Student reviewing a financial aid award letter at a desk with calculator and documents

Is Financial Aid a Loan or Free Money

Content

Your financial aid award letter just arrived. You're staring at a list of numbers—$8,000 here, $5,500 there, another $3,000 at the bottom. Here's what nobody tells you upfront: some of those numbers represent actual money that reduces your college bill. Other numbers? They're just fancy ways of saying "we'll let you borrow this much."

Most families think financial aid means "help paying for college." Technically true, but that definition hides a massive problem. Aid packages mix together genuine assistance with debt obligations, and schools rarely make the distinction clear. You might see "$25,000 in financial aid!" on your award letter and feel relieved, only to discover later that $18,000 of that aid will haunt your bank account for the next fifteen years.

College affordability hinges on your ability to separate what you're actually receiving from what you're merely borrowing. Get this wrong, and you'll graduate owing tens of thousands more than necessary. Get it right, and you'll pay only for education that couldn't be covered through genuine assistance programs.

What Financial Aid Actually Includes

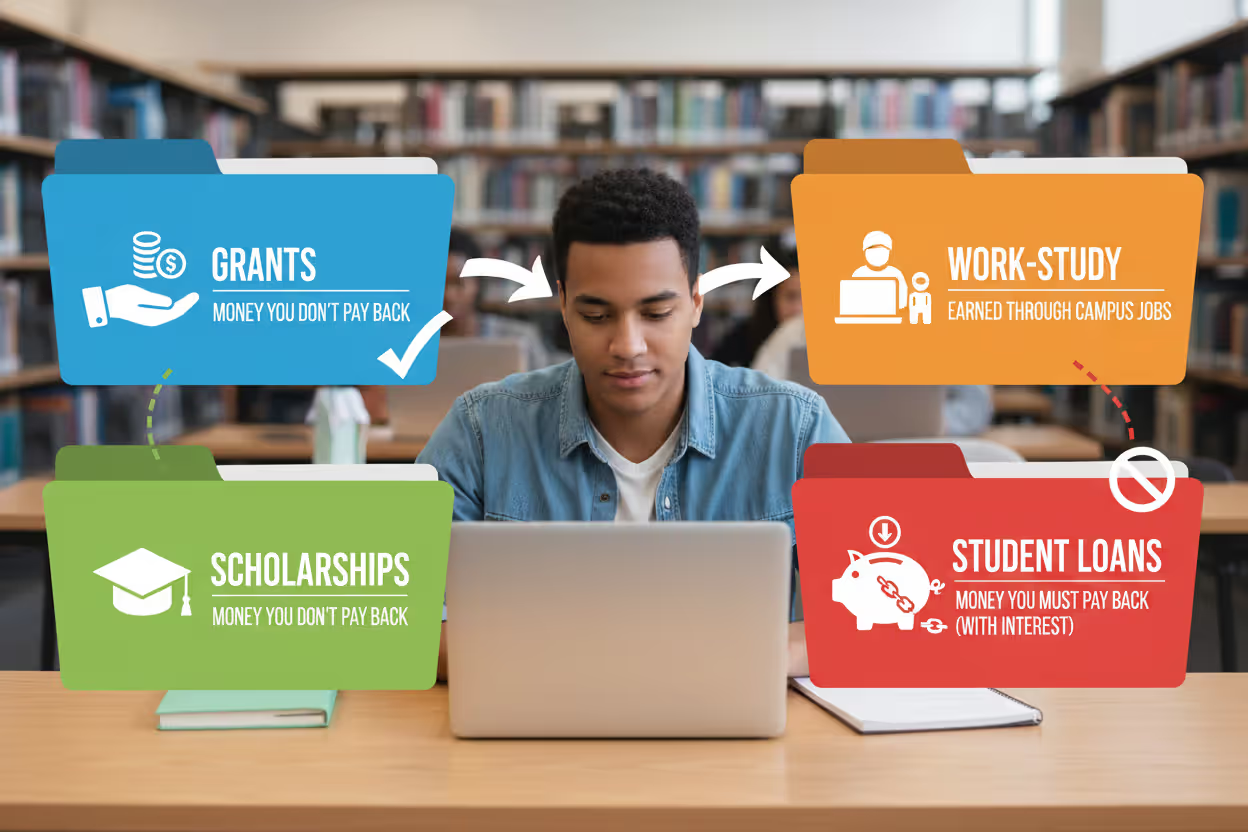

Think of financial aid as a toolbox with four different tools inside. Each tool works differently. Each comes from different sources. Each affects your wallet in completely different ways.

