Person reviewing insurance documents at home after property damage

How to File an Insurance Claim and What to Expect

Content

Most people don't think about insurance claims until disaster strikes—and then suddenly, you're googling "what do I do now?" at 2 AM after a fender bender or while staring at water pouring through your ceiling. The process doesn't have to be a nightmare. When you know what to expect and how to prepare, you can turn a stressful situation into a manageable one and actually get the payout your policy promises.

This article breaks down everything from your first phone call to fighting back if you get denied.

What Is an Insurance Claim and When Should You File One

Think of an insurance claim as knocking on your insurer's door and saying, "Hey, remember that policy I've been paying for? I need you to hold up your end of the bargain." Technically, it's your formal request for payment after something covered by your policy goes wrong.

File when you've experienced a loss that your policy covers—a car wreck, your house catching fire, a tree crashing through your roof during a storm, expensive medical treatment, or when a life insurance policyholder passes away.

Here's the tricky part: timing. Most insurers want to hear from you fast. Really fast. Auto accidents? They typically expect a call within 24 to 72 hours. House damage? You've got a bit more breathing room—usually several days to a few weeks—but don't push it. Even if you're not 100% sure you'll actually file, report it anyway. You can back out later, but calling three months after the fact almost guarantees a rejection.

Should you file every time something goes wrong? Absolutely not. If your repair bill is $1,200 and your deductible is $1,000, you're only getting $200 back—and that claim goes on your record. Two or three small claims in a few years can jack up your premiums or get you dropped entirely. Many people use this rule: only file when the damage exceeds your deductible by at least a grand, or when someone else might sue you for liability.

How to File an Insurance Claim Step by Step

Every insurer has its own quirks, but the basic flow stays pretty consistent. Knowing what happens next keeps you from feeling blindsided.

Reporting the Incident to Your Insurance Company

Call your insurance company right away—or use their app or website if you prefer digital communication. Most have 24/7 hotlines. Dig out your policy number before you dial (it's on your insurance card or declarations page). They'll want the basics: when it happened, where, and what went down.

They'll give you a claim number during this first contact. Write it on your phone, tattoo it on your forehead—whatever works. You'll need this number for literally every future conversation.

Answer their questions truthfully and completely, but keep it factual. Don't say things like "yeah, this is totally my fault" or "I should have been paying better attention" before anyone's actually figured out what happened. State facts, not feelings or guesses.

For car accidents, swap info with the other driver but keep your mouth shut about who's to blame. For home damage, stop the bleeding—literally cover that roof hole with a tarp, board up shattered windows—and hang onto those receipts. Insurance policies usually reimburse these emergency measures.

Author: Brandon Ellery;

Source: nayiyojna.com

Completing the Claim Forms

A few days after your initial call, expect a pile of paperwork (digital or physical). These forms want detailed accounts of everything: what broke, how it broke, what it'll cost to fix, whether police showed up—the works.

Fill out every single line. Leaving blanks makes adjusters suspicious or just slows everything down. If something doesn't apply to you, write "N/A" so they know you didn't skip it accidentally. Get specific. Don't write "car damaged"—write "front bumper crumpled inward 6 inches, passenger headlight completely shattered, hood creased down the center."

Here's a pro move: attach all your supporting documents right now instead of waiting for them to ask. This cuts weeks off your timeline. Make copies of everything and note when you sent it.

Working with the Claims Adjuster

Once your paperwork lands, the insurance company assigns an adjuster—basically a professional investigator who'll figure out what happened, whether it's covered, and how much to pay. They'll reach out to schedule an inspection or ask for more information.

Respond quickly. When you ignore their calls or emails, they assume you're not in a hurry, and your claim sinks to the bottom of their pile. That said, you don't have to give recorded statements without understanding what you're agreeing to, especially if the situation's complicated or involves serious liability.

During inspections, walk around with the adjuster and point out everything that's damaged. They're good at their jobs, but they're also human and can miss stuff. Take your own photos and videos before anyone starts repairs—this gives you backup evidence if disputes pop up later. If their damage estimate seems way too low, you can push back and request another inspection, though you might need to hire your own independent appraiser at your expense.

