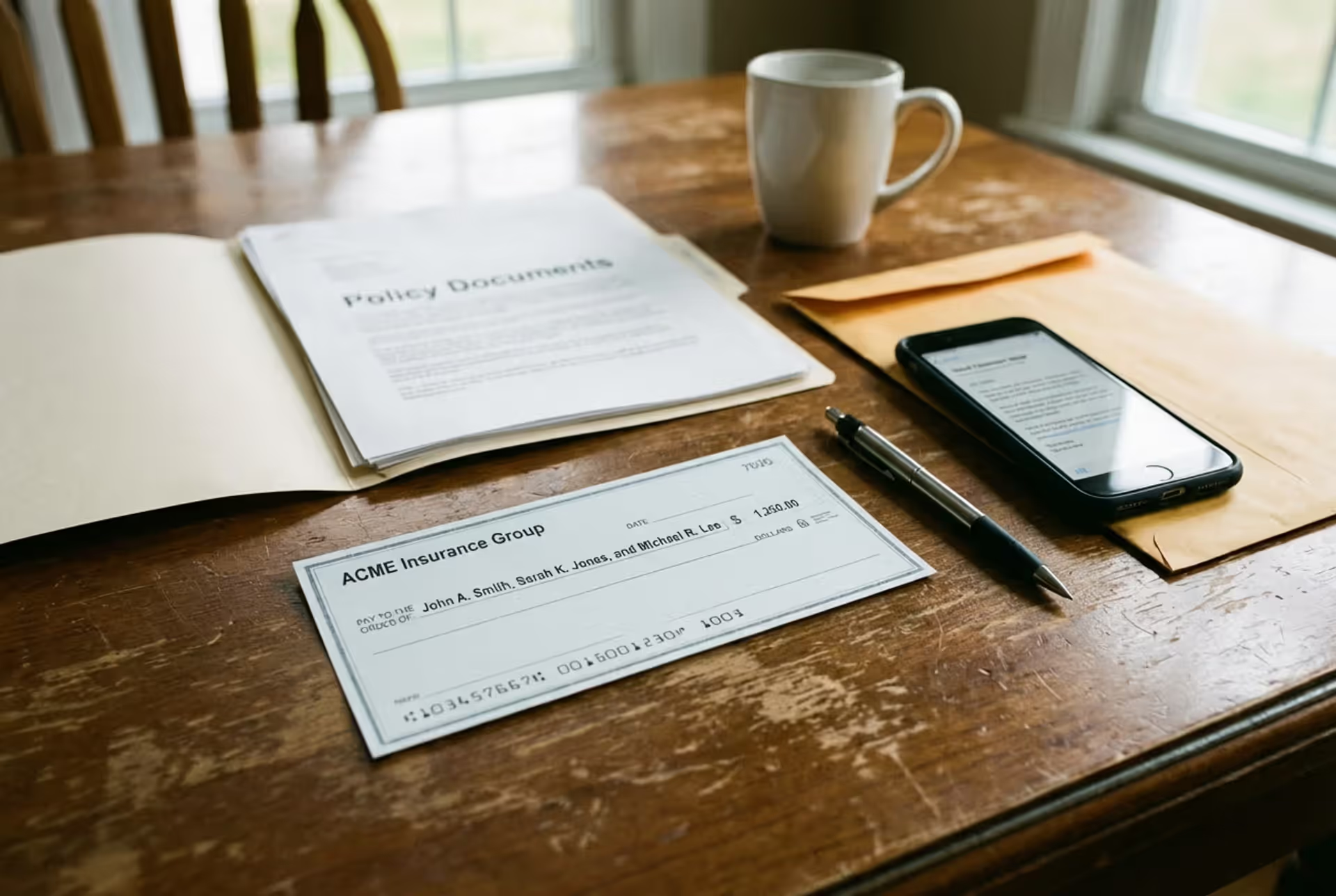

Insurance claim check with multiple payees on a desk

Insurance Claim Check Guide

Content

That check from your insurance company finally arrived—but wait. Your mortgage lender's name sits right next to yours on the payee line. Or maybe three different names appear, and you're not sure who needs to sign what. You expected a simple trip to the bank, but now you're staring at a piece of paper that might as well be written in code.