Author: Hannah Kingsley;

Source: nayiyojna.com

The first tool: grants. These come mostly from federal and state governments, distributed based on what your family can reasonably afford. Take the Pell Grant—up to $7,395 for the 2025-2026 year if your family's income falls below certain thresholds. California residents might get Cal Grants worth $6,000 or more. New York offers the Excelsior Scholarship covering full SUNY or CUNY tuition for middle-income families.

Second tool: scholarships. These can come from anywhere—your college, local businesses, national competitions, your parent's employer, community organizations. A 3.9 GPA might earn you $8,000 yearly from a state university. Writing a strong essay could win you $2,500 from a local credit union. Playing the oboe well enough might secure $15,000 annually from a private college desperate for orchestra members.

Third tool: work-study programs. You get a part-time campus job—shelving library books, answering phones in the admissions office, helping professors with research. Maybe ten hours weekly at $12 per hour. You earn roughly $120 per week, $480 monthly during the semester. That money arrives as paychecks you deposit like any job.

Fourth tool: loans. Here's where things get expensive. You borrow $5,500 your first year. At 5.5% interest over ten years, you'll actually pay back around $7,100. Borrow $3,500 more your second year, another $5,500 your third year, and suddenly you're looking at $50,000 in total repayment for $35,000 borrowed.

Is financial aid a loan? Only if you let it be. The system offers multiple types of assistance. Loans happen to be the largest, most aggressively promoted type, but they're not the only type available.

Grants vs Loans in Financial Aid

Here's a simple test: Will you owe anything in five years? Grants: no. Loans: absolutely yes.

Grants flow primarily through the federal government. Your FAFSA determines eligibility. Low expected family contribution? You'll likely qualify for the Pell Grant. Extremely low expected family contribution? You might also get the Federal Supplemental Educational Opportunity Grant, ranging from $100 to $4,000 depending on your school's funding. Planning to teach math or science in a low-income school district? The TEACH Grant provides up to $4,000 yearly—though it converts to a loan if you don't fulfill the teaching requirement.

State grants vary wildly. Texas offers the TEXAS Grant covering most tuition at public universities for students with family incomes below $60,000. Pennsylvania provides grants up to $5,750. Florida's Bright Futures program covers 75% to 100% of tuition based on high school GPA and test scores, functioning more like a merit scholarship despite being called a grant.

Contrast that with loans. Federal Direct Subsidized Loans—available only to undergrads showing financial need—don't accumulate interest while you're enrolled at least half-time. Interest starts after you leave school. First-year students can borrow up to $3,500 this way. Second-year students: $4,500. Third-year and beyond: $5,500 annually.

Federal Direct Unsubsidized Loans? Available regardless of need, but interest starts accumulating immediately. You're paying interest on top of interest if you don't make payments during school. Many students ignore the interest, letting it compound. A $10,000 unsubsidized loan taken freshman year grows to roughly $12,800 by graduation if you never touch it.

When comparing grants vs loans in financial aid offers, remember this: grants make college cheaper right now. Taking a loan just postpones the bill and adds a 30% to 60% markup depending on how long repayment takes.

Author: Hannah Kingsley;

Source: nayiyojna.com

You can decline loans. You can't decline grants (well, you could, but why would you?). If a school offers you $6,000 in grants and $5,500 in loans, you're only receiving $6,000 in actual assistance. The $5,500 is just an offer to borrow.

Scholarships vs Student Loans

Scholarships arrive with strings attached—but they're strings you can see and plan for. Maintaining a 3.2 GPA? Doable. Completing twenty volunteer hours yearly? Manageable. Compare that to loan strings: make 120 monthly payments on time, watch your credit score, hope your interest rate doesn't adjust upward if you refinanced to a variable rate.

Merit scholarships reward what you've already accomplished. A 1450 SAT and 3.8 weighted GPA might automatically qualify you for $12,000 annually at a state flagship. National Merit Finalist status could mean full tuition at certain universities. First-chair trumpet player? Some colleges will pay $5,000 yearly for your musical talent.

