Car buyer reviewing loan terms with a dealer at a desk in a showroom

What Is a Finance Charge on a Loan

Content

You've found the perfect car. The dealer quotes you a 6% interest rate on a $20,000 loan. Quick math tells you that's $1,200 in interest per year, right? Not quite. Three months into payments, you realize you're actually paying back $24,300—that's $4,300 more than you borrowed, not the $3,600 you calculated. Where did the extra $700 come from?

Finance charges explain that mystery. They're the real price tag on borrowed money, encompassing everything you'll pay beyond the principal. Most people zoom in on interest rates during loan shopping, then get blindsided by origination fees, insurance premiums, and administrative costs that weren't part of their mental math. Getting a handle on total borrowing costs means understanding every dollar you'll hand over to your lender.

Finance Charge Meaning and Definition

Finance charges show you the complete dollar cost of a loan. Back in 1968, Congress passed the Truth in Lending Act after consumers kept getting trapped by deceptive lending practices. Lenders would tout low rates while hiding costs in fine print. The law—which has been amended multiple times, most recently heading into 2026—forces lenders to display this all-in number before you commit to anything.

Here's what the law actually says: finance charges include everything a creditor requires you to pay, directly or indirectly, to get credit. It's comprehensive by design.

Picture borrowing $15,000 for home improvements. You make payments for five years and end up handing over $18,500 total. Your finance charge? That $3,500 gap between what you got and what you paid.

Why does this matter legally? Because banks used to play games. They'd advertise "6% loans!" while tacking on processing fees, mandatory insurance policies, and administrative charges that pushed your real cost to 9% or 10%. You wouldn't discover this until you'd already signed papers. The Truth in Lending Act shut down these tactics by demanding upfront disclosure of both the finance charge (in dollars) and the APR (as a percentage).

Principal sits in its own category, separate from finance charges. When you take out that $20,000 auto loan, the $20,000 you drive away with is principal. It's the money you actually get to use. Everything else you repay? That's your finance charge.

Author: Olivia Stratfor;

