Homeowner reviewing insurance documents with house keys on a desk

Insurance Binder Meaning and When You Need One

Content

You've just had your homeowners insurance application approved, but there's a problem—your house closes in three days and the full policy won't arrive for another two weeks. Here's where an insurance binder becomes your lifeline.

A binder acts as temporary proof you're insured right now, today, this minute. It's not a promise that coverage is coming eventually. It's actual, active protection that starts the second your insurer issues it.

Here's what trips people up: they assume binders and policies are basically the same thing. They're not. That confusion has torpedoed real estate deals, left new car buyers stranded at dealerships, and created coverage gaps that cost people serious money when disaster struck during those gaps.

What Is an Insurance Binder?

Think of a binder as a 30-to-90-day insurance contract that kicks in immediately while your insurance company cranks out the full policy paperwork. It's not some watered-down "almost insurance"—it's the real deal with full legal teeth.

Your agent or broker issues this document when speed matters. Maybe your mortgage lender needs proof of coverage by Friday or the deal falls apart. Maybe you're buying a car today and can't drive it home without insurance documentation. The binder solves these timing crunches.

Within hours—sometimes within 20 minutes of approval—you'll have this document. Usually it's a single page, maybe two, delivered straight to your inbox or printed at your agent's office. Compare that to your actual policy, which might be a 40-page booklet that takes weeks to produce.

Real estate transactions devour insurance binders. No lender will hand over hundreds of thousands of dollars for a mortgage without confirmed property insurance. Your closing is scheduled for March 15th, but the policy won't be ready until March 28th? The binder covers March 15th through April 14th, keeping everyone happy.

Author: Olivia Stratfor;

Source: nayiyojna.com

Car dealerships won't let you drive off their lot without insurance proof. You've just bought a vehicle, your auto insurer needs three days to add it to your policy formally, but you need to leave today. Binder issued, problem solved, you're driving home in your new car.

Business contracts create another common scenario. You're a contractor starting a commercial job Monday morning, but the property owner demands proof of $2 million in general liability coverage before you step on site. Your insurer just increased your limits yesterday—the updated policy is being processed, but the binder confirms your coverage meets requirements right now.

How an Insurance Binder Differs from a Policy

Both documents provide legitimate coverage, but they're built for completely different purposes and situations.

| What You're Comparing | Binder | Full Policy |

| How Long It Lasts | Usually 30-90 days | Six months to one year |

| Amount of Detail | Hits the highlights only | Every term, condition, and exclusion spelled out |

| Legal Weight | Completely binding while active | Binding throughout entire term |

| Why It Exists | Proves you're covered NOW | Your complete insurance contract |

| What It Costs | No separate charge | Requires full premium payment |

| How Fast You Get It | Same day, often within hours | Days or weeks to produce |

Timing differences matter enormously. Your house closes Thursday, but your homeowners policy needs 10 business days to finalize. Without a binder, your closing gets postponed or cancelled entirely—and that delay could cost you the house if the seller won't wait.

Detail is where they really diverge. Your final policy might dedicate three pages just to explaining water damage exclusions, wind and hail deductibles, and coverage for detached structures. The binder gives you the crucial facts: coverage amounts, who's insured, effective dates, and what protections you have.

Here's a critical point people misunderstand: the binder isn't "sort of" coverage or "pending" coverage. If your house burns down while you're holding a valid binder, the insurance company pays your claim according to the binder's terms. Period. The legal obligation is identical to a full policy.

Most insurers don't charge separately for binders. You pay your annual premium for the policy itself, and the binder is included as part of their service. Some agents have administrative fees for processing generally, but those aren't binder-specific charges.

Insurance binders are essential tools in time-sensitive transactions. They provide legitimate coverage with the full backing of the insurance company, not just a promise of future coverage. I've seen countless real estate deals that would have fallen apart without the ability to issue a binder immediately

— Jennifer Martinez

When Do You Need an Insurance Binder?