Let's decode how these checks actually work and get your money where it needs to go.

What Is an Insurance Claim Check?

Think of this as your insurance company's IOU made real. After they've said "yes, we'll cover that," they cut you a check for the damage. Sometimes it arrives as an actual paper check in your mailbox. Other times, money just appears in your bank account electronically.

The dollar amount you see represents what the insurer calculated for repairs, minus whatever deductible you agreed to pay. If you carry an actual cash value policy, they've also subtracted depreciation—that wear-and-tear discount that acknowledges your three-year-old roof wasn't worth what a brand-new one costs.

Property damage triggers most of these checks. Your car gets sideswiped in a parking lot. A summer hailstorm punches holes in your siding. Your water heater floods the basement at 2 AM. After the adjuster inspects everything and runs the numbers, a check shows up.

Homeowners claims make up a huge chunk of these payments. Storm damage, fire, burst pipes, fallen trees—anything covered under your policy that requires cash to fix. Auto claims work similarly, whether someone rear-ended you at a stoplight or a shopping cart dinged your door.

Here's where it gets interesting with replacement cost coverage: you might receive two checks. The first covers depreciated value right away. After you finish repairs and send proof, they mail a second check for that depreciation amount they held back. It's their way of making sure you actually fix things rather than pocketing the cash.

Medical insurance rarely sends you checks directly. Doctors and hospitals usually bill your insurer straight away. But visit an out-of-network provider or pay upfront for something? Then you might see reimbursement checks with your name on them.

How Insurance Claim Checks Work

Your adjuster closes their file and clicks "approve." Now what?

The claims department queues up your payment. Simple claims—think straightforward fender-benders with clear liability—generate checks within a week, sometimes sooner. Complicated situations where multiple coverages overlap, or where you and the adjuster disagree about repair costs, can drag on for months.

Most insurers still mail physical checks, believe it or not. You'd think everything would be electronic by now, but that paper check in an envelope remains standard. Processing and mail time means 7-14 days between approval and your mailbox.

Direct deposit speeds things up dramatically when available. Two or three days after approval, the money hits your account. A few companies experiment with payment cards or apps, though these haven't caught on widely for major settlements.

Here's an important distinction: first-party versus third-party checks. First-party means your own insurance company paying your claim. You file with State Farm because wind damaged your fence, and State Farm pays you. Third-party means someone else's insurance pays you directly—like when your neighbor's tree crushes your shed and their Allstate policy cuts you a check instead of you filing through your own carrier.

Author: Olivia Stratfor;

Source: nayiyojna.com

The payee line tells the whole story. Just your name? Easy. Your name plus your bank's name plus a contractor's name? Buckle up.

For big claims—say $40,000 in fire damage—many insurers break payments into chunks. Initial check covers emergency repairs and temporary housing. Submit contractor bids, and they release more. Finish the work with receipts, and the final payment arrives. This staged approach protects everyone. You get money as needed, they ensure it's spent appropriately, and nobody feels cheated.

Who Gets the Insurance Claim Check?

Your name appears on the check, obviously. But who else might be listed alongside you?

Own your home free and clear, with no mortgage? The check names only you. Paid off your car completely? Same deal—just your name on that collision payment.

Still making mortgage payments? Your lender's name appears right next to yours. They hold a lien on your house, and your mortgage contract specifically requires you to maintain insurance. Banks want certainty that you'll repair damage rather than letting their collateral deteriorate while still owing them $200,000.

Car loans work identically. Your bank or credit union owns that vehicle until you make the final payment. Any comprehensive or collision check will list both you and the lienholder. They're protecting their asset.

Other joint payee scenarios pop up regularly. Married co-owners both appear on homeowners checks. Business partners who co-own property both get named. Hired a roofer before the claim check arrived? Insurers sometimes list both you and the contractor to guarantee the worker gets paid.

Business claims add complexity. A check might name the LLC, any additional insureds listed on the policy, and potentially the property owner if you lease your space. Commercial vehicle claims follow personal auto patterns—whoever's on the title plus any lienholders.

