Family standing near home and car with insurance documents and symbolic umbrella

Insurance Umbrella Policy Guide

Here's something most people don't realize until it's too late: your car insurance and homeowners policy probably won't protect you from a major lawsuit. Got $300,000 in auto liability coverage? Sounds like plenty—until someone suffers a traumatic brain injury in an accident you caused, racks up $800,000 in medical bills, loses their $120,000 annual income permanently, and sues you for $2.5 million.

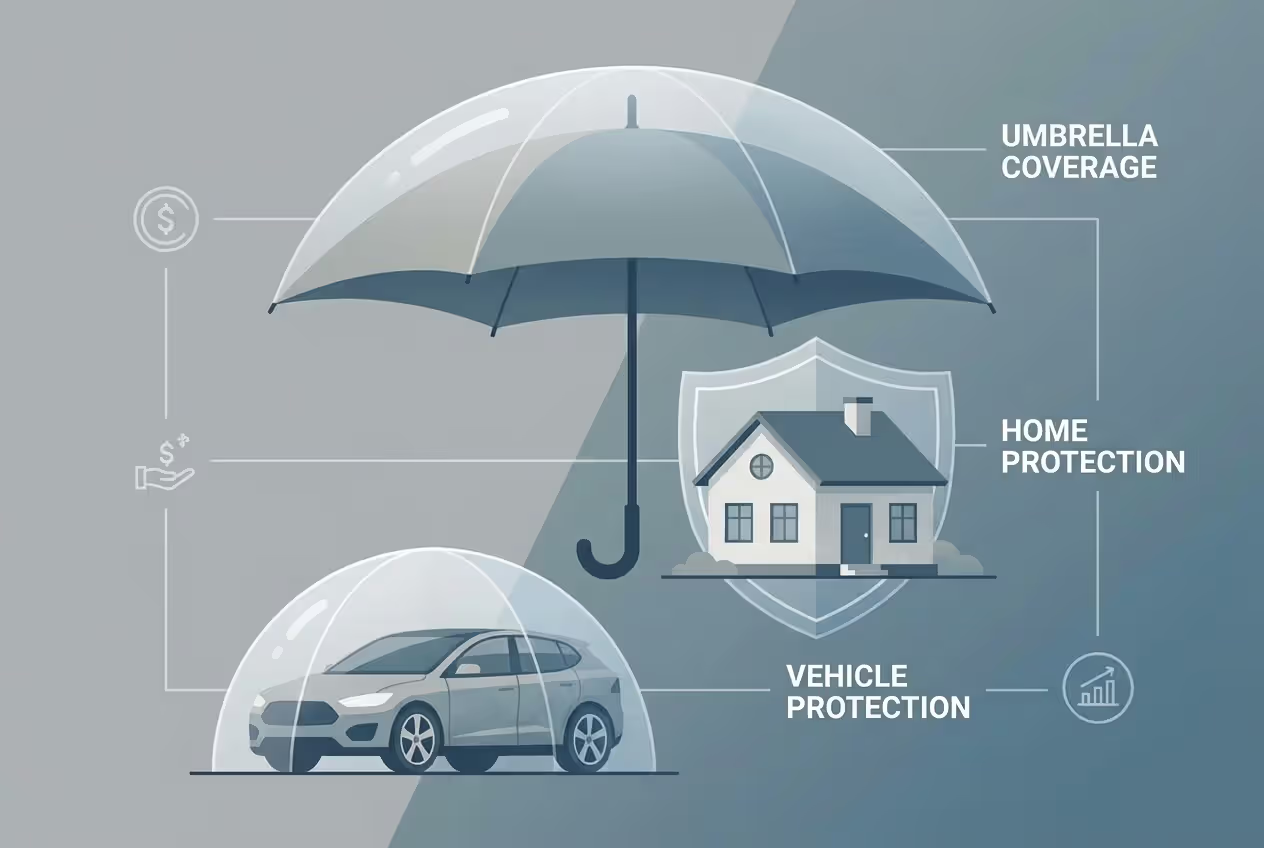

That's where an insurance umbrella policy comes in. It picks up where your regular policies stop, covering liability claims that blow past your standard limits.