Need-based scholarships split the difference. These programs consider your financial situation but also require maintaining academic standards or participating in specific programs. The Gates Scholarship provides full cost of attendance to exceptional students with significant financial need. QuestBridge matches high-achieving, low-income students with full scholarships at elite colleges.

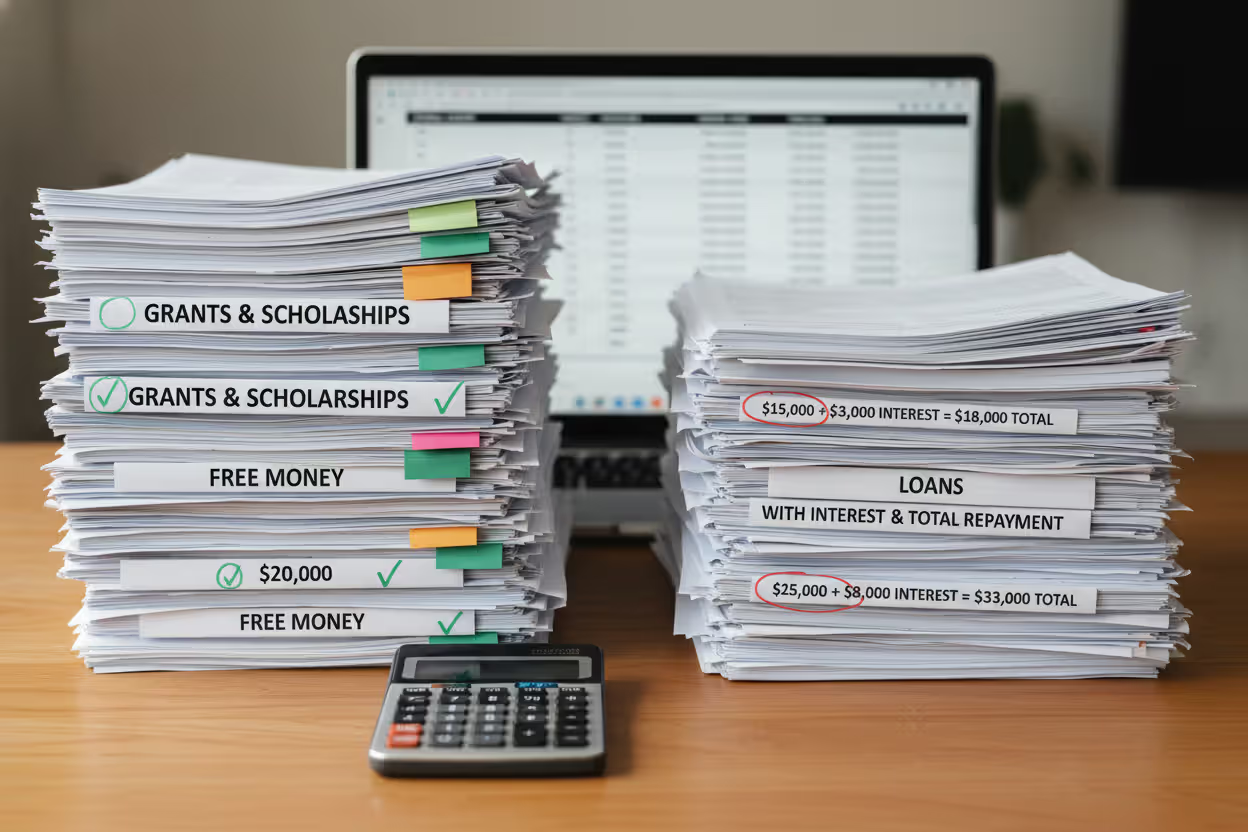

Looking at scholarships vs student loans reveals completely different long-term impacts. Accept a $4,000 scholarship, and you're $4,000 less in debt at graduation. Accept a $4,000 loan at 5.5% interest, and you'll pay roughly $5,200 back over ten years—meaning that money costs you an extra $1,200.

Multiply across four years, and the difference becomes staggering. A student with $16,000 in scholarships graduates debt-free (assuming scholarships covered full need). A student with $16,000 in loans graduates owing nearly $21,000 after interest.

