Person reviewing federal student loan documents on a desk with laptop and phone

How to Decide if Student Loan Consolidation Is Right for You

Content

Managing multiple federal student loan payments each month can feel like juggling with too many balls in the air. Federal student loan consolidation offers a way to simplify that process by combining several loans into one. But simplicity comes with trade-offs that can affect your finances for years, sometimes decades.

This guide breaks down everything you need to know about consolidating federal student loans—what it actually does to your debt, who can do it, and most importantly, whether it makes sense for your specific situation.

What Is Federal Student Loan Consolidation and How Does It Work

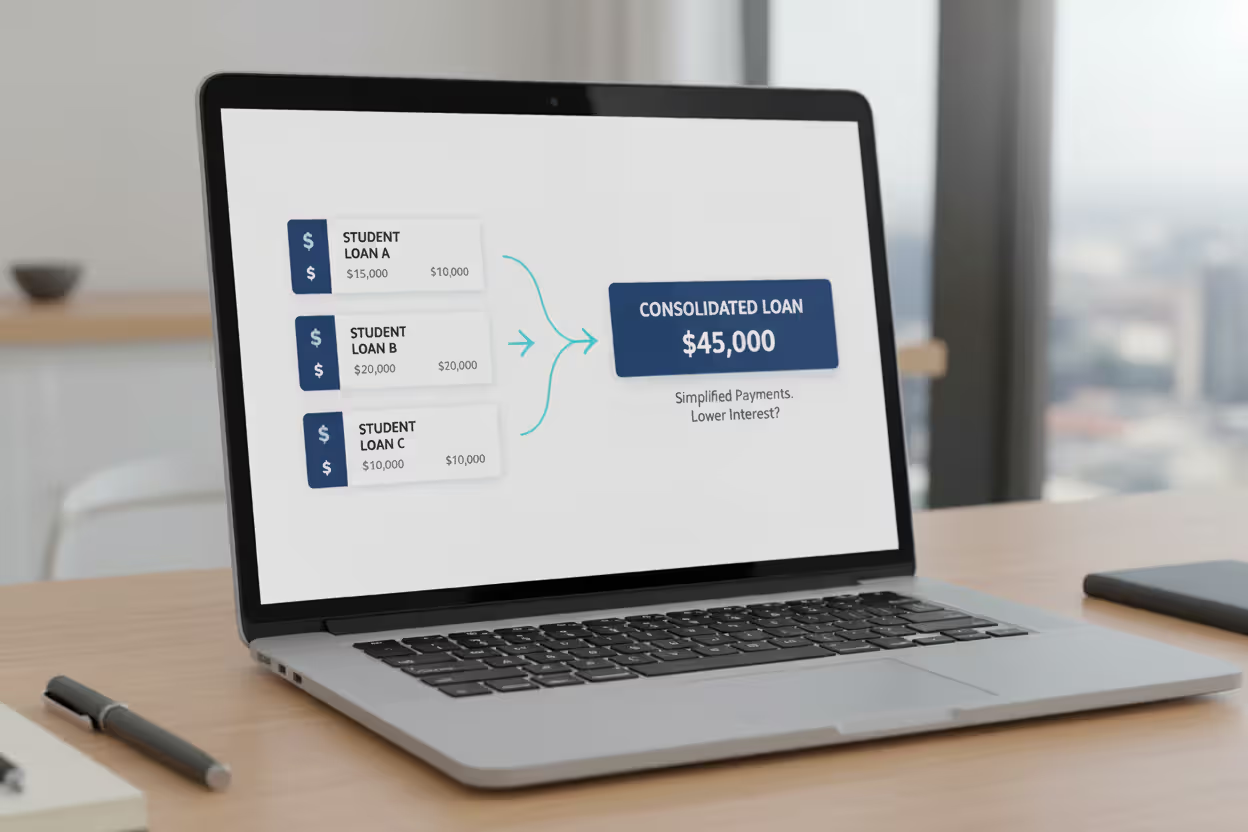

Federal student loan consolidation explained: It's a free government program that lets you combine multiple federal education loans into a single Direct Consolidation Loan through the U.S. Department of Education. You're not refinancing or getting a new loan from a private lender—you're bundling existing federal loans together under one servicer with one monthly bill.

