't fund businesses with unresolved legal troubles.

Unrealistic financial projections undermine credibility. Projecting 300% revenue growth without supporting evidence? Claiming fifty percent market share in saturated industries? Looks naive. Build projections on conservative assumptions with clear supporting logic.

Frequent bank overdrafts or NSF fees visible in statements indicate poor cash management. Even with overall profitability, chronic overdrafts suggest operating too close to the financial edge. Build adequate cash buffers before applying.

Recent business structure changes create uncertainty. Recently converted from sole proprietorship to LLC? Merged with another company? Lenders may want several months of financial performance under the new structure before lending.

Strengthen weak applications by addressing deficiencies before submission. Credit problems? Spend 6-12 months improving scores. Tight cash flow? Wait for 2-3 consecutive strong months. Incomplete documentation? Work with an accountant preparing proper statements.

FAQ: Business Loan Eligibility Questions

Meeting business loan requirements demands preparation, patience, and meticulous attention to detail. Lenders evaluate multiple factors simultaneously—no single strength compensates for major weaknesses elsewhere. Strong revenue with damaged credit? Excellent credit with minimal operating history? Both scenarios create approval challenges.

Start by honestly assessing where you stand against typical requirements for your target lender category. Traditional banks establish the highest standards but offer the lowest interest rates. Online lenders provide faster decisions and work with newer businesses, at higher cost. Alternative financing fills gaps for businesses not meeting conventional standards.

Assemble documentation early in the process. Complete, accurate financial records demonstrate professionalism and accelerate approval timelines. Incomplete applications waste time and damage approval odds.

Address weaknesses before applying whenever possible. Spend several months improving credit scores, building cash reserves, or establishing longer operating history. The difference between approval and rejection often comes down to timing—applying six months later with stronger financials fundamentally changes outcomes.

Explore multiple lender categories. Traditional bank rejection doesn't mean online lenders or alternative financing won't approve you. Each lender type serves different business profiles. Match your company's current position to lenders working with similar businesses.

Examine your application through the lender's perspective. Would you lend money to a business with your financial profile? If the answer isn't clearly yes, identify what needs improvement. Honest self-assessment prevents wasted applications and positions you for success when truly ready.

Business financing remains accessible to companies at various stages, from startups to established enterprises. Understanding what lenders evaluate, preparing accordingly, and applying to appropriate lenders dramatically improves your odds of securing needed capital.