Source: nayiyojna.com

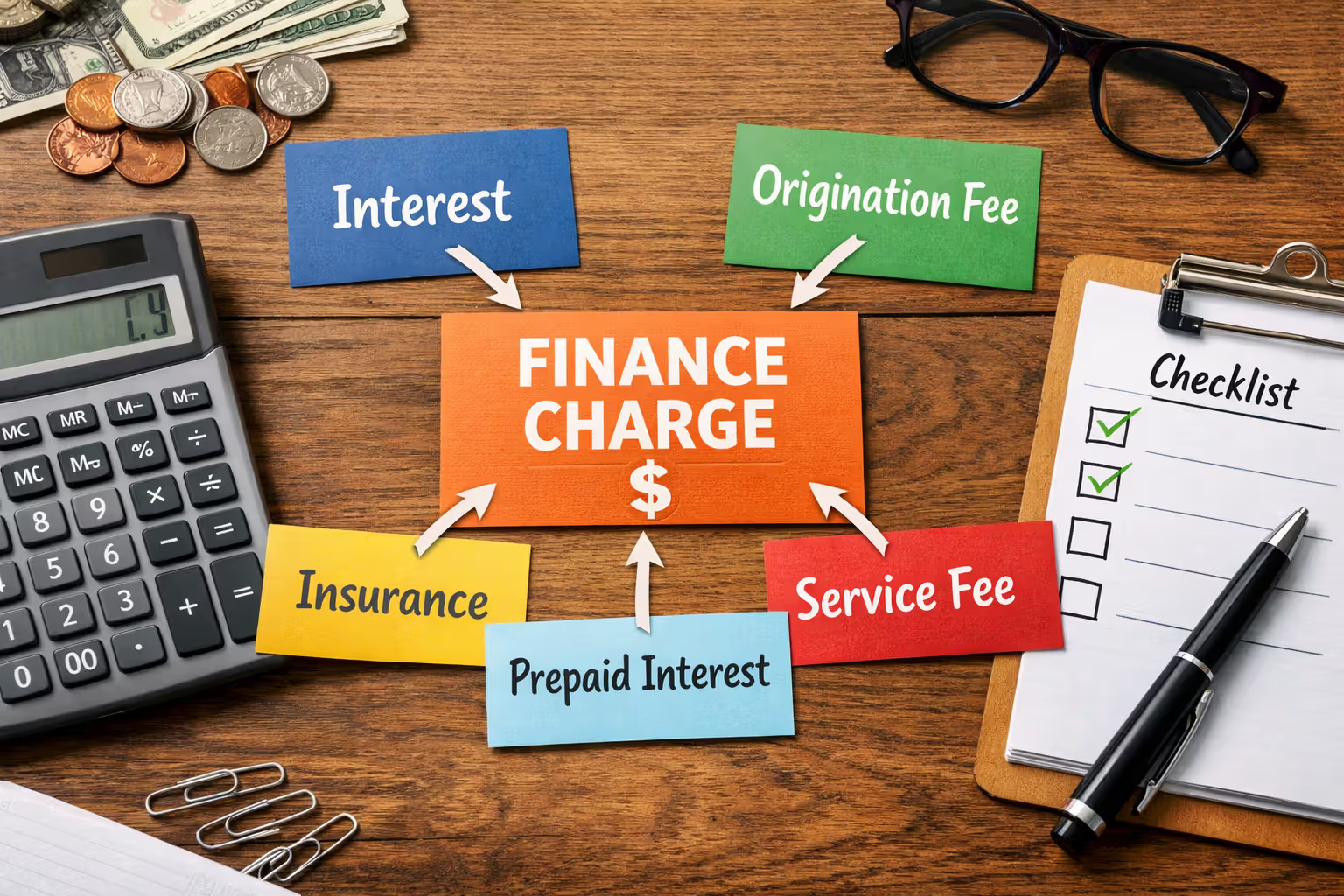

What Is Included in a Finance Charge

Finance charges pull together multiple cost types. Not every loan includes every item, but here's what could show up:

Interest makes up the biggest chunk for most borrowers. It's the percentage-based fee on whatever you still owe. Take a $10,000 personal loan at 7% annually. If you made zero payments for twelve months, you'd rack up $700 in interest. Make payments, and your balance drops—along with future interest calculations.

Origination fees pay lenders for the work of processing your application and setting up the loan. Mortgage lenders usually charge 0.5% to 1% of whatever you're borrowing. That means a $300,000 home loan could hit you with $3,000 right off the bat. Personal loan companies often take 1% to 8%, with the exact amount tied to your credit history.

Discount points show up mainly on mortgages. One point costs 1% of the loan and typically drops your interest rate by around 0.25%. Pay $4,000 in points on a $200,000 mortgage, and you might knock your rate from 6.5% down to 5.75%. You're paying more upfront (increasing immediate finance charges) to save on interest later.

Service charges and transaction fees cover the lender's administrative overhead. Credit card companies love annual fees. Other lenders charge for document prep or underwriting analysis.

Required insurance premiums count toward finance charges when your lender won't approve the loan without them. Private mortgage insurance (PMI) applies to conventional home loans when you put down less than 20%. Credit life insurance—which pays off your debt if you die—increases finance charges whenever lenders make it mandatory.

Late payment fees add to your ultimate finance charge if you trigger them. That $35 late fee on your personal loan won't appear in the initial disclosure, but it absolutely increases what you pay overall.

Prepaid interest appears when your closing date and first payment date create a gap longer than 30 days. Lenders charge interest for those extra days, adding it to your total finance charge.

Some loan-related expenses don't count as finance charges even though you pay them. Title insurance, property appraisals, credit report pulls, and notary services stay separate because third parties provide these services—they're not compensation going to your lender. Application fees sometimes dodge finance charge categorization if the lender charges them whether you complete the loan or walk away.

Author: Olivia Stratfor;

Source: nayiyojna.com

Finance Charge vs Interest: Key Differences

Most people treat these terms as synonyms. They're not, and mixing them up costs money.

Interest specifically means the percentage-based cost calculated from your balance, rate, and loan duration. Borrow $5,000 at 9% for three years with standard monthly payments, and you'll generate about $725 in interest charges.

The finance charge takes that $725 and adds everything else. Same loan with a $200 origination fee and $50 processing charge? Your finance charge jumps to $975.

Here's how this plays out in real decisions. You're shopping for a $25,000 auto loan:

First Bank advertises 5.5% interest with zero fees. Over five years, you'll pay roughly $3,700 in interest. That's your total finance charge—$3,700.

Second Bank counters with 5.0% interest but wants a $500 origination fee plus a $400 credit insurance premium. Despite the lower interest rate, your total finance charge climbs near $3,800 because those fees eat up your interest savings.

Why does confusion persist? Marketing. Lenders highlight interest rates in advertisements because 5.0% looks better than "$3,800 in total costs." Credit card companies promote "0% interest for 12 months" while charging a 3% balance transfer fee—which is absolutely a finance charge, even with zero interest accruing.