Liability claims flip the script entirely. You cause damage to someone else's property, and your liability coverage pays them directly. That check goes to the injured party, not to you. You never see or touch that money.

How to Cash or Deposit Your Insurance Claim Check

Walking into your bank with that check requires preparation. What you need depends entirely on how many names appear up top.

Single-Payee Checks

Only your name on the front? Smooth sailing ahead. Flip it over, sign your name exactly as printed on the front, and head to your bank.

Bring your driver's license, passport, or state ID. Banks won't process the check without confirming you're actually the person named.

Deposit options include the usual suspects: bank teller, ATM, or your phone's mobile app. That last option hits a snag with large amounts, though. Most banks cap mobile deposits somewhere between $5,000 and $10,000 daily. Your $30,000 roof claim? You'll need to visit a branch or split deposits across multiple days if your bank allows that workaround.

Big checks trigger holds even when properly endorsed. Banks get nervous when you suddenly deposit $25,000 and your typical deposits run $2,000. They might freeze those funds for a week while verifying the check's legitimacy. Call ahead if you need immediate access to a substantial settlement.

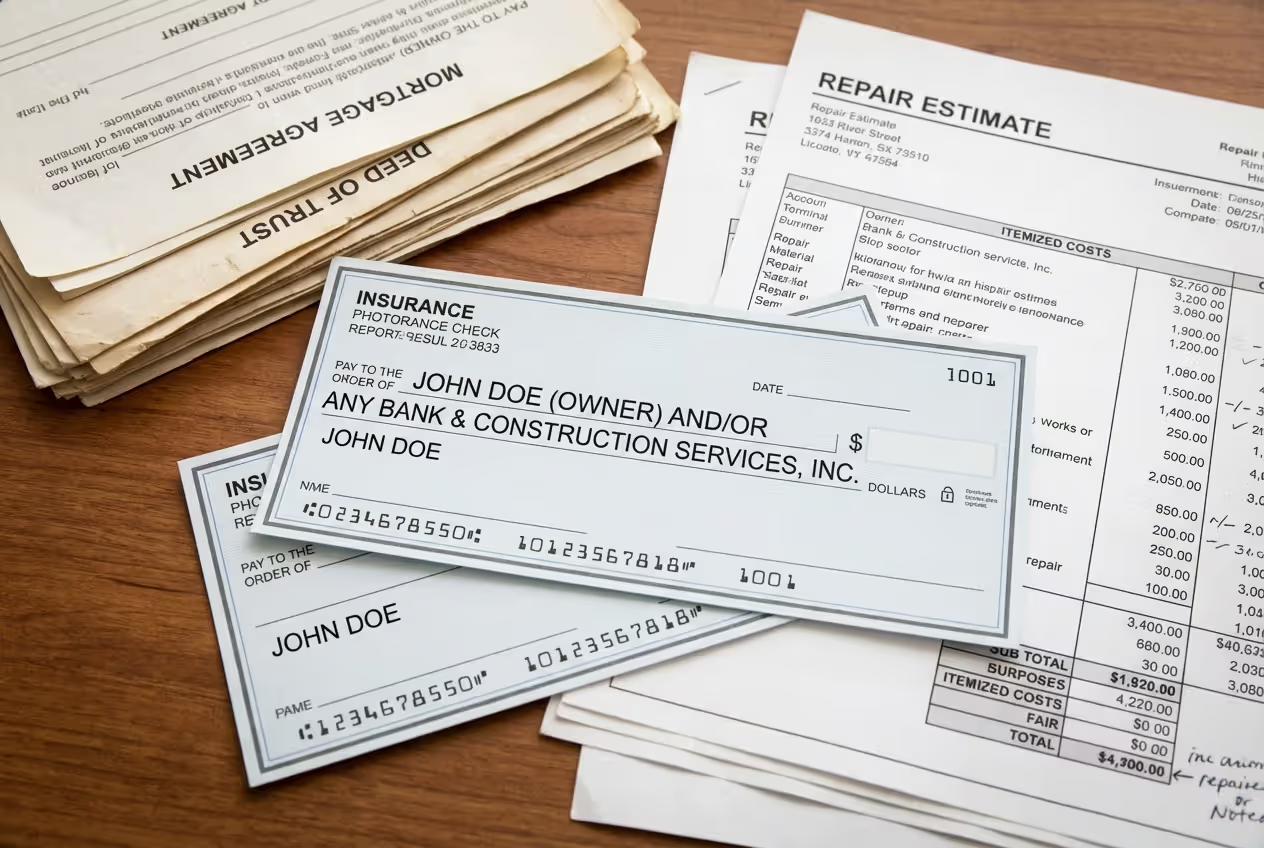

Multi-Payee Checks

Multiple names mean multiple signatures—every single person listed must endorse.