Consider what happened to a Seattle family in 2019. Their teenage son caused a three-car pileup that left two people with serious injuries. The resulting lawsuit demanded $1.8 million. Their auto policy maxed out at $500,000. Without their $2 million umbrella policy, they would've lost their home, retirement accounts, and faced wage garnishment for years.

These policies typically start at $1 million in coverage and scale up to $10 million or higher. They work across all your insurance—cars, home, boats, rental properties. And here's the part that surprises people: that first million dollars of protection usually costs between $150 and $300 per year. You're spending less than a dollar a day to safeguard everything you own.

The mechanics are straightforward. Let's say your auto insurance covers up to $300,000 in liability, but a court holds you responsible for $1.5 million in damages. Your car insurance pays its $300,000 maximum. Your umbrella policy handles the remaining $1.2 million (after you pay a small deductible, typically $250-$500). Without that umbrella coverage, you'd personally owe $1.2 million—enough to bankrupt most families.

What makes these policies especially valuable: one umbrella policy extends over multiple insurance types. It provides backup for your auto insurance, homeowners coverage, boat policy, and certain personal situations your other policies won't touch.

Author: Matthew Redford;

Source: nayiyojna.com

What an Umbrella Policy Covers

Most umbrella claims stem from bodily injury situations where someone gets seriously hurt and you're liable. Picture this: you're hosting a dinner party, someone trips on your uneven patio, falls down concrete steps, and suffers a spinal injury requiring three surgeries. The medical costs alone hit $400,000. Then there's physical therapy for two years, permanent disability payments, lost earnings from their $85,000-a-year job, and pain and suffering. Your homeowners liability might cover $300,000. The remaining $600,000-plus? That's why you need umbrella coverage.

Car accidents represent another common scenario. You run a red light and T-bone an SUV carrying a family of four. Two passengers need extensive reconstructive surgery. One develops chronic pain requiring lifetime treatment. Between emergency care, ongoing medical needs, income replacement, and compensation for reduced quality of life, damages can easily exceed seven figures.

Property damage liability extends beyond fender benders. A contractor friend once accidentally knocked over a scaffolding that crashed through a neighbor's roof, destroying not just the structure but also $75,000 worth of antique furniture and collectibles inside. Your tree could fall on someone's house during a storm, destroying their roof and everything underneath. You might back your truck into a classic Porsche at a car show. These aren't hypothetical—they happen every day.

Personal liability coverage under umbrella policies catches situations most people never anticipate. Your German Shepherd bites a jogger who needs facial reconstruction surgery and psychological counseling, generating $200,000 in claims. Your kid accidentally knocks another child off playground equipment, causing a severe concussion with long-term complications. You're volunteering at a school event and accidentally damage expensive video equipment. All covered.

Here's something that catches people off guard: legal defense expenses get paid on top of your policy limits, not subtracted from them. Defending a serious liability lawsuit can cost $75,000 to $200,000 before you ever get to trial—depositions, expert witnesses, motions, discovery. Even if you win, those costs add up. Your umbrella policy covers them separately, which means your $1 million policy actually provides more like $1.2 million in total protection once legal fees are factored in.

Defamation, libel, and slander claims have become increasingly relevant. Post the wrong thing on Facebook about a local business, and you might face a six-figure defamation suit. Repeat gossip that turns out to be false and damages someone's professional reputation. Make accusations online that you can't prove. Your homeowners policy might offer $1,000-$5,000 for these situations. Your umbrella policy covers substantial claims—and the legal costs to defend them.

Landlords benefit from coverage for false arrest, wrongful eviction, malicious prosecution, and privacy violations. Evict a tenant improperly, and you're looking at potential legal action. Your umbrella policy responds to these claims in ways your landlord policy might not.