Real estate closings probably account for 60% of all binders issued. Mortgage companies have zero flexibility here—no proof of insurance means no loan funding, which means no closing. Your closing date rarely syncs perfectly with how long it takes to produce a complete homeowners policy. Binders bridge that gap and keep transactions on schedule.

Buying a vehicle from a dealer creates instant binder demand. State law requires insurance before registration, and dealerships won't hand you the keys without documented proof. Your auto insurer might need 48 hours to process the addition and mail updated policy declarations. The binder proves your new Toyota is covered when you drive away Tuesday afternoon.

Business contracts frequently include insurance mandates before work starts. Property owners aren't letting contractors on site without confirmed general liability coverage, often with specific minimum limits like $1 million per occurrence. When you've just secured new coverage or increased existing limits to meet contract requirements, the binder demonstrates immediate compliance while paperwork catches up.

Financing a boat, motorcycle, RV, or other valuable asset? The bank wants assurance their collateral has protection before they approve your loan. They'll demand proof of insurance as a funding condition. If you're cutting it close on timing, that proof arrives as a binder.

Commercial lease agreements build in insurance requirements—specific liability limits, landlord listed as additional insured, coverage effective by lease commencement date. Moving into your new retail space next week but your business owners policy won't be finalized for another 10 days? You need a binder to satisfy your lease obligations and get your keys.

Some situations don't require binders at all. Renewing coverage with your current insurer usually doesn't need one since your existing policy continues seamlessly into the next term. If you've got six weeks before you need insurance proof—say, a closing scheduled way out—your insurer has plenty of time to issue the full policy without rushing.

Author: Olivia Stratfor;