The word between names matters legally. "And" requires everyone's signature. "Or" theoretically lets any single named party deposit it, though bank policies vary and most play it safe by requiring all signatures anyway.

Insurance checks almost always use "and." That check reading "Michael Torres and Premier Bank and ABC Contractors" needs three signatures before anyone touches that money.

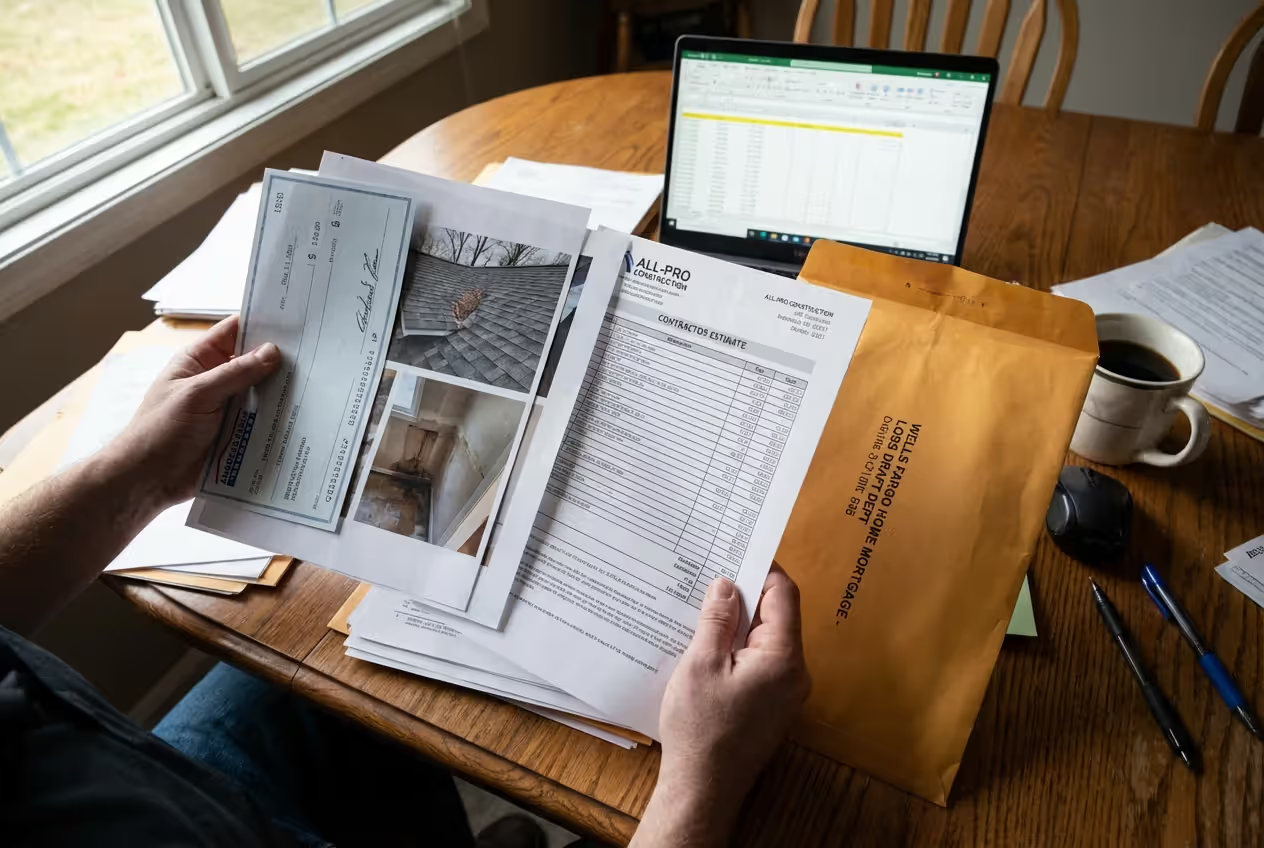

Mortgagee-included checks follow a specific dance:

- Sign your name first on the back

- Package it with damage photos and contractor estimates

- Mail everything to your mortgage company's insurance claims department

- Wait while they review

- They either send it back endorsed, put money in escrow, or pay contractors directly as work progresses

Smaller amounts—typically under $10,000 to $25,000, depending on the lender—often get endorsed and returned immediately. Larger sums usually land in an escrow account the lender controls. They release money in stages as you prove work completion.

This escrow process infuriates homeowners who want their money now. Mortgage companies counter that they're protecting a $300,000 asset from remaining unrepaired. Both sides have valid points. The lender wins because they wrote that requirement into your mortgage contract.

Author: Olivia Stratfor;

Source: nayiyojna.com

Insurance Claim Check Endorsement Rules

Your signature on the back isn't just formality—it's a legal certification that you're entitled to those funds.

Every named payee must sign. Banks face serious liability for cashing improperly endorsed checks, so they enforce this rule strictly. Try depositing a multi-payee check with only your signature, and it bounces right back.

Sign using the exact name printed on the front. Check says "Elizabeth Anne Morrison" but you always sign "Liz Morrison"? Your bank might balk at the discrepancy. Match what's printed, even if it feels awkward.

Lienholder endorsement procedures vary by institution, but most auto lenders want:

- Their endorsement form completed

- Photos showing the damage

- Repair estimates from licensed shops

- Current insurance declaration page

They review everything, confirm the claim amount matches actual damage, then either endorse the check back or pay your repair shop directly. Figure 5-10 business days for most lenders, sometimes longer during busy periods.

Mortgage companies often require more. Large claims might trigger an inspection—they send someone to photograph damage and verify your claim amount aligns with reality. For staged payments, they want proof of progress before releasing additional funds from escrow.

What if someone refuses to sign? You're stuck.

Maybe a contractor got angry over a dispute and won't endorse that joint check. Perhaps a divorcing spouse uses their signature as leverage. Sometimes lienholders just sit on checks for weeks without explanation.

Your options aren't great:

- Negotiate to resolve whatever's blocking the signature

- Ask your insurer to reissue the check with different payees

- Pursue legal action forcing endorsement (expensive and slow)

- File a complaint with your state insurance department if payees were improperly named

Some states mandate timeframes for mortgage companies to endorse checks or release escrow funds. Research your state's requirements if a lender creates unreasonable delays.

Insurance Claim Check Endorsement Rules

Sign the check exactly how your name appears on the front—character by character. Banks verify this match carefully because your signature legally certifies your entitlement to the funds.

Banks carry significant liability for processing checks with missing or forged endorsements. They've learned through expensive lawsuits to reject anything questionable. One missing signature from a three-party check? The bank sends it back, no exceptions.

Author: Olivia Stratfor;

Source: nayiyojna.com

Auto lenders typically require a packet of information before they'll add their endorsement:

- Completed endorsement request form from their website

- Photos clearly showing your vehicle's damage

- Written estimates from licensed repair facilities

- Copy of your current insurance declarations page proving active coverage

They verify that claim dollars match the actual damage—protecting against fraud where someone might exaggerate damage to pocket extra money. Most process these requests within a week. During heavy claim periods after major hailstorms or hurricanes, wait times stretch longer.

Mortgage companies often demand more documentation, especially for large claims exceeding $20,000 or $30,000. They may dispatch an inspector to photograph damage and confirm repairs match the claim amount. This protects their collateral—your home—and ensures money gets spent appropriately.

For staged payments through escrow, lenders release funds as you demonstrate progress. Submit photos of completed framing, and they release money for the next phase. Show receipts for completed roofing, and electrical funds become available. This milestone-based approach frustrates homeowners wanting all money upfront but gives lenders confidence their collateral is actually being restored.