Umbrella Policy vs Liability Coverage

Author: Matthew Redford;

Source: nayiyojna.com

Your existing policies provide the first line of defense. Umbrella coverage functions as your backup plan—but only after you've used up your primary protection.

Think of it like this: your auto policy covers the first $250,000 or $500,000 of liability from a car accident you cause. Your homeowners policy handles the first $100,000 to $500,000 for injuries on your property or personal liability incidents. These policies respond immediately when something goes wrong. They're your frontline coverage.

Umbrella insurance sits in reserve. It activates only after your primary coverage hits its maximum payout. That's why insurers call it "excess liability coverage"—it covers the excess above what your other policies will pay.

Here's a real-world example: you cause an accident that injures multiple people, resulting in $1.3 million in total damages. Your auto policy carries $300,000 in liability coverage. It pays out its full $300,000. Now you're still on the hook for $1 million. Your umbrella policy covers that remaining million. Without it, that's coming out of your personal assets—bank accounts, investment portfolios, home equity, even future wages.

| Coverage Type | Auto Liability (Standard) | Homeowners Liability (Standard) | Umbrella Coverage |

| Coverage Amounts | $100,000 to $500,000 per incident | $100,000 to $500,000 per claim | $1 million to $10 million+ |

| Protection Included | Vehicle-related accidents where you're at fault | Property injuries, personal liability events | Secondary coverage across all policies, plus scenarios primary insurance excludes |

| What You'll Pay | $800 to $2,000 yearly (highly variable) | Built into your homeowners premium | $150 to $500 annually per million |

| Activation Point | Responds immediately to covered claims | Responds immediately to covered claims | Kicks in after primary coverage exhausted |

Before any carrier will sell you umbrella coverage, they'll require minimum liability limits on your underlying policies. You'll typically need at least $250,000 per person/$500,000 per accident on your auto insurance, plus $300,000 in homeowners liability. Some insurers demand even higher minimums—$500,000 across the board isn't uncommon. This ensures you're not using expensive umbrella coverage for smaller claims that your primary policies should handle.

The coverage scope differs significantly. Your car insurance only covers vehicle incidents. Your homeowners policy addresses property-related events and general personal liability. Umbrella coverage spans everything—auto, home, boats, recreational vehicles—and includes additional scenarios like defamation that your other policies might exclude entirely.

One quirk worth knowing: when your umbrella policy responds to a claim that doesn't involve an underlying policy—say, a slander lawsuit that your homeowners policy won't cover—you'll pay a deductible (usually $250-$500). But when it's extending your auto or homeowners coverage, there's typically no additional deductible since you've already met your primary policy's deductible.

Umbrella Insurance Coverage Limits Explained

Choosing the right coverage amount requires honest assessment of what you could lose in a worst-case scenario. Carriers typically offer policies starting at $1 million, jumping in $1 million increments to $5 million, with higher amounts available for high-net-worth individuals.

The standard advice suggests matching your coverage to your net worth. Own a home with $600,000 in equity? Have $400,000 in retirement accounts and another $150,000 in taxable investments? That's $1.15 million in assets that could disappear after a major judgment. A $1-2 million umbrella policy makes sense.

But that formula misses something crucial: your future earning power. If you're 38 years old earning $125,000 annually, you'll potentially earn over $3 million before retirement (not accounting for raises). Courts can garnish your wages for years to satisfy a judgment. A young attorney or physician with decades of high income ahead might need $3-5 million in coverage despite having modest current assets.

Risk factors matter too. Own rental properties? Each one multiplies your exposure. Teenage drivers in your household? Accident rates for 16-19 year-olds run three times higher than drivers over 25. Coach youth sports, sit on nonprofit boards, or maintain an active social media presence with thousands of followers? Your likelihood of facing liability claims increases.

| Coverage Amount | Annual Premium Range | Best Fit For |

| $1 million | $150 to $300 | Net worth $500K to $1M, standard risk profile |

| $2 million | $250 to $425 | Net worth $1M to $2M, above-average assets |

| $5 million | $425 to $750 | Net worth over $2M, multiple properties, or elevated risk exposure |

| $10 million | $850 to $1,600 | Substantial wealth, significant business holdings, high-profile individuals |

The pricing structure heavily favors buying more coverage. Your first million costs $150-$300. Each additional million typically adds just $50-$100. You can jump from $1 million to $3 million in coverage for maybe $100 extra per year. That's less than $10 monthly for an additional $2 million in protection.