Source: nayiyojna.com

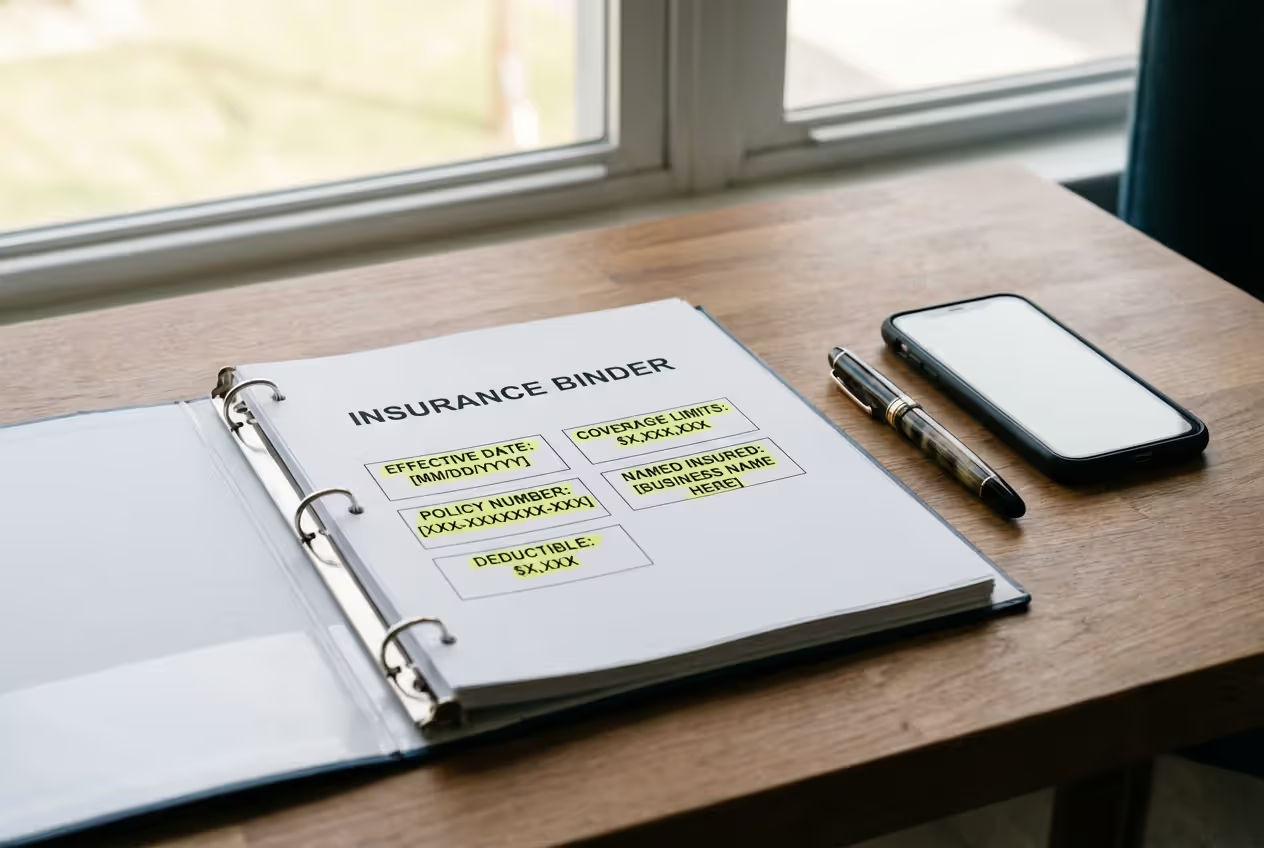

What Information Is Included in an Insurance Binder?

Coverage types form the document's backbone. Homeowners binders spell out dwelling coverage, personal property, liability, and additional protections like water backup or identity fraud coverage. Auto binders specify bodily injury liability, property damage liability, collision, comprehensive, medical payments, and uninsured motorist coverage.

Your coverage limits get prominent placement because they determine maximum protection. A typical homeowners binder might show $425,000 dwelling coverage, $318,750 for personal belongings (usually 75% of dwelling), $500,000 liability protection, and $5,000 medical payments to others. These numbers prove to lenders or landlords that your coverage hits required minimums.

Effective dates appear with precision because timing is everything. You'll see something like "Coverage begins March 22, 2026, at 12:01 AM Eastern Time and ends April 21, 2026, at 11:59 PM Eastern Time." Any claim must fall inside this specific window. A loss on April 22nd at 9:00 AM? You're not covered under this binder.

Named insureds identify exactly who's protected. For homeowners coverage, that's typically both spouses listed individually. Business binders might list the LLC, individual business owners, and third parties added per contractual requirements—like a landlord demanding additional insured status.

Premium amount tells you what the full policy will cost. You might see "$2,847 annual premium" or a breakdown showing how much goes to each coverage type. Some binders indicate your payment plan—paying in full versus monthly installments—though this varies by insurer.

Policy numbers connect your binder to the forthcoming policy. Even though your complete policy hasn't been produced yet, the insurer assigns a policy number that appears on your binder. This number tracks your coverage across systems and ensures continuity when the full policy arrives weeks later.

Company contact information includes your insurer's name, their claims phone number (often 24/7), your agent or broker's contact details, and sometimes the underwriter's information. If you have questions about coverage or need to file a claim during the binder period, this section tells you who to call.

Deductibles specify your out-of-pocket costs for covered claims. A homeowners binder might show a $2,500 deductible for most perils, but a separate 2% hurricane deductible (2% of your dwelling coverage amount). Knowing these numbers prevents nasty surprises if you file a claim while the binder is active.

How Long Does an Insurance Binder Last?

Most binders last 30 to 90 days, with 60 days being the industry sweet spot. That gives insurers enough time to complete underwriting, generate policy documents, and get them delivered without rushing.

Several factors push duration up or down. Complicated coverage situations need longer binder periods. Insuring a 1920s historic home requiring specialized appraisal? You might get a 90-day binder. Standard suburban house built in 2015? Probably 30 or 45 days because underwriting moves faster.

Your state's regulations matter too. Some states cap how long binders can remain active—preventing insurers from using them indefinitely instead of issuing proper policies. These rules protect consumers by forcing timely delivery of complete documentation.