Refused endorsements create nightmares. A contractor withholding their signature over a payment dispute. An ex-spouse using endorsement as leverage during divorce proceedings. A lienholder that simply ignores your requests for weeks.

You have limited remedies:

- Negotiate directly with the refusing party to address their concerns

- Request your insurer reissue the check excluding the problematic payee

- File legal action compelling endorsement (costly and time-consuming, often exceeding the claim amount)

- Report the issue to your state's insurance regulatory department if you believe payees were incorrectly named

Several states enacted laws requiring mortgage companies to endorse within specific timeframes—often 10-15 business days—or face penalties. Check your state's insurance regulations if a lender stalls unreasonably.

Common Problems With Insurance Claim Checks

Expert Insight:

The biggest mistake I see homeowners make is cashing multi-payee checks without understanding the endorsement requirements.They deposit a check that includes their mortgage company's name, their bank rejects it, and suddenly they're facing delays while the insurer reissues the payment. Always read the payee line carefully and contact all named parties before attempting to deposit a claim check

— Robert Chen

Misspelled names rank among the most common frustrations. Your insurer lists "Johnathan" instead of "Jonathan," or includes a lienholder you refinanced away from two years ago. These errors make the check undepositable. Contact your adjuster immediately requesting corrected reissue. Add another 10-14 days to your timeline.

Lost or stolen checks demand quick action. Call your insurance company's claims department the moment you realize the check is missing. They'll place a stop payment on the original and queue a replacement. Some insurers charge $25-$50 for this service. Replacement typically takes two weeks.