The catch with scholarships? You have to find them and apply. This takes work. Most scholarships require essays, recommendations, transcripts, maybe interviews. But here's the math: spending twenty hours applying for ten scholarships might land you two awards totaling $3,500. That's $175 per hour of "work"—better pay than any part-time job.

Loans require one form. Scholarships require dozens of applications. But loans cost you money for a decade or more. Scholarships save you money forever.

What Part of Aid Must Be Repaid

Let's divide your financial aid package into two piles: the "definitely paying this back" pile and the "actually mine to keep" pile.

Definitely paying back:

Federal Direct Subsidized Loans start at 5.50% for undergraduates (2025-2026 rates). You won't pay interest while enrolled at least half-time, but repayment starts six months after graduation. Borrow $3,500 freshman year, and you'll repay roughly $4,520 over the standard ten-year plan.

Federal Direct Unsubsidized Loans charge the same 5.50% for undergrads, but interest runs from day one. Graduate students face 7.05% rates. That $3,500 borrowed freshman year? It's already $4,100 by graduation if you never paid interest during school. Total repayment: approximately $5,300.

Parent PLUS Loans and Grad PLUS Loans hit you with 8.05% interest. These also charge origination fees around 4.2%. Borrow $10,000 through a PLUS loan, and you actually receive $9,580 after fees—but you owe the full $10,000 plus interest. Ten-year repayment on that $10,000 costs roughly $14,900 total.

Private loans range from reasonable (4% to 6% for borrowers with excellent credit and a cosigner) to predatory (12% to 14% for borrowers with limited credit history). These lack federal protections. No income-driven repayment. No public service forgiveness. No forbearance options if you hit financial hardship. The bank wants its money, period.

Actually yours to keep:

Federal grants like the Pell Grant or FSEOG don't require repayment unless you withdraw before completing 60% of the semester. Finish your classes? The grant money stays yours.

State grants follow similar rules. Complete the term, maintain satisfactory academic progress (usually 2.0 GPA minimum), and the money's yours permanently.

Scholarships stay yours if you meet renewal requirements. Lose your scholarship because your GPA dropped below 3.0? You don't repay what you already received, but future semesters become more expensive.

Work-study earnings are literally paychecks from a job. You're not borrowing anything. You work, you get paid, you spend it however you want.

The answer to "what part of aid must be repaid" should be the first thing you identify on any award letter. Some schools helpfully separate "gift aid" from "self-help aid." Others bury loans alongside grants under a generic "Your Financial Aid Award" heading, forcing you to read the fine print on every line item.

Financial Aid Package Explained

Award letters vary dramatically in clarity and honesty. School A might show your aid like this:

Total Cost: $35,000 - Federal Pell Grant: $6,500 - State Grant: $4,000

- Institutional Scholarship: $10,000 - Federal Direct Subsidized Loan: $3,500 - Federal Direct Unsubsidized Loan: $2,000

School B might show essentially the same package this way:

Total Financial Aid Award: $26,000! - Congratulations! We're pleased to offer you $26,000 in financial assistance!

See the problem? School B makes it sound like you're receiving $26,000 in help. Actually, you're receiving $20,500 in genuine assistance and being offered the opportunity to borrow $5,500.

When you get a financial aid package explained properly, it breaks down into three numbers that actually matter:

- True cost of attendance (everything you'll pay for the year—tuition, fees, room, board, books, supplies, travel, personal expenses)

- Actual gift aid (only grants and scholarships, nothing requiring repayment or work)

- Your remaining responsibility (true cost minus actual gift aid)

Using School A's example above: - True cost: $35,000 - Gift aid: $20,500 ($6,500 + $4,000 + $10,000) - Your remaining responsibility: $14,500

That $14,500 needs to come from somewhere. Your family contribution. Your savings. Summer job earnings. Outside scholarships you win. Work-study earnings during the semester. And yes, loans if absolutely necessary.

The award letter offered $5,500 in federal loans. Maybe you only need $3,500 after your family chips in $5,000 and you earned $6,000 over the summer. Borrow only the $3,500. The financial aid office doesn't care if you decline $2,000 of the offered loans—that's your decision.

Understanding Self-Help Aid

"Self-help aid" is a polite way of saying "money you need to generate yourself through work or borrowing." Sounds better in marketing materials than "money that's not really ours to give."