This distinction prevents expensive mistakes. A mortgage at 6.25% with $5,000 in upfront fees might cost less over two years than a 6.5% mortgage with $1,000 in fees, depending on when you refinance or sell.

How Finance Charges Are Calculated

Calculation approaches vary, but patterns emerge once you know what to look for.

Simple interest drives most installment loans—mortgages, auto financing, personal loans. The math multiplies your remaining balance by the interest rate and time period. Owe $8,000 at 6% annually? You're accumulating $480 in interest per year, which breaks down to $40 monthly. As you chip away at the principal, future interest drops because there's less balance to calculate against.

Compound interest adds accumulated interest back into your principal, then calculates new interest on that larger total. Credit cards typically compound daily. Carry a $3,000 balance at 18% APR, and the card issuer calculates interest on $3,000 plus the previous day's interest charge. This creates a snowball effect that makes credit card debt particularly expensive.

Lenders fold non-interest fees into your total finance charge. They take origination fees, points, mandatory insurance, and other costs, then add them to the interest total.

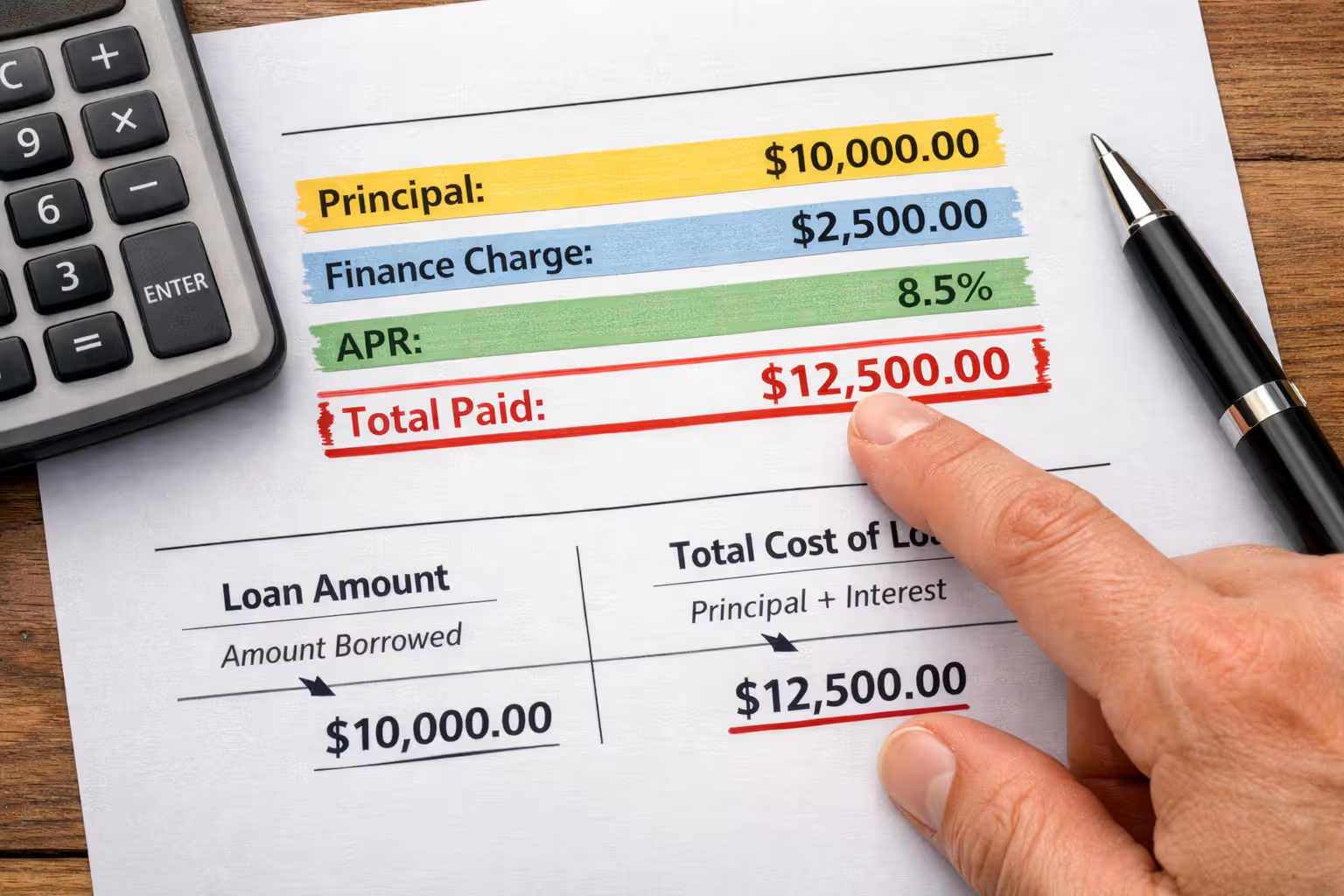

Finance Charge Calculation Example

You're buying a used car with a $12,000 loan:

- Annual interest rate: 7%

- Repayment period: 48 months

- Origination fee: $300

- Documentation fee: $75

Your monthly bill comes to $287.48. Multiply that by 48 payments and you get $13,798.40 total paid out. Subtract the $12,000 you originally borrowed: $1,798.40 in interest charges. Now tack on that $300 origination fee and $75 documentation fee. Your complete finance charge hits $2,173.40.

If you'd only looked at interest, you'd think the loan costs $1,798.40. Those seemingly small fees add $375—that's 21% more than you expected.

Author: Olivia Stratfor;

Source: nayiyojna.com

Understanding APR in Finance Charges

Annual Percentage Rate (APR) standardizes comparisons by converting total costs into a yearly percentage. Unlike the interest rate (which only covers interest), APR wraps in fees and other expenses.

That $12,000 auto loan above carries a 7% interest rate but roughly an 8.2% APR once fees factor in. Bigger fees relative to loan size create wider gaps between interest rate and APR.

Federal regulations require lenders to show APR next to the interest rate specifically so you can compare actual costs. A mortgage advertised at 6% with 2 points and $3,000 in assorted fees might carry a 6.4% APR, while a 6.25% loan with minimal fees shows a 6.3% APR—making the second choice cheaper despite its higher stated interest rate.

One caveat: APR calculations assume you'll keep the loan for its entire term. Refinance a mortgage after three years, and those upfront fees get spread across fewer years, pushing your effective APR higher than originally disclosed.

Why Finance Charges Differ by Loan Type

Loan design, collateral requirements, and payment structures create massive variations in finance charges.

Mortgages pile up the highest absolute finance charges thanks to enormous principal amounts and extended terms. A $350,000 mortgage at 6.5% stretched over 30 years generates approximately $450,000 just in interest. Layer on $7,000 in origination fees, $4,000 in discount points, and potentially decades of PMI payments, and total finance charges can blast past $500,000—exceeding what you originally borrowed.

Auto loans land in the middle. A $30,000 car financed at 6% over 60 months costs about $4,800 in interest. Dealer-arranged financing tends to carry higher fees than direct bank loans, adding $500 to $1,000 through documentation charges and rate markups that dealers pocket.

Personal loans show enormous variation. Borrowers with excellent credit scores access rates near 6% to 8% with modest fees, keeping finance charges manageable. Subprime borrowers face 18% to 36% rates plus origination fees reaching 8% of the loan amount. A $5,000 personal loan at 28% with a 5% origination fee generates nearly $3,500 in finance charges over three years.

Credit cards impose the steepest percentage-based finance charges. Average APRs cluster around 20% to 24% in 2026, with penalty rates hitting 29.99%. Carry a $4,000 balance for two years at 22% APR while making only minimum payments, and you'll rack up approximately $2,000 in interest. Annual fees ($95 to $550 for premium cards) and late charges ($30 to $40 per incident) pile on additional finance charges.

What drives these differences?

Loan term length directly controls interest accumulation time. Shorter terms provide less runway for interest to build, cutting finance charges even though monthly payments increase. A 15-year mortgage at 6% costs roughly half the interest of a 30-year loan at the identical rate.

Creditworthiness determines risk-adjusted pricing. Lenders charge substantially higher rates and fees to borrowers with sub-670 credit scores, compensating for elevated default risk. The gap between a 5% rate for excellent credit and a 12% rate for fair credit adds thousands in finance charges on identical loan amounts.

Secured versus unsecured debt creates significant rate disparities. Mortgages and auto loans use property as collateral, enabling lenders to offer lower rates because they can repossess assets if you default. Personal loans and credit cards lack collateral, forcing lenders to charge higher rates to absorb losses from borrowers who can't repay.

Lender business models influence cost structures differently. Credit unions frequently charge lower fees and rates than commercial banks because of their nonprofit status and member-ownership model. Online lenders might waive origination fees but compensate with higher interest rates. Payday lenders impose astronomical finance charges—a $500 two-week payday loan with $75 in fees translates to 391% APR.

How to Reduce Finance Charges on Your Loan

Smart moves before and during your loan can save thousands.