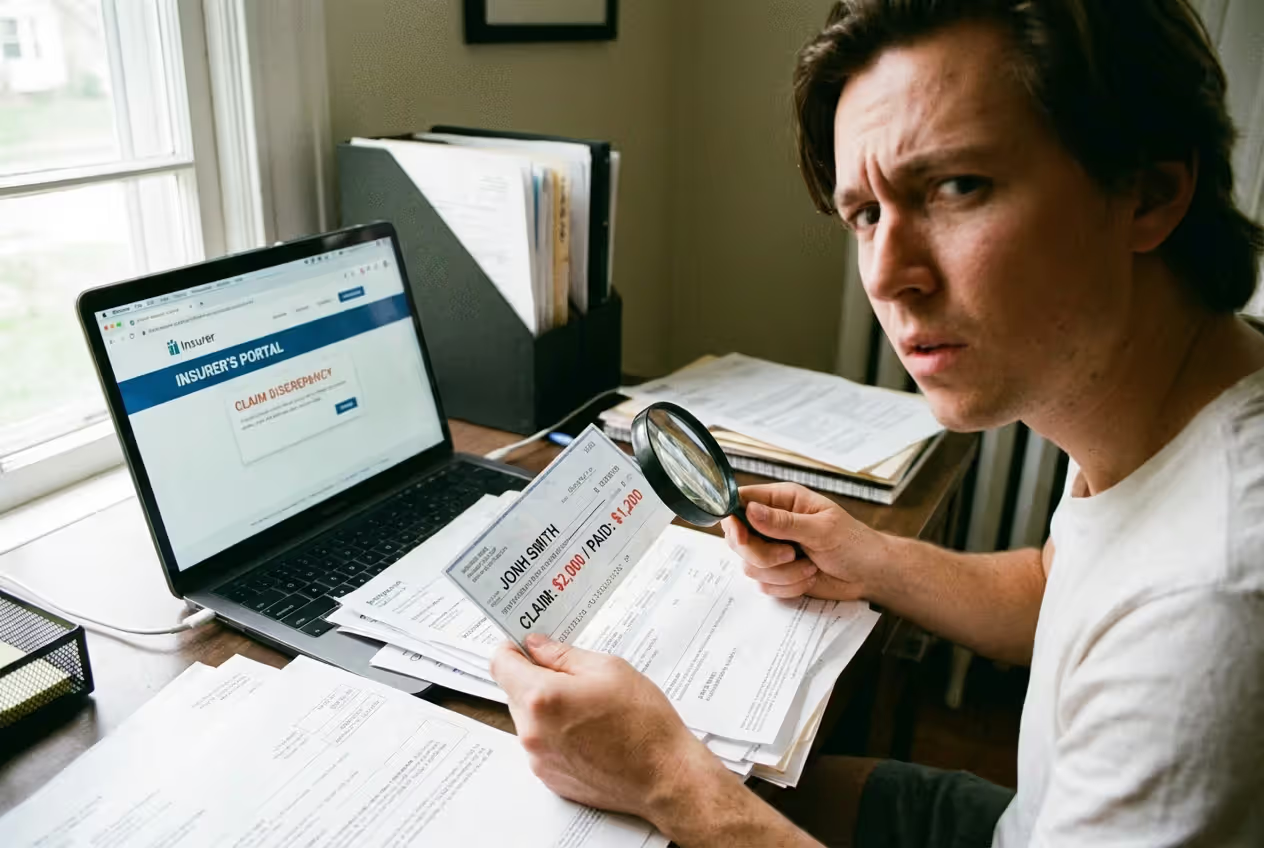

Amount disputes create bigger headaches. You collected $18,000 in contractor estimates, but the insurer's check shows $9,500. Before depositing, understand whether cashing constitutes acceptance of full settlement. Many checks include fine print stating that depositing waives your right to dispute the amount.

Author: Olivia Stratfor;

Source: nayiyojna.com

If the settlement seems low:

- Obtain independent estimates from three licensed contractors

- Review your policy's dispute resolution and appraisal clauses

- Consider hiring a public adjuster who works on your behalf (they take 10-15% of settlements but often increase payouts substantially)

- Request re-inspection or invoke your policy's appraisal provision if available

Contractor payment problems emerge when homeowners deposit checks listing the contractor's name without paying the worker. Contractors can file mechanics liens against your property, sue for payment, and create complications when you try selling or refinancing. Always pay contractors properly for completed work.

Some contractors pressure homeowners to sign over checks before starting work. Red flag. If they vanish with your money or perform shoddy work, you've lost all leverage. Pay in stages tied to completion milestones, not upfront lump sums. Most state contractor licensing boards recommend this approach.

| Check Type | Who Signs | Deposit Location | Typical Situations | Timeline |

| Single-Payee | You alone | Any bank, ATM, mobile app | Paid-off car damage, renters claims, minor home repairs | Same day to 2 days |

| Joint with Mortgage Company | You and lender | Send to lender first, then your bank after their endorsement | Home damage when you have a mortgage | 10-30 days including lender review |

| Joint with Auto Lienholder | You and financing company | Send to lender first, then bank or directly to repair shop | Car damage while you're making payments | 5-15 days including lender review |

| Joint with Contractor | You and the worker | Your bank after both sign, or directly to contractor | Major repairs with contractor named | 1-3 days after all signatures |

| Third-Party Payment | Injured party only | Their bank | Your liability coverage paying someone you damaged | Same day to 2 days |

FAQ

Those insurance claim checks represent more than just money—they're legal financial instruments requiring careful handling and proper procedures. The payee line determines everything: who signs, where you deposit, how long processing takes.

Multiple parties on your check mean coordinating signatures and following specific endorsement procedures. Lenders control large claim payments through escrow accounts and staged releases. Rushing the process or ignoring requirements creates delays, rejected deposits, and frustrated phone calls.

When your check arrives, read the payee line carefully before doing anything else. Gather required documentation like damage photos and contractor estimates. Contact all named parties to understand their endorsement procedures and timelines. This preparation minimizes delays and gets your money accessible faster.

Complex situations—disputed amounts, contractor disagreements, uncooperative payees—benefit from professional guidance. Licensed public adjusters negotiate with insurers on your behalf. Attorneys handle cases where parties refuse endorsement or disputes over payee designation arise. Your state insurance department can intervene when companies violate regulations.

Document everything throughout the process. Photograph damage before and during repairs. Save all contractor estimates and receipts. Keep copies of correspondence with your insurer and lender. This documentation protects you if disputes arise and speeds up processing when you need to prove work completion.

Treat your claim check seriously from the moment it arrives until the final deposit clears. Understanding the rules, following proper procedures, and communicating with all parties prevents the common pitfalls that turn a simple insurance payment into a months-long ordeal.