Work-study functions as self-help aid because the financial aid office doesn't hand you a check. They offer you access to part-time campus employment. You still need to find an available position, get hired, show up for shifts, and work enough hours to earn the full amount. Award letters might show $3,000 in work-study, but that's just earning potential. Work fifteen hours weekly at $12 per hour for twenty-eight weeks? You'll earn roughly $5,040 before taxes. Work only six hours weekly? You'll earn $2,016.

The self-help aid meaning becomes clearer when schools calculate your "unmet need." If your cost of attendance is $32,000, you receive $18,000 in gift aid, and you're offered $5,500 in loans plus $2,500 in work-study, schools might claim they "met your full need." Technically accurate, since $18,000 + $5,500 + $2,500 = $26,000, leaving only a $6,000 gap they expect your family to cover.

But did they actually meet your need? Not if you define "need" as "money that makes college affordable." They offered you the opportunity to borrow or work to bridge the gap. Whether that's truly meeting your need or just making it theoretically possible to attend is a philosophical question.

Understanding this distinction helps you evaluate whether a school is genuinely affordable or just accessible if you're willing to take on debt.

How to Calculate Your Out-of-Pocket Cost

Ignore everything labeled as a loan. Seriously, just cross it out mentally. Now look at what remains.

Author: Hannah Kingsley;

Source: nayiyojna.com

Start with the sticker price—the school's cost of attendance. Let's say $42,000 for this example.

Subtract every grant and scholarship: - Federal Pell Grant: $6,000 - State grant: $5,000 - University merit scholarship: $12,000 - Outside scholarship from local Rotary Club: $1,000 - Total gift aid: $24,000

Your actual cost just dropped from $42,000 to $18,000. That's the number that matters.

Now assess your available resources: - Expected family contribution (what your parents saved/can pay): $8,000 - Your summer earnings: $3,500 - Available resources: $11,500

The gap you need to fill: $6,500.

At this point, you make strategic decisions. You could: - Accept a $3,500 federal subsidized loan and earn $3,000 through work-study - Accept a $5,500 federal subsidized loan and earn $1,000 through a regular part-time job - Spend another month applying for five more scholarships, potentially winning enough to eliminate the gap entirely - Ask your parents to pay an extra $2,000 if possible, reducing your borrowing to $4,500

Notice what we didn't do? Accept the full $12,500 in federal loans just because the award letter offered that amount. Most students see loans on their award letter and assume they should accept everything offered. That's how students graduate with $35,000 in debt when they only actually needed $15,000.

The cost calculation reveals your true financial obligation. Everything else is just noise.

Common Financial Aid Mistakes to Avoid

I spend half my time explaining to families that aid packages are starting points for negotiation, not final offers. If your financial situation changed, if another school offered more, if you've won outside scholarships—tell us. We can often adjust. But I also spend the other half explaining that loans aren't actually aid in any meaningful sense. We include them in packages because we're required to show students all available options, but accepting maximum loans is almost never the right choice

— Robert Chen

Treating loans like aid instead of debt. This one comes first because it's the most expensive mistake. You see "$8,000 Federal Direct Loans" listed under "Your Financial Aid" and your brain files it alongside grants. Five years later, you're making $280 monthly payments and wondering why college felt affordable until it wasn't.

Ignoring subsidized vs. unsubsidized differences. You need to borrow $4,000. The award letter offers $3,500 subsidized and $2,000 unsubsidized. Take only the $3,500 subsidized, then find the remaining $500 elsewhere. That $500 saved from unsubsidized loans saves you roughly $125 in interest charges over ten years. Small potatoes? Now multiply that logic across four years and you're saving $500+ total.

Not comparing the actual cost between schools. School X costs $55,000 but offers $40,000 in grants and scholarships—actual cost $15,000. School Y costs $28,000 but offers only $8,000 in grants and scholarships—actual cost $20,000. School X is cheaper despite the higher sticker price, but you'd never know that by comparing published tuition rates.

Accepting Parent PLUS Loans without exploring alternatives. Financial aid offices include PLUS loans in packages as though they're standard aid. They're not. These are high-interest loans your parents take on. Before your family borrows $12,000 per year through PLUS loans, exhaust every alternative: your own federal loans, payment plans spreading costs across monthly installments, choosing a less expensive school.

