Insurance card, driver's license, car keys, and digital insurance card on smartphone

Insurance Card Guide for US Policyholders

Content

That little plastic rectangle tucked behind your driver's license? It holds the keys to your medical care and keeps you legal on the road. Lose it, misread it, or show up without it, and you might face anything from a $600 traffic fine to a $12,000 hospital bill that should've been covered. Let's break down everything printed on that card—and why each detail matters more than you'd think.

What Is an Insurance Card?

Think of your insurance card as a backstage pass to healthcare and legal driving. This document—whether it's plastic, paper, or pixels on your phone—confirms that you've paid your premiums and you're entitled to coverage under a specific policy.

When you sign up for a new policy or renew an existing one, your insurer ships out cards within about a week to ten days. Health plans typically send separate cards for each family member listed on the policy, while car insurance usually means one card per vehicle (though some carriers send extras). Each card stays valid for your policy period, which runs six months for most auto plans and twelve months for health coverage.

Here's where it gets serious: every state requires drivers to prove they carry minimum liability coverage. Show up to a traffic stop empty-handed, and you're looking at fines that start around $500 in states like California—even when you actually have insurance. You'll just need to show proof later at the courthouse, but that still means taking time off work and dealing with paperwork.

On the medical side, emergency rooms won't turn you away, but their billing departments will absolutely chase you for the full uninsured rate if they can't confirm your coverage. We're talking $8,000 for a broken arm that would've cost you a $150 copay with proper documentation.

Author: Hannah Kingsley;

Source: nayiyojna.com

How to Read an Insurance Card

Insurance companies cram more information onto these cards than seems physically possible. Each field serves a specific purpose, and mixing them up can derail your entire claim.