Here's how the process works mechanically. You apply through StudentAid.gov, selecting which eligible federal loans you want to include. The Department of Education pays off those original loans and creates a new Direct Consolidation Loan for the total amount. Your new interest rate is the weighted average of your old rates, rounded up to the nearest one-eighth of one percent. If you had loans at 4.5%, 5.0%, and 6.0%, your consolidated rate might land around 5.2%—not lower, just averaged.

The consolidation becomes official once your application is processed, typically within 30 to 60 days. Your old loans disappear from your account, replaced by the single consolidated loan. You'll get a new servicer (possibly different from any you worked with before) and start fresh with a new repayment timeline.

One critical detail: consolidation only works with federal loans. You cannot consolidate private student loans through this program, though there's a workaround for certain older federal loans that we'll cover in the eligibility section.

Author: Brandon Ellery;

Source: nayiyojna.com

Who Qualifies for Student Loan Consolidation

Most federal student loan borrowers qualify, but the student loan consolidation requirements have specific boundaries.

You must be in your grace period, in repayment, or in default. Strangely enough, being in default doesn't disqualify you—in fact, consolidation is one of the few ways to get defaulted loans back into good standing without paying the full amount owed upfront. You can also consolidate while in school if you're including a Direct PLUS Loan or if you agree to an income-driven repayment plan.

Eligible loan types include Direct Loans (Subsidized, Unsubsidized, PLUS), Federal Family Education Loans (FFEL), Federal Perkins Loans, Health Professions Student Loans, and several other federal programs. Parent PLUS loans can be consolidated, but only with other Parent PLUS loans—you can't mix them with your own student loans.

Here's what you cannot consolidate: private loans from banks or credit unions, state agency loans that aren't federally backed, and loans already in a Direct Consolidation Loan (though you can reconsolidate under certain circumstances if you add at least one new eligible loan).

Timing matters more than most borrowers realize. If you consolidate during your six-month grace period after graduation, you immediately enter repayment—losing those remaining grace months. If you're three months into your grace period and consolidate, you forfeit the other three months of payment-free time.

You need at least one eligible federal loan to consolidate. You cannot consolidate a single loan by itself unless you're doing so to access specific repayment plans or forgiveness programs (like consolidating to make FFEL or Perkins loans eligible for Public Service Loan Forgiveness).

Advantages and Disadvantages of Consolidating Your Student Loans

The pros and cons of consolidation aren't equal for everyone. What helps one borrower might hurt another, depending on their loan portfolio and financial goals.

Key Benefits of Consolidation

Single monthly payment. Instead of tracking three, five, or eight different loans with different servicers and due dates, you make one payment. This reduces the chance of missing a payment through simple oversight. For borrowers with loans spread across multiple servicers, this administrative relief is real.

Access to additional repayment plans. Some federal loans—particularly FFEL and Perkins loans—don't qualify for income-driven repayment plans or Public Service Loan Forgiveness unless you consolidate them into a Direct Consolidation Loan first. If you work in public service or nonprofit, consolidation might be your only path to loan forgiveness.

Lower monthly payments through extended repayment. Consolidation can stretch your repayment term up to 30 years depending on your total loan balance. If you owe $60,000 or more, you could qualify for a 30-year term, which dramatically lowers your monthly obligation. A borrower paying $600 monthly on a 10-year plan might drop to $350 on an extended 25-year plan.

Exit from default without a lump sum. If your loans are in default, consolidating them (often combined with enrolling in an income-driven plan) can rehabilitate your loans and stop wage garnishment or tax refund offset without requiring you to pay thousands upfront.

Fixed interest rate for life. Your new consolidated rate is fixed for the life of the loan. If you had variable-rate FFEL loans from years ago, consolidation locks in a fixed rate, eliminating future rate increases.

Author: Brandon Ellery;

Source: nayiyojna.com

Potential Drawbacks to Consider

You'll pay more interest over time. Extending your repayment from 10 years to 25 years means you're paying interest for 15 additional years. That $60,000 loan might cost you an extra $30,000 to $40,000 in interest over the life of the loan, even though your monthly payment dropped.

Loss of progress toward forgiveness. If you've already made 50 payments toward Public Service Loan Forgiveness, consolidating resets your payment count to zero. You'd need to make 120 new qualifying payments. This is one of the costliest mistakes borrowers make.