The single biggest mistake policyholders make is failing to document everything from day one. I've seen legitimate claims denied simply because the insured couldn't prove the extent of their loss. Photos, receipts, and written records are your best defense

— Jennifer Martinez

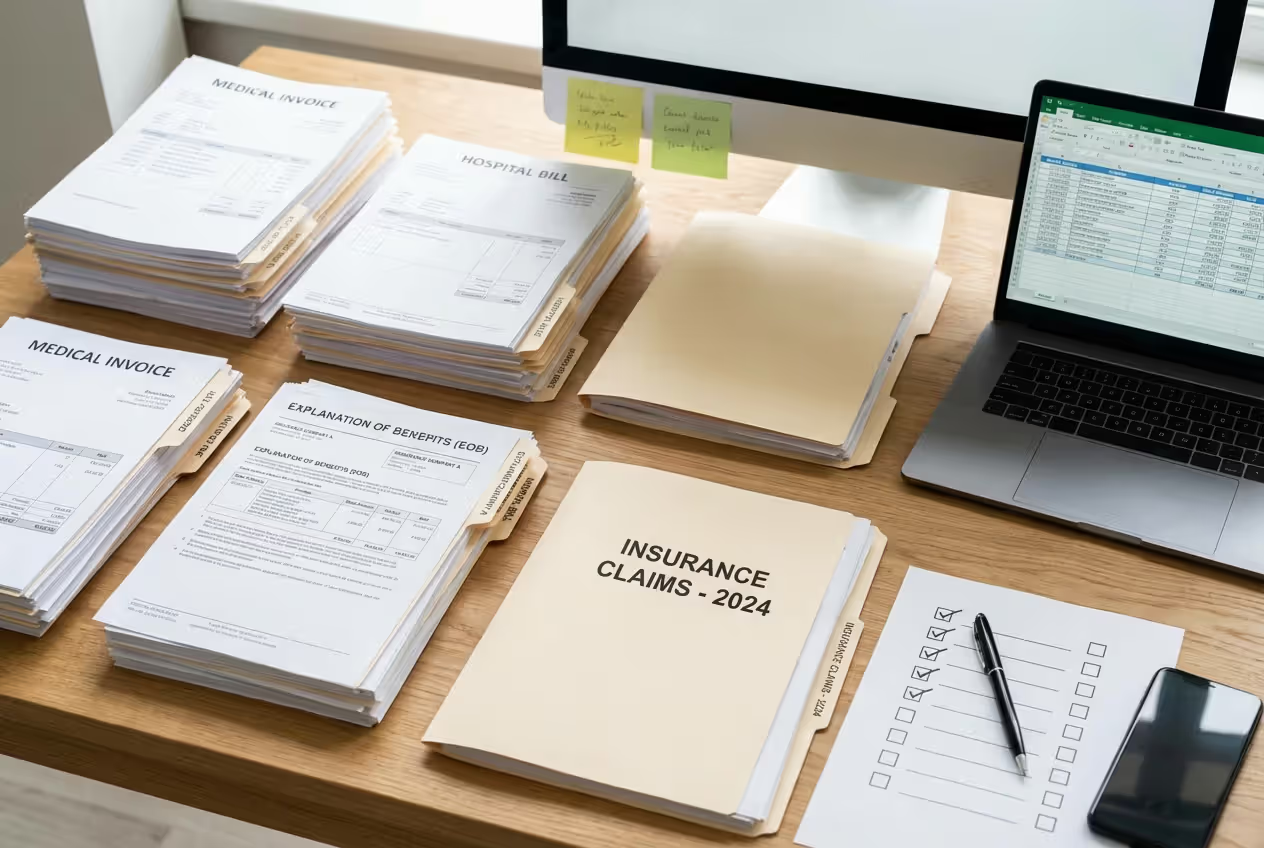

Documents Needed to Support Your Insurance Claim

Documentation separates successful claims from failed ones. Missing paperwork ranks right up there with late reporting as a top reason claims get rejected or delayed.

Start with your policy's declarations page—that's the document showing your coverage limits, deductibles, and what's actually covered. Then grab your incident report: police reports for accidents or theft, fire department reports for fires, medical records for health issues.

For auto claims: snap photos of every dent, scratch, and broken part from multiple angles. Get repair estimates from at least two licensed shops. Document any injuries with medical bills and treatment notes. If another driver's involved, you need their insurance details, license plate number, driver's license info, and contact information. Got dashcam footage or witness statements? Even better—include those.

For home claims: go photo-crazy. Document damage immediately, then prove you actually owned the stuff that got destroyed or stolen. Dig up receipts, user manuals with serial numbers, or old photos showing items in your home before disaster struck. No receipts? Credit card statements work. For major catastrophes like fires or floods, professional contractor estimates become essential.

For health claims: collect itemized bills from every doctor, hospital, and pharmacy involved. Grab your explanation of benefits (EOB) forms from your insurer. You'll need medical records proving the treatment was necessary (not cosmetic or experimental), plus any referral paperwork or prior authorization documents your policy required.

Author: Brandon Ellery;

Source: nayiyojna.com

Create a physical or digital folder organized by date. Build a spreadsheet tracking every conversation: date, who you talked to, what was discussed, what needs to happen next. This level of organization impresses adjusters and becomes invaluable if you need to appeal or escalate.

