Person holding insurance cards and checking a policy number on a smartphone

What Is an Insurance Policy Number and Where to Find It

Content

Ever fumbled through your wallet at the pharmacy counter, desperately searching for that string of numbers the clerk needs? Or sat on hold with a medical office because you couldn't rattle off your policy information? That alphanumeric sequence printed on your insurance card matters more than most people realize—until they urgently need it.

These identification codes connect you to your coverage. Without them, you're looking at delays, rejected claims, and frustrated phone calls. Miss an appointment because you couldn't verify coverage? That happens more often than you'd think.

Let's fix that problem. Here's everything you need to know about tracking down and using these critical numbers.

What Is an Insurance Policy Number?

Think of this number as your coverage's social security number. Every insurance contract gets assigned its own unique code—a combination of letters, numbers, or both. Your insurer uses this code to pull up everything about your coverage: what's included, what's excluded, your deductibles, your payment history, past claims.

Last month, three patients postponed surgeries at our facility—medically necessary procedures—simply because they couldn't provide accurate policy information during pre-authorization.We're talking knee replacements, cardiac catheterizations. The insurance would've covered it. But without the right numbers, we couldn't get authorization in time for their scheduled dates

— Michael Torres

This code does heavy lifting behind the scenes. When your dentist's office submits a bill for your crown, that policy number tells the insurance computer exactly which contract to charge against. When the auto body shop checks whether you have collision coverage after a fender bender, they're looking up your specific policy details using that number.

Here's where people get confused: these numbers work differently depending on your coverage type. Got insurance through your job? That policy number probably covers your entire company's plan—hundreds or thousands of employees. Your individual member ID then identifies you specifically within that group plan. Bought auto insurance on your own? Your policy number is unique to just your vehicles and coverage.

The number sticks with your contract. Keep the same health plan through work for five years? Same policy number. Buy a six-month auto policy and renew it? Usually the same number (maybe with a new suffix to show the renewal period). Switch to a different plan or carrier? You'll get a fresh number.

Different insurance types structure these codes differently. Health plans often use longer strings—10 to 13 characters—because they're tracking group arrangements and multiple dependents. Auto policies might run shorter. Life insurance keeps it simple since each contract covers one person. Your homeowners policy might include letters indicating your coverage type (HO-3, HO-6) right in the number itself.

Author: Brandon Ellery;

Source: nayiyojna.com

Where to Find Your Insurance Policy Number

Most insurers give you multiple ways to access this information. Smart move: check all these locations and save the number somewhere you'll actually remember.

On Your Insurance Card

Start here. Flip out your insurance card right now. For health coverage, scan the front side first. Look for labels like "Policy #," "Group Policy Number," "Contract Number," or just "Policy." Some carriers print it on the back instead—apparently to keep you on your toes.

Your auto insurance card (that paper or digital proof you're legally required to carry while driving) displays the policy number front and center. It's usually near the top, alongside your coverage start and end dates. Progressive uses one format, State Farm uses another, but they all put it somewhere obvious.

Homeowners coverage doesn't typically come with a wallet card. But your declarations page—that multi-page summary of your coverage—puts the policy number right at the top. You received this when you bought the policy and again at each renewal.

Author: Brandon Ellery;

Source: nayiyojna.com

In Your Policy Documents

Buried in paperwork? Your full policy packet includes that number on practically every page, usually in the header or footer. The declarations page I just mentioned is part of this packet.

Remember that welcome packet you got when first enrolling? Policy number's in there, typically on page one. Insurance companies also print it on regular correspondence—billing statements, coverage change confirmations, renewal notices. Check the upper right corner of any letter from your insurer.

Through Your Insurer's Mobile App or Online Portal

Download your carrier's app. Seriously, do it now. After logging in, your policy number appears on the home screen or account overview. No digging required.

Most apps let you view a digital insurance card. Screenshot it. Save it to your phone's photo album. Add it to your digital wallet if your phone supports that. Then you've got instant access whether you're at the ER at 2 AM or getting pulled over for a broken taillight.

On Explanation of Benefits Statements

Filed an insurance claim recently? Your EOB (that confusing document explaining what the insurance paid and what you owe) lists your policy number in the header section. These arrive by mail or email after any claim gets processed.

Haven't used your coverage lately? Then EOBs won't help. But if you visited a doctor last month and misplaced your card since then, check your recent mail or email for those EOB statements.