Capitalized interest increases your principal. Any unpaid interest on your old loans gets added to your principal when you consolidate. If you had $2,000 in unpaid interest across your loans, that becomes part of your new loan balance, and you'll pay interest on that interest going forward.

Loss of borrower benefits on original loans. Some older federal loans came with interest rate discounts for auto-pay or on-time payments. Consolidation wipes out those perks. Similarly, if you had subsidized loans where the government paid interest during deferment, that subsidy applies only to the subsidized portion of your new consolidated loan—and tracking that gets complicated.

Your interest rate might increase slightly. The rounding-up rule means your new rate could be up to 0.125% higher than the true weighted average. On a large balance, that adds up over decades.

You lose the ability to target high-rate loans. Some borrowers use the avalanche method, paying extra toward their highest-interest loan while making minimums on others. Consolidation blends everything into one rate, eliminating this strategy.

Student Loan Consolidation vs Refinancing: What's the Difference

These terms get used interchangeably, but they're completely different processes with opposite implications for your federal protections.

Consolidation vs refinancing student loans comes down to this: consolidation keeps your loans federal and maintains all federal benefits; refinancing moves your loans to a private lender and you lose federal protections permanently.

| Feature | Federal Consolidation | Private Refinancing |

| Interest rate calculation | Weighted average of existing rates, rounded up | New rate based on credit and income; potentially lower |

| Federal benefit retention | Keeps all federal protections (IDR, forbearance, forgiveness) | Loses all federal benefits permanently |

| Credit check requirement | None (available even with poor credit) | Yes; requires good to excellent credit |

| Eligibility | Federal loans only | Federal and private loans |

| Best for whom | Borrowers needing federal protections, pursuing forgiveness, or in financial uncertainty | High earners with stable income seeking lower rates, not pursuing forgiveness |

Refinancing through a private lender like SoFi, Earnest, or a bank can lower your interest rate if you have strong credit and income. A borrower with a 6.5% federal rate might refinance to 4.0% and save thousands. But that savings comes at a steep cost: you lose access to income-driven repayment, federal forbearance, deferment options, and all forgiveness programs.

During the COVID-19 payment pause that ended in 2023, millions of borrowers with federal loans paid nothing for over three years. Those who had refinanced to private loans kept making payments throughout. That's the protection gap in a nutshell.

Choose consolidation when you need to maintain federal benefits, qualify for forgiveness programs, or access income-driven plans. Choose refinancing when you're financially stable, have excellent credit, don't work in public service, and can secure a significantly lower rate that justifies giving up federal protections.

Never refinance federal loans if there's any chance you'll need income-driven repayment or if you're pursuing any forgiveness program.

Author: Brandon Ellery;

Source: nayiyojna.com

How Consolidation Affects Your Repayment Plan and Loan Terms

When consolidation changes repayment, the impacts ripple across your entire loan structure—not just your monthly bill.

Repayment timeline resets. Your new Direct Consolidation Loan starts fresh with a new repayment term, typically 10 to 30 years depending on your total education debt. If you'd already paid four years on a 10-year loan, consolidating starts you back at year zero. Those four years of progress vanish. You're not picking up where you left off; you're beginning again.

Payment count resets for forgiveness programs. This is where borrowers get burned. Public Service Loan Forgiveness requires 120 qualifying payments. If you've made 70 payments and then consolidate, you're back to zero. The same applies to the income-driven repayment forgiveness that kicks in after 20 or 25 years of payments—consolidating resets that clock.

There's one major exception: As of 2022, the Department of Education implemented a one-time payment count adjustment that gave borrowers credit for past payments when consolidating FFEL or Perkins loans into the Direct program. But that was a temporary policy fix, and normal rules apply going forward.

Interest capitalization adds to your balance. When you consolidate, any unpaid interest from your old loans capitalizes—it's added to your principal. If you were in forbearance or deferment and interest was piling up, that amount becomes part of your new loan balance. You'll pay interest on interest, which compounds your cost over time.

Monthly payments can increase or decrease. Most borrowers consolidate to lower their monthly payment by extending the term. But if you consolidate into a standard 10-year plan and your original loans had 15 or 20 years remaining, your payment could actually increase because you're compressing the timeline.