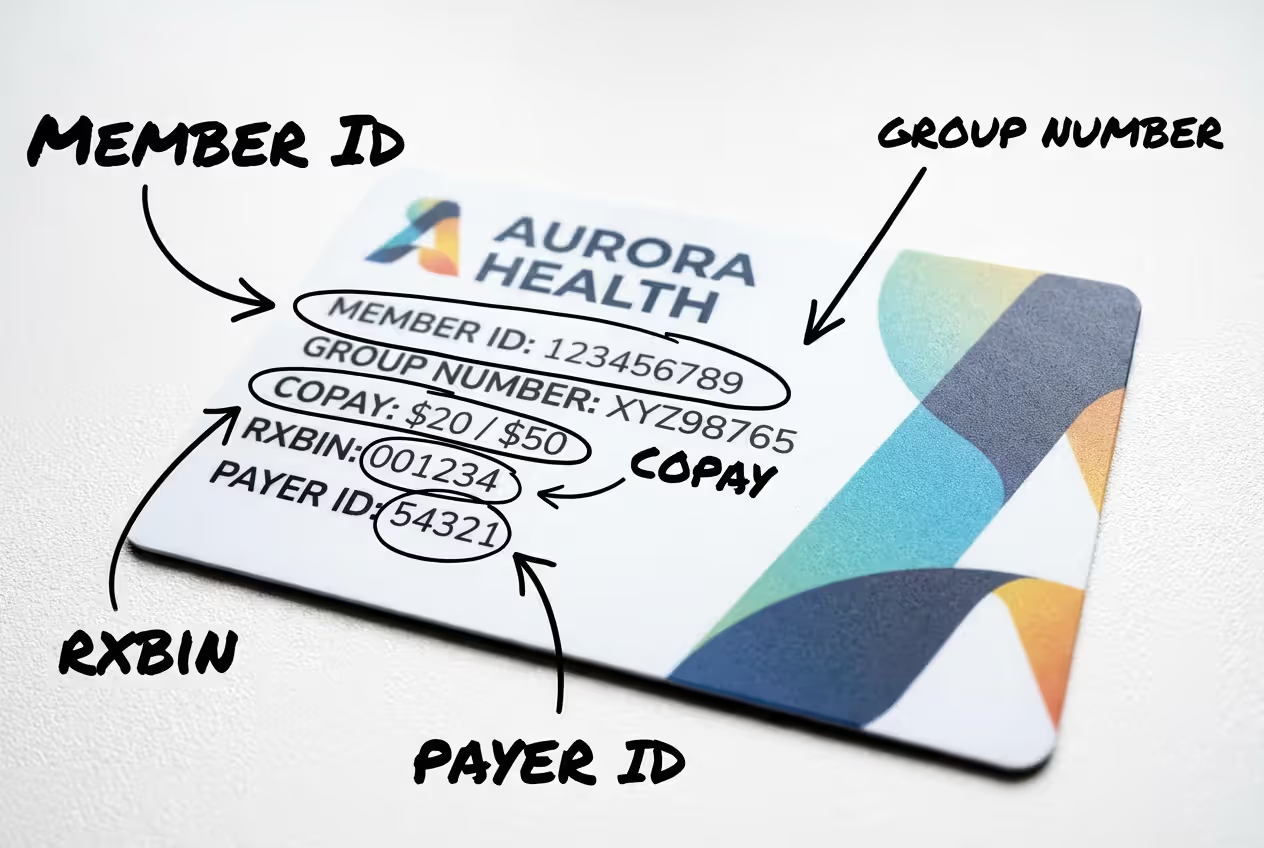

Policyholder Name: This is whoever actually owns the policy—called the subscriber on health plans. If you're covered under your spouse's employer plan, their name appears here even though you have your own card. Kids covered under a parent's policy will see mom or dad listed as the policyholder.

Member ID: Your personal identification code, usually mixing letters and numbers in strings like "ABC123456789." Medical offices and pharmacies type this into their systems to pull up your specific benefits. Transpose one character—say, a "B" instead of an "8"—and the system spits back "member not found." Then you're stuck at the front desk while they sort it out.

Group Number: This code tells providers which employer or plan sponsor is footing the bill for your coverage. Bought your plan directly through Healthcare.gov or your state's marketplace? You might not see a group number at all. That's normal for individual policies.

Policy Effective Dates: Start and end dates for your current coverage period. Bring a card that expired last month, and you'll get rejected even if you renewed—provider systems check real-time eligibility, and outdated cards throw red flags.

Copay Amounts: These are your fixed prices for specific services. Maybe $30 to see your primary doctor, $60 for a specialist, $100 for an urgent care visit. Not every plan uses copays—some charge you a percentage of the total bill instead (that's called coinsurance).

Author: Hannah Kingsley;

Source: nayiyojna.com

RxBin, RxPCN, and RxGroup: Your pharmacy trinity. The RxBin (Bank Identification Number) routes your prescription claim to the right insurance company. The PCN (Processor Control Number) aims it at the correct claims processor within that company. Forget to give the pharmacist these numbers, and your $15 prescription suddenly costs $340 at full retail price.

Payer ID: A five-digit electronic routing code that billing departments use to submit claims. You'll probably never need to know yours, but medical offices punch it in constantly.

Customer Service Number: Your lifeline when something goes wrong. Most health cards list different numbers for medical benefits versus mental health services, so check which line you're calling.

| Card Field | What It Does | Who Needs It |

| Member ID | Pulls up your benefits and claim history | Doctors, hospitals, pharmacies |

| Group Number | Connects you to your employer's plan | Medical billing offices, insurers |

| RxBin / RxPCN | Directs pharmacy claims to the right processor | Pharmacy staff |

| Payer ID | Routes electronic claims submission | Hospital billing departments |

| Copay Amounts | Shows what you pay out-of-pocket per visit | Front desk staff, patients |

Using Your Card as Proof of Insurance

Three scenarios demand that you produce this card on the spot. First up: traffic stops. Police officers in all fifty states can ticket you for failing to show proof of auto insurance, even during routine stops. Some jurisdictions impound your vehicle on the spot if you can't prove coverage.

Second: medical appointments. Walk into any doctor's office, specialist clinic, or outpatient facility, and the receptionist will ask for your card before you sit down. They'll scan or photocopy it to verify your coverage and calculate what you owe. Show up without it? Many offices make you pay the full visit cost upfront—anywhere from $150 to $400—then you file for reimbursement later. That process drags on for weeks.

Third: pharmacy counters. When you drop off a prescription, the tech enters your card information to determine your copay. Without those details, you're paying whatever the pharmacy charges uninsured customers. I've seen $25 copays balloon to $280 for the exact same medication.

Can't find your card? Call your insurer immediately and ask them to email or text temporary proof. Most companies send digital cards within minutes through their member portals or apps. For auto coverage, some states let you show your policy number and insurer contact information instead, though this takes longer for officers to verify and they might still write you a ticket.

Author: Hannah Kingsley;

Source: nayiyojna.com

Digital Insurance Cards: Acceptance and State Rules

Digital insurance cards live on your phone—either as PDFs, images in your photo library, or through your insurer's mobile app. They display identical information to physical cards but eliminate the "I left my wallet at home" panic.

Every state now accepts digital proof of auto insurance. The last holdouts updated their laws in late 2023, making electronic cards legal nationwide as of 2024. That said, your phone needs to actually work—dead batteries, cracked screens that obscure text, and extreme glare can still get you ticketed. Officers need to clearly read your policy number, coverage dates, and insurer information.