Several factors influence your specific rate. Location matters—living in litigation-heavy states like California, Florida, or New York costs more. Your driving record plays a role; multiple tickets or accidents in the past five years increase rates. Property features like pools, trampolines, or aggressive dog breeds affect pricing. Interestingly, maintaining higher liability limits on your underlying policies can actually reduce your umbrella premium, since it lowers the insurer's overall risk exposure.

Bundling creates significant savings. Keeping your umbrella, auto, and homeowners coverage with the same carrier typically generates 10-25% discounts across all three policies. You might pay $1,800 for auto and homeowners coverage separately, but bundling could drop that to $1,500—a $300 annual savings that more than covers your umbrella premium.

The cost of inadequate coverage far exceeds any premium savings. Carrying $1 million when you face a $2.8 million judgment leaves you personally liable for $1.8 million. That kind of shortfall can mean bankruptcy, loss of your home, retirement savings wiped out, and decades of wage garnishment. Spending an extra $75-$150 annually to double your coverage makes the underinsurance risk inexcusable.

Author: Matthew Redford;

Source: nayiyojna.com

What Umbrella Policies Don't Cover

Umbrella coverage offers broad protection, but important gaps exist that catch people unprepared.

Deliberate harmful acts won't trigger coverage. Punch someone during a road rage incident? Intentionally vandalize a neighbor's property? Commit assault? You're on your own. Insurance companies won't protect you from consequences of criminal behavior or actions you meant to cause harm. Courts have ruled that even if you only intended to scare someone but caused serious injury, you may not have coverage if the act itself was deliberate.

Business-related liability requires completely separate coverage. Running a consulting business from your home office? Providing freelance services? Operating an Airbnb or managing multiple rental properties (usually more than three or four units)? Standard umbrella policies exclude these commercial activities. You'll need a commercial general liability policy or business owners policy. This exclusion extends to side hustles—that Etsy shop or weekend photography business needs its own liability coverage.

Your own property damage falls outside umbrella protection. These policies cover your liability for damaging other people's stuff, not your own. Back your car into your own garage door? Accidentally drop your laptop? Those losses fall under your property insurance (homeowners, auto comprehensive), not liability coverage.

Contractual obligations you voluntarily assume often aren't covered. Sign a venue rental agreement where you agree to indemnify the property owner for any incidents? Accept full liability in a business contract? Your umbrella policy likely won't cover those assumed liabilities. Read contracts carefully before signing away your protections.

Workers' compensation situations need dedicated coverage. Employ a nanny, housekeeper, or landscaper? If they're injured while working for you, your umbrella policy won't respond. State laws typically mandate workers' compensation insurance for household employees—even part-time ones. Penalties for non-compliance can be severe.

Property in your custody may not be covered when damaged. Borrowing your friend's $4,000 camera lens and dropping it? Storing your sister's antique furniture and discovering water damage? These "care, custody, and control" exclusions appear in most umbrella policies. Some homeowners policies offer limited coverage for borrowed property, but don't assume your umbrella extends here.

Professional mistakes and malpractice require errors and omissions or professional liability coverage. Physicians, attorneys, accountants, architects, real estate agents, and other licensed professionals face malpractice exposure that umbrella policies specifically exclude. If you provide professional services—even informally—you need specialty coverage for that work.

Certain recreational vehicles like ATVs, dirt bikes, and jet skis may be excluded, though some carriers offer endorsements to add them back. Aircraft ownership typically demands standalone aviation liability insurance—only the highest-tier umbrella policies include any aircraft coverage, and it's usually quite limited.