What happens when your binder expires before your policy shows up? You're looking at a coverage gap unless you act. Most insurers will extend the binder if delays stem from their processing backlog rather than problems with your application. Call your agent at least a week before expiration to request an extension, which typically means issuing a fresh binder with a new expiration date.

Author: Olivia Stratfor;

Source: nayiyojna.com

Ideally, your full policy arrives with two weeks to spare before binder expiration. Your insurer should deliver complete policy documents—either mailed or emailed—giving you time to review everything before the binder period ends. The policy's effective date usually matches when your binder started, creating seamless transition from temporary to permanent coverage.

Sometimes circumstances require extending coverage beyond the original binder timeline. Maybe the insurance company discovered they need a roof inspection, or perhaps title issues are delaying your home closing. Your insurer can issue a second binder or extend the first one, though they'll want to understand and resolve whatever's causing the holdup.

Common Mistakes When Using Insurance Binders

Treating the binder as permanent coverage tops the list of dangerous assumptions. People receive their binder, toss it in a drawer, and completely forget about it. Two months pass, the binder expires, and they're driving around or living in their home with zero insurance without realizing it. Mark your calendar the second you receive a binder and set two reminders—one at 75% of the period and another five days before expiration.

Skipping careful review of coverage limits causes headaches when those limits fall short. Your lender requires dwelling coverage equal to your $380,000 loan amount, but your binder shows only $325,000. This mismatch could derail your closing entirely or leave you seriously underinsured. Cross-check every number on the binder against contractual requirements before assuming you're compliant.

Missing expiration dates creates coverage gaps with potentially catastrophic consequences. Your binder expires May 15th, your full policy arrives May 18th, and your house floods on May 16th. That two-day gap? You're personally liable for $80,000 in water damage because you had zero coverage when disaster struck.

Author: Olivia Stratfor;

Source: nayiyojna.com

Never following up on the full policy leaves you in dangerous limbo. Don't assume your policy will magically arrive before your binder expires. Call your agent or insurer 15 days before expiration to confirm policy production is on track. If there are delays or problems, you'll discover them while there's still time to fix issues or extend the binder.

Ignoring binder revisions creates confusion about your actual coverage. Sometimes insurers issue amended binders with adjusted limits, corrected dates, or modified terms. Each new binder supersedes the previous one completely. Always reference the most recent document with the latest date when verifying coverage details.

Misunderstanding claims procedures during the binder period causes unnecessary panic. Some people think they can't file claims with "just a binder," but that's completely wrong. Valid binder plus covered loss equals legitimate claim. File immediately using the contact information printed on the binder document. Your claim gets handled according to whatever terms are specified there.

Overlooking premium payment requirements occasionally causes binder cancellation. Most insurers collect premiums when issuing the full policy, but some require deposit premiums or down payments before they'll issue binders. Missing required payments can void your binder retroactively, meaning you never actually had the coverage you believed you had.

Frequently Asked Questions About Insurance Binders

Insurance binders solve real problems in time-sensitive situations where you need coverage immediately but full policy production takes weeks. These documents carry full legal weight and provide legitimate protection from the moment of issuance through their expiration date.

The key distinction between binders and policies comes down to duration and detail—binders last 30 to 90 days and summarize essential coverage points, while policies last months or years and include comprehensive terms and conditions. Both are legally enforceable insurance contracts during their respective periods.

Three critical actions protect you when using binders: mark expiration dates immediately upon receipt, verify coverage limits match all contractual requirements, and follow up proactively on full policy status well before the binder expires. These simple steps prevent coverage gaps that have cost people tens of thousands of dollars when disasters struck during uninsured periods.

Whether you're closing on your first home, buying a vehicle, or starting a business contract requiring proof of insurance, understanding how binders work gives you confidence to navigate insurance requirements smoothly. The binder keeps your transaction moving forward while ensuring you're protected from day one—exactly what it's designed to do