How Long Does the Insurance Claim Process Take

Asking "how long will this take?" is like asking "how long is a piece of string?"—it depends. Simple claims with obvious liability and minor damage can wrap up in days. Complicated messes involving disputes, major damage, or multiple parties can drag on for months.

Most states have laws forcing insurers to acknowledge your claim within about 15 days and make a decision within 30 to 45 days after receiving complete documentation. But here's the catch: that clock doesn't start until they have everything they asked for. Missing documents hit the reset button.

What speeds things up: submitting complete documentation immediately, clear-cut liability, working with repair shops your insurer already knows, choosing electronic payments over mailed checks, and straightforward coverage with no room for interpretation.

What slows things down: fights over who's at fault, fraud investigations, natural disasters that swamp the system with thousands of claims at once (think hurricanes or wildfires), ongoing medical treatment for injuries, and situations where multiple insurance companies need to coordinate.

| Claim Type | Simple Claim Timeline | Complex Claim Timeline | Key Factors Affecting Speed |

| Auto | 7-14 days | 30-90 days | Who's at fault, injury severity, whether parts are in stock |

| Homeowners | 14-30 days | 60-180 days | How bad the damage is, contractor availability, coverage disputes |

| Health | 15-30 days | 45-90 days | Whether pre-approval was needed, if treatment was medically necessary, billing code errors |

| Life | 30-60 days | 90-180 days | Beneficiary fights, investigating cause of death, contestability period issues |

If your timeline's blown past expectations, call your adjuster for an update. Write down what they say. Getting radio silence? Escalate to their supervisor or file a complaint with your state's insurance department—that usually gets things moving fast.

Common Reasons Insurance Claims Get Denied

Denials don't always mean you screwed up. Sometimes it's a misunderstanding or the adjuster misread something that you can fix on appeal.

Policy exclusions kill tons of claims. Your policy has a whole section listing what it won't cover. Standard homeowners policies don't cover floods (you need separate flood insurance). Most policies exclude intentional damage, normal wear and tear, and specific natural disasters depending on your location. Dig into your exclusions section before filing so you're not caught off guard.

Missed deadlines are a fast track to rejection. Report an auto accident six months late without a compelling reason? Denied. Fail to submit requested documents within their deadline? Claim closed.

Weak documentation leaves adjusters unable to verify anything. Can't prove you owned the stolen laptop? No payout. Can't demonstrate how badly your car was damaged? They'll lowball you or deny the claim entirely.

Pre-existing conditions affect health claims obviously, but also some property claims. If your roof was already falling apart before the hailstorm, your insurer might argue the damage resulted from neglected maintenance rather than the storm itself.

Fraud red flags trigger instant denials and possible policy cancellation. Obvious fraud includes staging accidents or lying about what happened, but even innocent inconsistencies—saying the accident happened at 3 PM on your form but telling the adjuster 5 PM on the phone—raise suspicions. Stick to facts and never exaggerate losses.

Lapsed coverage is straightforward: no active policy when the incident occurred means no payout. This includes situations where you thought you were covered but a payment bounced, or where you switched policies and something happened during the gap.

Author: Brandon Ellery;