When Umbrella Insurance Is Worth It

The question isn't whether umbrella coverage provides value—it's whether your situation demands it.

Substantial assets make you a lawsuit target. Once your net worth exceeds $500,000—and that includes home equity, retirement accounts, investment portfolios, savings—you have enough wealth to make litigation worthwhile for plaintiffs' attorneys. Someone suffering serious injuries in an accident you caused will investigate your financial situation. Their attorney will discover your assets. Without umbrella protection, you're risking everything.

I tell clients that umbrella insurance is the first coverage you should never skimp on. I've worked with three families over the past decade who faced lawsuits exceeding $1 million—one from a car accident, one from a pool drowning, one from their dog. The two families with umbrella policies survived financially intact. The family without it lost their retirement savings and nearly lost their home. For $300 a year, that's unconscionable

— Michael Thornton

Rental property ownership dramatically increases exposure. Landlords face liability for tenant injuries, slip-and-falls on rental property, discrimination claims (even unintentional ones), wrongful eviction suits, and premises liability issues. A single rental property justifies umbrella coverage. Multiple properties make it essential. Standard landlord policies offer limited liability—often just $300,000-$500,000. That won't cover a catastrophic injury on your property.

Young or inexperienced drivers in your household multiply accident risk exponentially. Statistics from the Insurance Institute for Highway Safety show drivers aged 16-19 have crash rates nearly four times higher than drivers 20 and older. Letting your 17-year-old daughter drive to school? The moment she gets her license, your liability exposure skyrockets. A serious accident she causes becomes your financial liability. The $200-$300 umbrella premium looks incredibly cheap compared to potential seven-figure exposure.

Visible public roles increase certain liability risks. Active on Twitter with 15,000 followers? Serve on your HOA board? Coach youth soccer? Volunteer as a Girl Scout troop leader? These roles increase your exposure to defamation claims, accusations of improper conduct, and personal liability situations. Umbrella policies cover many scenarios your homeowners policy won't touch.

Attractive hazards on your property warrant additional protection. Swimming pools, trampolines, tree houses, or aggressive dog breeds all increase injury likelihood. Many insurers won't even write homeowners coverage for certain dog breeds (pit bulls, Rottweilers, Akitas) without requiring umbrella coverage. A child drowning in your pool or suffering traumatic injuries from your dog creates massive liability—the kind that exceeds standard policy limits.

High income earners should protect future wages even with modest current assets. Earning $175,000 annually at age 35? You'll potentially earn $5+ million before retirement. Courts can garnish 25% of your disposable earnings to satisfy judgments in most states. Losing $40,000-$50,000 annually for a decade or more devastates your financial life. Your future earning power deserves protection just like your current savings.

You might reasonably skip umbrella coverage if you: rent your home, don't own vehicles, have minimal assets (under $100,000), maintain a very low-risk lifestyle, and have limited future income potential. Even then, carrying $1 million costs so little that it's worth considering.

For everyone else—homeowners, families with children, anyone with assets to protect—umbrella insurance delivers exceptional value. You're spending $0.50-$1.00 daily to safeguard decades of financial progress.

Author: Matthew Redford;

Source: nayiyojna.com

How to Buy an Umbrella Policy

Purchasing umbrella coverage follows a logical sequence, though you'll need to meet specific requirements before carriers approve your application.

Start by auditing your current liability limits. Pull out your auto and homeowners policy declarations pages. Look for your liability coverage amounts. Most insurers won't issue umbrella coverage unless you're carrying at least $250,000 per person/$500,000 per accident on your auto policy and $300,000 on your homeowners policy. Some demand higher thresholds—$500,000 across the board isn't unusual. If you're currently at $100,000/$300,000 auto liability, you'll need to increase those limits first.