Author: Olivia Stratfor;

Source: nayiyojna.com

Improve your credit score before applying. Lenders reserve their best rates for borrowers with scores above 740. Paying down credit card balances, disputing credit report errors, and avoiding new credit applications for six months before your loan application can boost your score 30 to 50 points—enough to trim your rate by 0.5% to 1% and substantially reduce finance charges.

Make larger down payments. Borrowing less directly cuts interest charges. A 20% down payment on a home eliminates PMI requirements, saving $100 to $300 every month. On auto loans, putting down 20% instead of 10% reduces both your principal and the interest calculated on it.

Choose shorter loan terms. A 48-month auto loan at 6% generates lower total finance charges than a 72-month loan at 5.5%, even though the extended loan advertises a lower rate. The shorter term reduces interest accumulation time. Monthly payments climb, but your total cost drops.

Compare multiple lenders. Rate and fee differences between lenders can span 1% to 2% on identical loans. Pull quotes from at least three sources—a traditional bank, a credit union, and an online lender—to find the best rate-and-fee combination. Don't fixate solely on interest rates; calculate complete finance charges including every fee.

Negotiate fees. Origination fees, processing charges, and documentation fees are often negotiable, particularly when you're armed with competing offers. Lenders frequently waive or reduce fees to secure your business. Mortgage brokers sometimes absorb certain costs to close deals.

Pay ahead of schedule. Extra principal payments shrink your balance faster, cutting future interest charges. Adding $100 to your monthly mortgage payment can eliminate years from your loan term and tens of thousands in finance charges. Verify your lender doesn't charge prepayment penalties before implementing this strategy.

Refinance when rates drop. If interest rates fall 1% or more below your current rate, refinancing can reduce your APR and total finance charges. Calculate whether new loan fees are offset by interest savings over your expected holding period.

Avoid unnecessary add-ons. Lenders generate profit from credit insurance, extended warranties, and GAP coverage by embedding costs in your finance charge. Buy these products separately if you genuinely need them—third-party providers usually offer better prices—or skip them entirely when your situation doesn't warrant them.

Finance Charge Comparison by Loan Type

| Loan Type | Interest Rate Range (Typical) | Fees Usually Included | Approximate Total Finance Charge on $10,000 |

| Mortgage (30-year fixed) | 6.0%–7.5% | Origination costs, discount points, PMI, prepaid interest | $11,500–$14,000 (for $10K portion only) |

| Auto Loan (60 months) | 5.0%–8.0% | Origination charges, documentation costs | $1,300–$2,200 |

| Personal Loan (36 months) | 7.0%–18.0% | Origination costs (1%–8% range), processing charges | $1,100–$3,500 |

| Credit Card (revolving credit) | 18.0%–24.0% | Annual membership fee, late charges, over-limit charges | $2,000–$4,000 (assuming 24-month payoff) |

These figures represent 2026 market conditions for borrowers with good credit (670–739 score range). Your actual costs depend on credit profile, specific lender, and geographic location.

Expert Perspective on Finance Charges

I watch clients obsess over monthly payment amounts without ever calculating lifetime loan costs.One client picked a loan with $50 lower monthly payments, completely missing that the extended term and additional fees tacked on $8,000 to their total finance charges. Here's my advice: before you sign anything, calculate the complete finance charge—take your total payments, subtract the principal, then add every fee. That single number reveals the true borrowing cost and makes comparison shopping actually meaningful instead of confusing

— Jennifer Hartman

Frequently Asked Questions About Finance Charges

Finance charges capture the complete cost of borrowed money—interest combined with every fee, insurance requirement, and charge your lender imposes. The gap between what you borrow and what you ultimately repay reveals the actual price you're paying for credit access.

Savvy borrowers dig past advertised interest rates to calculate total finance charges before committing. A loan with a lower rate but substantial fees frequently costs more than a slightly higher rate with minimal fees. APR provides standardized comparison tools, but calculating actual finance charge dollar amounts gives you the clearest view of what you'll pay.

Cutting finance charges demands strategic action: boosting your credit score before applying, shopping across multiple lenders, negotiating fees aggressively, selecting shorter terms when your budget allows, and making extra principal payments whenever possible. These approaches can preserve thousands of dollars across a loan's lifespan.

Federal disclosure mandates exist because finance charges significantly shape your financial health. A $300,000 mortgage might accumulate $400,000 in finance charges over three decades—more than the home's original price tag. Grasping what you're paying for and why costs fluctuate empowers you to make borrowing choices that advance rather than undermine your financial objectives.

Before you sign your next loan agreement, calculate the complete finance charge, compare it across potential lenders, and verify you understand every component. That homework separates borrowers who control their debt from those whose debt controls them.