Policy Number vs Group Number vs Member ID

Insurance cards throw multiple numbers at you. Use the wrong one and the pharmacy's system can't find your coverage. Here's the breakdown:

| Policy Number | Group Number | Member ID | Subscriber ID |

| What it identifies: The insurance contract itself (individual or group plan) | What it identifies: Your specific employer or organization within a large insurer's book of business | What it identifies: You as an individual person receiving coverage | What it identifies: The primary employee who provides the coverage (might be you or your spouse) |

| Who uses it: Everyone under the same employer plan shares this number; individual plans assign one per person | Who uses it: All workers and family members under the same company plan | Who uses it: Each covered person gets their own unique identifier | Who uses it: Only the main policyholder gets this designation |

| Where it appears: Front or back of insurance card, policy paperwork, online account home page | Where it appears: Insurance card (check near "Group #" or "Grp") | Where it appears: Insurance card, often labeled "ID Number" or "Member Number" | Where it appears: Policy documents, sometimes on cards for employer plans |

| Common formats: Mix of letters and numbers, typically 8-15 characters, may include hyphens | Common formats: Usually all numbers, often 5-8 digits long | Common formats: Often the subscriber ID with a suffix added (like 00 for primary, 01 for spouse, 02 for first child) | Common formats: Alphanumeric string, 8-12 characters |

| Sample: H12345678 or ABC123456789 | Sample: 12345 or 0067890 | Sample: ABC12345600 (base number plus 00) | Sample: ABC123456 |

Employer health plans hand you all four numbers. Gets confusing fast. Your policy number represents your company's entire agreement with the insurer. The group number pinpoints your specific company (matters when insurers manage thousands of different employer groups). Your member ID singles you out. The subscriber ID shows which family member actually works for the company providing coverage.

When calling to make a doctor's appointment, they'll usually want your member ID first. But if there's confusion verifying benefits, they might ask for the group or policy number next. Keep all four numbers accessible.

Author: Brandon Ellery;