Losing renewable scholarships due to ignorance. Your university offered $8,000 yearly, renewable for four years provided you maintain a 3.25 GPA. You finish freshman year with a 3.1 GPA. The scholarship disappears. Sophomore year just got $8,000 more expensive, forcing you to borrow what you could have kept free. Read the scholarship requirements. Understand exactly what GPA, credit hours, or activities you must maintain. Losing a scholarship creates an emergency.

Skipping scholarship applications out of laziness. This one hurts because it's so preventable. "I'll never win" becomes a self-fulfilling prophecy. Meanwhile, students who apply for fifteen scholarships win three totaling $6,500. Those students graduate with $6,500 less debt. The application process takes time—but so does working enough hours at a minimum-wage job to earn $6,500 after taxes (roughly 520 hours, or thirteen full-time weeks).

Treating work-study as guaranteed money. Award letter shows $2,800 in work-study. You budget accordingly. September arrives. The good positions already filled. You find a job offering six hours weekly instead of the ten you needed. You'll earn only $1,680, not $2,800. Suddenly you're short $1,120. Work-study represents opportunity, not certainty. Budget conservatively.

Types of Financial Aid at a Glance

| Type of Aid | Requires Repayment? | Awarded Based On | Where It Comes From | Annual Amount Range | How to Apply |

| Pell Grants | No | Financial need | U.S. Department of Education | $750–$7,395 | FAFSA only |

| State Grant Programs | No | Financial need | State education departments | $500–$6,000+ depending on state | FAFSA plus possible state application |

| College Scholarships | No | Merit, need, or combination | The institution's own funds | $1,000–complete tuition coverage | Admission application and/or separate scholarship forms |

| Outside Scholarships | No | Varies widely—merit, identity, interests, random selection | Private organizations, companies, foundations, community groups | $250–$10,000+ | Individual applications for each scholarship |

| Federal Work-Study | No (you're paid for hours worked) | Financial need | Federal funding administered by schools | $1,500–$5,000 earning potential | FAFSA only |

| Subsidized Direct Loans | Yes, with interest | Financial need (undergrads only) | U.S. Department of Education | $3,500–$5,500 based on year in school | FAFSA plus entrance counseling |

| Unsubsidized Direct Loans | Yes, with interest | No need requirement | U.S. Department of Education | $5,500–$20,500 including any subsidized amounts | FAFSA plus entrance counseling |

| Parent PLUS Loans | Yes, with interest | No need requirement | U.S. Department of Education | Up to full cost of attendance minus other aid | FAFSA plus separate PLUS application and credit check |

| Private Student Loans | Yes, with interest | No need requirement | Banks, credit unions, online lenders | Varies by lender and credit approval | Direct application through lender, credit check required |

Frequently Asked Questions

Financial aid functions as an umbrella covering both genuine assistance and marketed debt products. The system intentionally obscures this distinction. Schools that list "$32,000 in financial aid!" know most families won't immediately realize that $20,000 of that figure represents loans requiring repayment with interest.

Your defense against this marketing tactic? Ruthless categorization. Every time you see an aid package, perform the same analysis: What's actually free? What requires working? What requires borrowing? The first category reduces your real cost. The second category requires time and effort. The third category creates debt that follows you into your career.

Students who graduate with manageable debt levels—or no debt—typically made smarter decisions before freshman year started, not after. They maximized applications to schools offering substantial merit aid. They spent summer before senior year applying for twenty or thirty private scholarships. They chose colleges where their academic credentials placed them in the top 25% of admitted students, making them attractive candidates for institutional scholarships. They understood their financial aid packages completely before accepting anything.

You have more control over college costs than the system wants you to believe. Schools present aid packages as take-it-or-leave-it offers. They're not. You can negotiate. You can decline loans. You can appeal for more grant funding if circumstances changed. You can choose a less expensive school offering better aid over a prestigious school offering mostly loans.

Decades from now, you won't remember whether you carried $0 in debt or $50,000 in debt because you'll have paid it off either way. But you'll remember it every month during those decades when loan payments hit your bank account. The difference between understanding your aid package now and figuring it out later is the difference between financial freedom and financial stress throughout your twenties and thirties.

Separate free money from borrowed money. Make decisions based on that distinction. Your future self will thank you