Source: nayiyojna.com

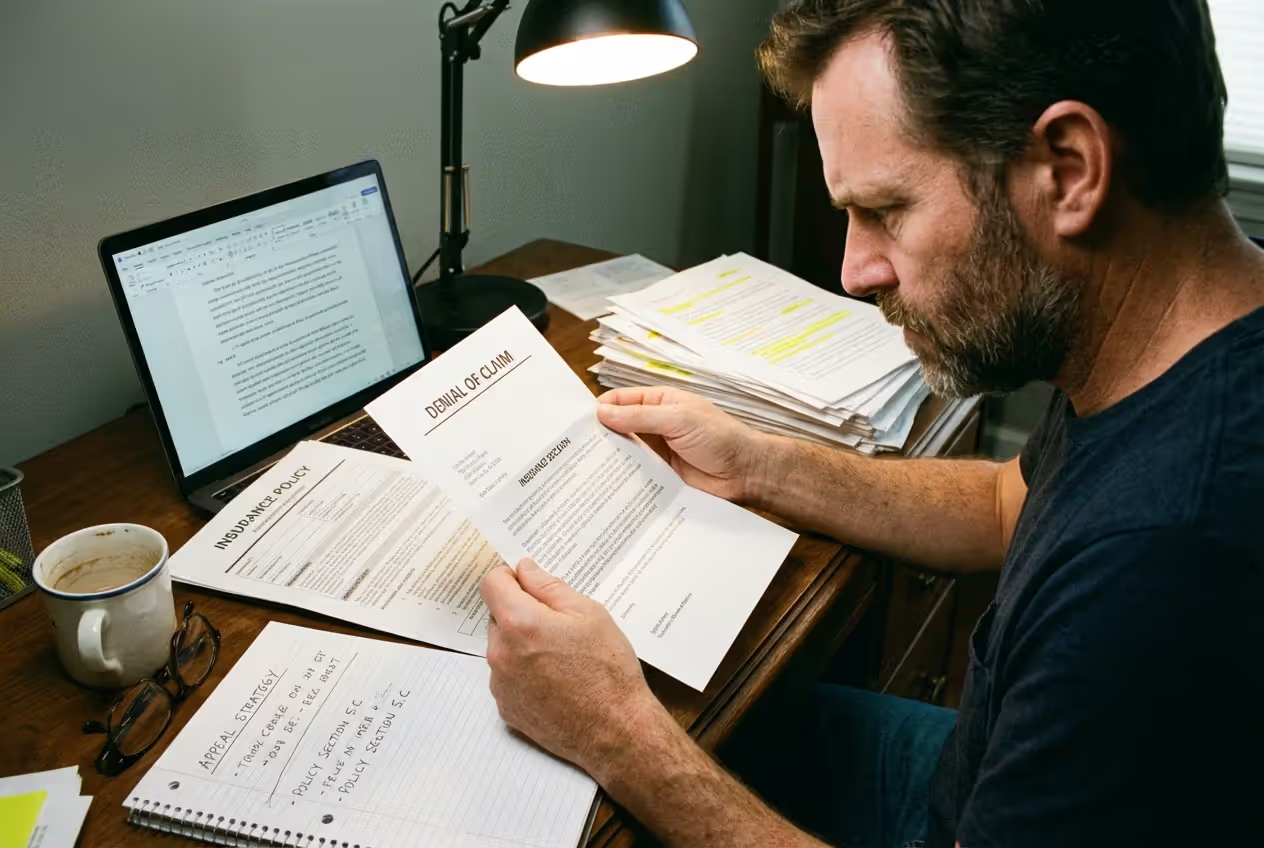

What to Do If Your Insurance Claim Is Denied

A denial letter doesn't end the story. Plenty of initially-denied claims get approved on appeal when people provide better evidence or catch errors in how the policy was interpreted.

Ask for a detailed written explanation of why they denied your claim. Insurers must cite specific policy language or reasons. Pull out your actual policy and compare their explanation against what it actually says—adjusters sometimes misinterpret coverage or overlook exceptions.

Collect additional evidence addressing whatever reason they gave for denial. They claim insufficient proof? Gather more detailed records. They cite a policy exclusion? Research whether exceptions apply to your situation—many exclusions have carve-outs for specific circumstances.

Submit a formal appeal through your insurer's internal process. Most require written appeals within 60 to 180 days of denial. Your appeal letter needs your policy and claim numbers, a clear explanation of why the denial is wrong, and supporting documents. Mail it certified so you can prove they received it.

Internal appeals going nowhere? Contact your state insurance department. These regulatory agencies investigate policyholder complaints and can pressure insurers to reconsider. They won't represent you like a lawyer, but they enforce insurance laws and can make life uncomfortable for insurers who step out of line.

For high-value claims, consider hiring a public adjuster or insurance attorney. Public adjusters work on contingency (usually 10-20% of your final settlement) and negotiate directly with your insurer. Attorneys become necessary when you suspect bad faith—situations where insurers unreasonably delay or deny clearly valid claims. Bad faith lawsuits can result in penalties way beyond your original claim amount.

Keep records of every single interaction during appeals: save emails, document phone calls with dates and names, photocopy all correspondence. This paper trail becomes your ammunition if things escalate to legal action.

Frequently Asked Questions About Insurance Claims

Successfully working through an insurance claim boils down to three things: acting quickly, documenting obsessively, and communicating clearly. Report problems immediately, build an ironclad paper trail, and stay in regular contact with your adjuster.

Your insurance policy is a two-way contract. You've got rights alongside your responsibilities. When you hold up your end—providing accurate information, submitting required documents, cooperating with investigations—your insurer must hold up theirs by investigating fairly and paying legitimate claims promptly.

Running into roadblocks? Don't give up. State insurance departments, consumer advocates, and legal professionals exist specifically to help policyholders get the coverage they've paid for. The key is acting decisively and maintaining detailed records at every step.

Spending time now to understand claims pays off when you actually need your coverage. Review your policies once a year, photograph your belongings periodically, and keep important documents somewhere accessible (like cloud storage). When trouble hits, you'll be ready to file efficiently and fight effectively for a fair settlement.