Source: nayiyojna.com

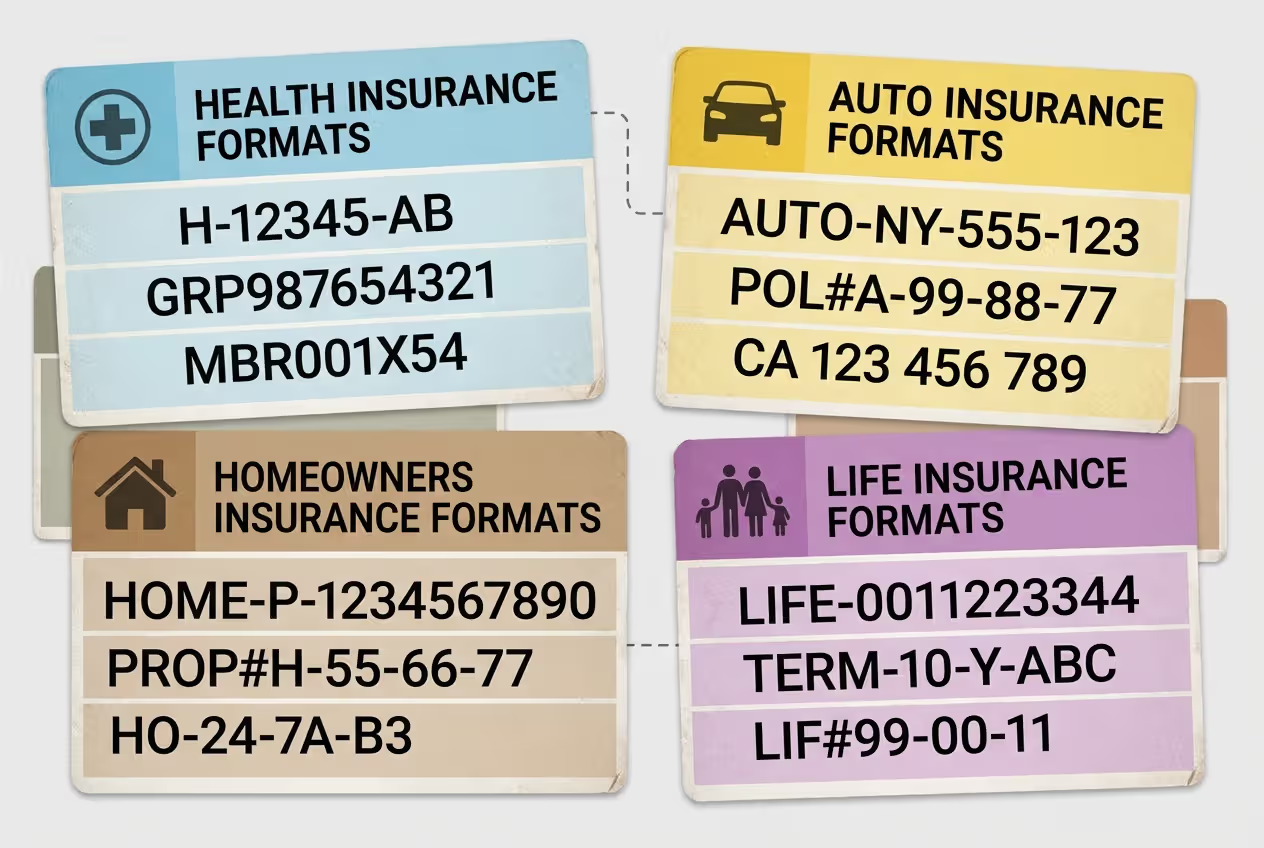

Insurance Policy Number Format and Examples

No industry standard exists for formatting these numbers. Each company invents its own system. But patterns emerge once you look at enough examples.

Health Insurance Samples: - Anthem Blue Cross member working for a tech company: W234567890 (letter W prefix followed by nine digits) - Kaiser Permanente Northern California: 12345000 (eight digits, last two zeros indicate primary member) - Medicare Advantage plan: 1EG4TE5MK73 (seemingly random letters and numbers—Medicare uses these complex codes)

Employer health plans pack information into those numbers. Early digits might indicate which employer, middle digits might show the plan type (PPO vs HMO), later digits might reflect the coverage tier. Individual marketplace plans use simpler formats since they're not juggling multiple employers.

Auto Insurance Samples: - Geico policy covering two vehicles: 1234567890 (ten straight digits, clean and simple) - State Farm policy in California: 01-AB-C234-5 (includes territory codes and policy identifiers) - Liberty Mutual policy: POL123456789-2024 (prefix showing it's a policy, then digits, then year)

Auto policies sometimes build in information about your renewal cycle. Add a third vehicle and you might see a letter change. Renew for another term and a suffix gets updated. The core number typically stays constant.

Homeowners Insurance Samples: - Allstate homeowners in Florida: 12-HO-3456789 (year issued, coverage type code, unique identifier) - Farmers condo policy: HO6-987654-26 (HO-6 indicates condo coverage form, then number, then abbreviated year) - USAA policy: 12345678HO3 (base number plus coverage form at the end)

Homeowners policies love including those HO codes. HO-3 means special form coverage (the most common type). HO-6 covers condos. HO-4 is renters insurance. Seeing these codes in your policy number actually tells you something useful.

Life Insurance Samples: - Northwestern Mutual whole life policy: L12345678 (L for life insurance, followed by eight digits) - Term life from Haven Life: 1234567890 (straightforward ten-digit number) - Variable universal life policy: VUL-987654321 (type indicator included)

Life insurance keeps it simpler. You're one person with one contract. No need for complex group structures.

Length varies wildly—I've seen seven-character policy numbers and fifteen-character monsters. Some use only numbers. Others mix letters and numbers. Hyphens and spaces may appear, though online systems usually let you skip them when typing the number in.

When You Need to Provide Your Policy Number

This number comes up in more situations than you'd expect. Some routine, some stressful. Here's when you'll need it:

Submitting Claims: Mandatory, non-negotiable. Health claim for your kid's broken arm? Policy number required. Auto claim after someone rear-ended you at a stoplight? Policy number required. Home claim after a pipe burst and flooded your basement? Policy number required. Claims literally cannot process without it—the insurer's system needs to confirm coverage was active when the incident happened.

Booking Doctor's Appointments: Most offices verify benefits before you show up. The scheduler will ask for your insurance details over the phone. They need your member ID for sure, often the group or policy number too. This tells them your copay amount and whether your plan covers that specific provider. Skip this step and you might get stuck paying full price at checkout, then filing for reimbursement later (annoying and time-consuming).

Emergency Room Situations: ERs legally must treat you regardless of insurance status. But you definitely want to provide your policy information so bills get filed correctly. Otherwise you'll receive statements as if you're uninsured, showing astronomical charges. Then you'll spend weeks on the phone sorting it out retroactively.

Pharmacy Prescription Pickup: Your pharmacist needs to run your insurance to determine your copay. Usually your member ID handles this. But if their system can't find your coverage, they'll ask for the policy or group number to troubleshoot. Without insurance running properly, a $10 prescription might ring up at $150.

Changing Your Coverage: Got married? Having a baby? Divorced? These life events trigger a special enrollment period where you can modify coverage. You'll need your policy number to access your account and make these updates. Miss the window and you're waiting until next year's open enrollment.