Calculate what you actually need to protect. Grab a calculator and total up your assets. Home equity (current value minus mortgage): $__. Retirement accounts (401(k), IRA, etc.): $_. Investment and brokerage accounts: $. Savings and CDs: $. Vehicles and other valuable property: $___. That's your baseline. Now factor in your annual income multiplied by your years until retirement—that represents future earning potential. Consider risk factors: rental properties, teen drivers, pools, dogs. This exercise reveals your actual exposure.

Get quotes from at least three insurers. Start with your current auto and home insurance carrier—bundling typically saves 15-25% and simplifies claims since one company handles everything. But also request quotes from two competitors. Rates can vary by 40% or more between carriers for identical coverage. Major insurers offering competitive umbrella coverage include State Farm, Allstate, Travelers, Nationwide, Liberty Mutual, and USAA (for military-affiliated families).

Compare more than just premium costs. Policy features vary. Does the coverage extend to rental properties, and if so, how many? What's the deductible when umbrella coverage applies without underlying insurance being involved? Do legal defense costs get paid above policy limits or count against them (above is better)? How does the insurer handle situations where you have multiple umbrella policies? Read the exclusions—some carriers impose stricter limitations on watercraft, ATVs, or certain activities.

Verify underlying coverage requirements for each quote carefully. One insurer might accept $250,000/$500,000 auto liability; another demands $500,000/$500,000. These requirements directly impact your total insurance costs, not just your umbrella premium. Calculate the all-in cost: any increases to your auto/home liability limits plus the umbrella premium.

Ask about every possible discount. Beyond bundling, you might qualify for reductions based on: claims-free history (often 3-5 years), multiple vehicles, home security systems, automatic payments, paperless billing, defensive driving course completion, professional association memberships, or military service. Stack these discounts and you could reduce premiums 20-30%.

Review and adjust coverage as life changes. Your umbrella policy should grow with your wealth. Got a raise that bumped your income from $85,000 to $115,000? Consider increasing coverage. Bought a rental property? Increase coverage. Your teenager getting a driver's license? Definitely review your limits. Inherited money or sold investments that significantly grew your net worth? Adjust upward. Most carriers allow limit increases with minimal underwriting—often just a phone call or online request.

The application process requires disclosing your assets, driving history, property details (pools, trampolines, etc.), and any high-risk activities or hobbies. Insurers may request copies of your current auto and homeowners declaration pages to verify your underlying coverage. Most applications take 20-30 minutes. Approval and coverage activation typically happens within 2-5 business days.

Don't make the mistake of buying umbrella coverage, filing it away, and forgetting it exists. Set a calendar reminder to review it annually. Your financial situation five years from now will likely look very different than today. Your coverage should evolve accordingly.

Frequently Asked Questions

Most people spend more time researching which smartphone to buy than evaluating whether they need umbrella insurance. That's backward. Your phone costs $1,000. A lawsuit could cost you $2 million.

Umbrella coverage delivers exceptional protection for minimal cost—typically $150-$400 annually for $1-2 million in coverage that extends across your auto, home, and personal liability exposures. It covers situations your primary policies exclude entirely, like defamation claims. It pays legal defense costs on top of policy limits. And it protects not just your current assets but your future earnings from wage garnishment following a judgment.

The uncomfortable truth: if you own a home, have accumulated any savings, earn a decent income, or face elevated liability risks (rental properties, teen drivers, pools, certain dog breeds), you probably need umbrella coverage. The question isn't whether you can afford the premium—it's whether you can afford the consequences of going without.

Start by pulling out your current insurance policies and checking your liability limits. Calculate your net worth honestly. Consider your risk factors—what could go catastrophically wrong? Then contact your insurance agent or request online quotes from multiple carriers. Compare coverage features, not just prices. Make sure you understand underlying coverage requirements.

Then make a decision based on facts, not hope. Hope isn't a strategy for protecting decades of financial progress from a single terrible accident or lawsuit. Umbrella insurance is. For less than a dollar a day, you can safeguard everything you've worked to build.

Don't wait until after an accident to wish you'd acted. Your financial future is too important to leave exposed.