Health insurance digital cards face fewer restrictions. Nearly every medical facility and pharmacy accepts them, though I've run into a couple of small-town practices that prefer paper copies because their office systems haven't been updated since 2015. But those are outliers.

Accessing your digital card usually means downloading your insurer's app—Aetna, Blue Cross Blue Shield, UnitedHealthcare, and Cigna all offer them. Most apps let you save the card to Apple Wallet or Google Wallet for faster access. When you need to show it, unlock your phone and open the app before handing it over. Receptionists and officers need to see the full screen with all your policy details visible.

Pro tip: screenshot your card and save it to your photos, or email yourself a PDF backup. If you're somewhere with no cell service or your app glitches, you'll still have access. Also helpful if your battery is at 2% and you need to keep your phone alive long enough to get where you're going.

Common Mistakes When Using Your Insurance Card

Carrying an expired card tops the list of everyday errors. Your policy might be active and paid up, but if the card in your wallet shows last year's dates, you'll get denied. Providers verify eligibility electronically, and expired cards trigger immediate rejections. Insurers usually mail updated cards about two weeks before your renewal date, but postal delays happen. If yours hasn't shown up, log into your account and print a temporary one.

Mixing up health and auto insurance happens more than you'd expect. People hand their Blue Cross card to state troopers or give their Geico card to the medical assistant at their physical. It wastes everyone's time. Try keeping them in different sections of your wallet or labeling them with a small sticker.

Not updating your address after you move creates a paper trail nightmare. Insurers mail replacement cards, renewal notices, claim explanations, and policy updates to your address on file. Miss a renewal reminder because it went to your old apartment, and your coverage could lapse without warning. Then you're driving uninsured or showing up to appointments with no active policy.

Lending your health card to someone who's uninsured is insurance fraud, full stop. I've seen people give cards to siblings or friends who need medical care, thinking they're being generous. What actually happens: providers file claims under your name and member ID, you get stuck with bills for services you never received, and your insurer might cancel your policy and report you for fraud. On auto policies, letting an unlisted driver borrow your car can void your entire coverage if they cause an accident.

Finally, people rely too heavily on phone photos of their cards without keeping physical or proper digital backups. Your phone dies at the worst possible moment—say, after a fender bender when you need to exchange insurance information with the other driver. Always keep at least one additional copy somewhere: laminated card in your glove compartment, printed PDF in your home files, or properly saved in your digital wallet.

Author: Hannah Kingsley;

Source: nayiyojna.com

What to Do If Your Card Is Lost or Damaged

Call your insurer's customer service line right away. Most carriers email or text temporary digital cards within five to ten minutes. Physical replacement cards typically arrive in five to seven business days by standard mail, sometimes faster if you're willing to pay $15 to $25 for expedited shipping.

While you wait for the replacement, ask for a temporary proof letter. Insurers can fax this directly to your doctor's office or email you a PDF to print. For auto insurance, you can often satisfy proof requirements by giving the officer or DMV your policy number and insurer's phone number so they can verify coverage, though this takes extra time and some states still ticket you for not having the card on hand.

If your card vanished along with a stolen wallet or purse, watch your explanation of benefits statements carefully over the next few months. Thieves sometimes use stolen health insurance cards to fill fake prescriptions or receive medical services under your coverage. Spot something you didn't authorize? Contact your insurer's fraud department immediately—the number is usually on their website.

Update your insurer's mobile app as soon as the new card is issued. Sometimes policy numbers change during replacement, and having outdated information in your app can cause claim denials even when you're holding the correct physical card.

Your insurance card works like a debit card for healthcare—without it, you're basically paying cash prices.I've watched patients get hit with $10,000 emergency room bills because they couldn't show their card at admission. The hospital assumes you're uninsured and charges accordingly. Keep proof accessible, whether that's physical or digital. It's the easiest way to protect your wallet

— Jennifer Hartman

Frequently Asked Questions About Insurance Cards

Your insurance card punches above its weight. This small document opens doors to medical treatment, keeps you legal behind the wheel, and protects you from surprise five-figure bills. Knowing how to read every field, when you need to show it, and how to maintain both physical and digital backups means you won't get caught off guard.

Digital acceptance has reached a tipping point—2024 marked the year when electronic proof became standard everywhere in the United States. But the basics haven't changed: keep your proof current, carry it whenever you might need it, and understand what every code and number represents. Whether you're picking up prescriptions, getting pulled over, or checking into an emergency room, having your insurance card ready saves you from headaches, delays, and unnecessary costs.