Proving Coverage to Third Parties: Mortgage lenders require proof of homeowners insurance before closing. Auto loan companies want confirmation you're carrying collision coverage. Landlords often demand renters insurance. These parties need your policy number to verify coverage meets their requirements—correct property address, adequate coverage limits, proper liability amounts.

Modifying Policy Details: Raising your auto coverage limits? Lowering your homeowners deductible? Adding an umbrella policy endorsement? Customer service needs your policy number to pull up your contract and quote the changes.

Creating Online Accounts: First-time registration on your insurer's website typically requires your policy number for identity verification. Once you're set up, you can usually log in with just email and password.

Resolving Billing Problems: Received a bill for a service you thought was covered? Balance looks wrong? Customer service representatives need your policy number to investigate. They'll pull up your claims history, check your coverage terms, and explain what happened.

Switching Primary Care Doctors: HMO plans make you designate a primary care physician who coordinates everything. Changing that designation requires your policy information so the insurer can update your records.

Store this number somewhere practical. Take a photo of your insurance cards and keep it in a "Medical Info" album on your phone. Type the number into your phone's notes app with a clear label. Write it on an index card in your wallet. Text it to your spouse. The three minutes spent doing this now saves you from panicking when the dentist's receptionist asks for it while you're sitting in traffic on your way to an appointment.

Author: Brandon Ellery;

Source: nayiyojna.com

What to Do If You Can't Find Your Policy Number

Cards get lost. Emails get deleted. Documents get shoved in drawers and forgotten. Don't panic—you have options.

Call Your Insurer's Customer Service Line: Fastest solution. Have your personal details ready: full legal name, date of birth, Social Security number, current address. The rep verifies your identity and reads off your policy number within two minutes. Most insurers also offer chat support if you hate phone calls.

Search Your Email Inbox: Open your email. Search for your insurance company's name. Try searches like "welcome," "enrolled," "confirmation," "policy," "coverage begins." Your initial enrollment almost certainly arrived via email, and that message included your policy number. If you've had the policy for years, scroll back to messages from your enrollment date.

Log Into Your Online Account: Already registered on your insurer's website but blanking on your policy number? Log in with your username and password. The dashboard displays it immediately. Forgot your password? Reset it—the password recovery process verifies identity through email or phone, not policy number.

Contact Your Insurance Agent or Broker: Bought coverage through an agent instead of directly? That agent keeps your information on file. Call or email them. They'll reply with your policy number in minutes. This is literally part of their job.

Ask Your HR Department: Work-provided health insurance? Your benefits coordinator has all employee policy information. Send them a quick email or stop by their office. They manage enrollment files and can look up your details instantly.

Check Recent Medical Bills or EOB Statements: Used your health coverage in the past few months? Dig through your mail pile or email for those EOB statements or medical bills. Both include policy information. Even an old bill from six months ago works—policy numbers rarely change mid-year.

Review Bank or Credit Card Statements: Pay insurance premiums yourself? Your bank statement shows payments to the insurance company. That confirms which insurer you're using, making it simple to call their customer service line for your policy number.

Visit a Local Office: Some insurance companies maintain physical offices where you can walk in and talk to someone face-to-face. Bring your driver's license or another photo ID, plus any insurance-related papers you managed to find. They'll look up your information on the spot.

Request a Replacement Card: Most insurers mail replacement cards within three to seven business days. Some offer expedited shipping. Many can email you a temporary digital card within hours.

What if you need medical care right now, before tracking down that number? Many providers will see you and file claims later if you can give them your insurer's name, your date of birth, and your Social Security number. They'll note "pending insurance verification" on your chart. But you're potentially on the hook for full charges if they can't successfully file that claim later, so follow up with the correct policy number ASAP.

Author: Brandon Ellery;

Source: nayiyojna.com

Frequently Asked Questions About Insurance Policy Numbers

That string of letters and numbers on your insurance card does more work than most people realize. It's your access key to coverage, your claim ticket when things go wrong, your proof that you're protected when verification is required.

Stop right now and locate your policy numbers for every insurance type you carry. Photograph those cards. Type the numbers into your phone. Store them in a password-protected note. Tell your spouse or partner where to find this information if they need it in an emergency. Spending five minutes on this task now prevents hours of frustration when you're stressed and need quick access.

Your policy number is one piece of a larger puzzle. Learn what coverage your policy actually provides. Know your deductibles. Understand whether you need referrals to see specialists. Save your insurer's customer service number in your phone contacts. Being organized with insurance information means you can navigate claims, appointments, and coverage questions confidently instead of frantically scrambling every time someone asks for details.

Protection only works when you can prove you have it. Keep these numbers handy.