Income-driven repayment becomes available. For borrowers with FFEL or Perkins loans, consolidation is the gateway to income-driven repayment plans like SAVE (Saving on a Valuable Education), PAYE, or IBR. These plans cap your payment at a percentage of discretionary income, which can be life-changing for low earners or those with high debt-to-income ratios.

Loan forgiveness eligibility changes. Perkins Loan forgiveness for teachers or Perkins Loan cancellation for certain professions goes away if you consolidate those loans. Once a Perkins Loan becomes part of a Direct Consolidation Loan, it's no longer a Perkins Loan—it's a Direct Loan, and Perkins-specific benefits disappear.

When Consolidation Makes Sense and When to Avoid It

The decision framework isn't complicated, but it requires honest assessment of your situation and goals.

Consolidation makes sense when:

You have FFEL or Perkins loans and want to pursue Public Service Loan Forgiveness. These older loan types don't qualify for PSLF unless consolidated into the Direct Loan program. A teacher with $40,000 in FFEL loans working at a public school needs to consolidate to access forgiveness after 10 years of qualifying payments.

You're juggling multiple servicers and keep missing payments. If administrative complexity is causing you to miss due dates, the risk of late fees and credit damage outweighs the downsides of consolidation. One payment to one servicer is easier to manage.

Your loans are in default and you need to stop garnishment. Consolidation combined with an income-driven repayment plan can pull your loans out of default and halt wage garnishment or Social Security offset. This is often faster and less expensive than loan rehabilitation.

You need access to income-driven repayment and have ineligible loan types. FFEL borrowers who need to cap payments based on income must consolidate first. If you're earning $35,000 annually with $50,000 in FFEL debt, consolidation unlocks payment plans that might cut your monthly bill in half.

You have variable-rate FFEL loans and want rate certainty. Older FFEL loans sometimes carried variable rates. Consolidating locks in a fixed rate, protecting you from future increases.

Author: Brandon Ellery;

Source: nayiyojna.com

Avoid consolidation when:

You've already made significant progress toward forgiveness. If you're 80 payments into PSLF or seven years into a 20-year income-driven plan, consolidating erases that progress. The cost is too high.

You're planning to aggressively pay off your loans. Borrowers aiming to clear their debt in three to five years don't benefit from consolidation. The weighted-average rate doesn't help, and you don't need extended terms if you're paying extra anyway.

You have Perkins Loans with valuable cancellation benefits. Teachers, nurses, and certain public servants qualify for Perkins Loan cancellation—up to 100% forgiveness over five years. Consolidating destroys this benefit. Check your specific cancellation eligibility before consolidating Perkins loans.

You're in your grace period and need those months. If you just graduated and have four months of grace remaining, consolidating immediately throws away that payment-free time. Wait until your grace period ends unless there's a compelling reason to start repayment early.

You could refinance to a much lower rate and don't need federal protections. A doctor earning $200,000 with $150,000 in loans at 6.8% might save $40,000 by refinancing to 3.5% with a private lender. If you're not pursuing forgiveness and have stable, high income, refinancing beats consolidation.

Expert perspective:

Consolidation is a tool, not a solution.I see borrowers consolidate because it sounds like it should help, without understanding what they're giving up. The biggest mistake is consolidating when you're already halfway to forgiveness. Those lost payments can cost you tens of thousands of dollars. On the flip side, borrowers with FFEL loans who qualify for PSLF and don't consolidate are leaving money on the table. The decision has to match your specific loan portfolio and career path

— Marcus Chen

Frequently Asked Questions About Student Loan Consolidation

Student loan consolidation works for some borrowers and backfires for others. The difference comes down to understanding what you're gaining versus what you're giving up. If you need to simplify payments, access income-driven plans, or qualify older loans for forgiveness programs, consolidation serves a clear purpose. But if you've already made years of progress toward forgiveness, have valuable loan-specific benefits, or could secure a lower rate through refinancing, consolidation might cost you more than it saves.

Take inventory of your specific loan types, how many qualifying payments you've made toward any forgiveness program, your current financial situation, and your career trajectory. Federal consolidation is free and reversible only by refinancing (which brings its own trade-offs), so the decision deserves more than a quick application. The right choice depends entirely on your circumstances, not on generic advice or what worked for someone else with a different loan portfolio.