Young homebuyers meeting with a mortgage advisor in an office

FHA Loan Requirements for Homebuyers in 2026

Content

Since Franklin D. Roosevelt signed the National Housing Act in 1934, the Federal Housing Administration has opened doors for everyday Americans who'd otherwise watch homeownership from the sidelines. Right now, if you're sitting on the fence wondering whether you'll ever qualify for a mortgage with your 620 credit score and $10,000 in savings, FHA might be your ticket in. But here's the thing—you can't just walk in and expect approval. There are hoops to jump through, standards to meet, and plenty of fine print that trips up unprepared buyers.

What Is an FHA Loan and Who Qualifies?

Think of FHA as the friend who co-signs your apartment lease, except instead of your buddy vouching for you, it's the federal government. The FHA backs mortgages issued by regular banks and mortgage companies. When a lender knows Uncle Sam will cover their losses if you default, they suddenly become a lot more willing to work with borrowers who don't fit the conventional lending mold.

Here's what makes this different from standard mortgages: the government insures your loan through the Department of Housing and Urban Development. Private lenders—your Wells Fargos, Quicken Loans, and local credit unions—actually hand you the money, but they're protected if things go south.

Who benefits? Picture a 28-year-old dental hygienist with student loans, a 580 credit score from a rough patch during the pandemic, and $15,000 saved up. Conventional lenders would laugh her out of the office. FHA lenders will sit down and crunch numbers. Or consider a self-employed graphic designer whose income looks erratic on paper, even though he pulls in $75,000 annually. FHA programs understand these real-world situations better than conventional underwriting formulas do.

Author: Hannah Kingsley;

Source: nayiyojna.com

You need steady work—generally two years in the same industry, though not necessarily the same company. You'll need Social Security documentation proving you're authorized to work here. The property you're buying has to become your actual home within two months of closing, not an investment property or vacation spot. And your income needs to realistically cover the payments plus your existing debts.

Current FHA lending caps shift annually with housing markets. In 2026, you're looking at $498,257 for most counties, jumping to $1,149,825 in expensive markets like San Francisco or Manhattan. These limits keep the program focused on starter homes and middle-market properties rather than luxury estates.

Minimum Credit Score Standards for FHA Approval

The official floor sits at 500, but let's be real—finding a lender who'll approve someone at 500 is like finding a unicorn. Most want at least 580 to unlock the 3.5% down payment option. Drop below that, and you're staring at a 10% down payment requirement that defeats the whole purpose for many buyers.

Here's where it gets frustrating. FHA headquarters says 580 is acceptable. But Branch Manager Jennifer at your local bank says she needs 620. Why? She's implementing what insiders call "overlays"—basically, her company's extra safety requirements layered on top of FHA's baseline rules. One lender might work with 580, while another demands 640. This makes shopping around absolutely critical rather than optional.

Author: Hannah Kingsley;

Source: nayiyojna.com

Your score dictates your rate, period. Someone with 640 might pay 6.75% while their 720-score neighbor gets 6.0%. On a $300,000 thirty-year loan, that's $138 more per month, or roughly $50,000 over the loan's lifetime. Not pocket change.

Past financial disasters don't permanently disqualify you. Bankruptcy? Wait two years after Chapter 7 discharge or make payments for twelve months under Chapter 13. Foreclosure? Three years from completion. Short sale? Same three-year window. The clock resets from the date your name comes off the property, not when you first missed payments. Documented hardships—cancer treatment that buried you in bills, a factory closure that ended your career—can sometimes shorten these waiting periods. You'll need evidence: medical records, layoff notices, that sort of documentation.

Lenders scrutinize patterns, not just scores. Five late payments last year concern them more than a single collection account from 2019. Opening four new credit cards in six months raises red flags. Sometimes paying off old collections backfires by resetting the "date of last activity," making old debts look fresh again. Counterintuitive? Absolutely. But understanding these quirks prevents costly mistakes.

How Much Down Payment Do You Need?

That 3.5% minimum turns heads because it makes expensive markets suddenly accessible. A $400,000 condo needs just $14,000 down instead of the $80,000 you'd need for conventional financing with 20% down. Below 580? Brace yourself for 10%, which on that same condo means $40,000—still less than conventional, but substantially more demanding.

Author: Hannah Kingsley;

Source: nayiyojna.com

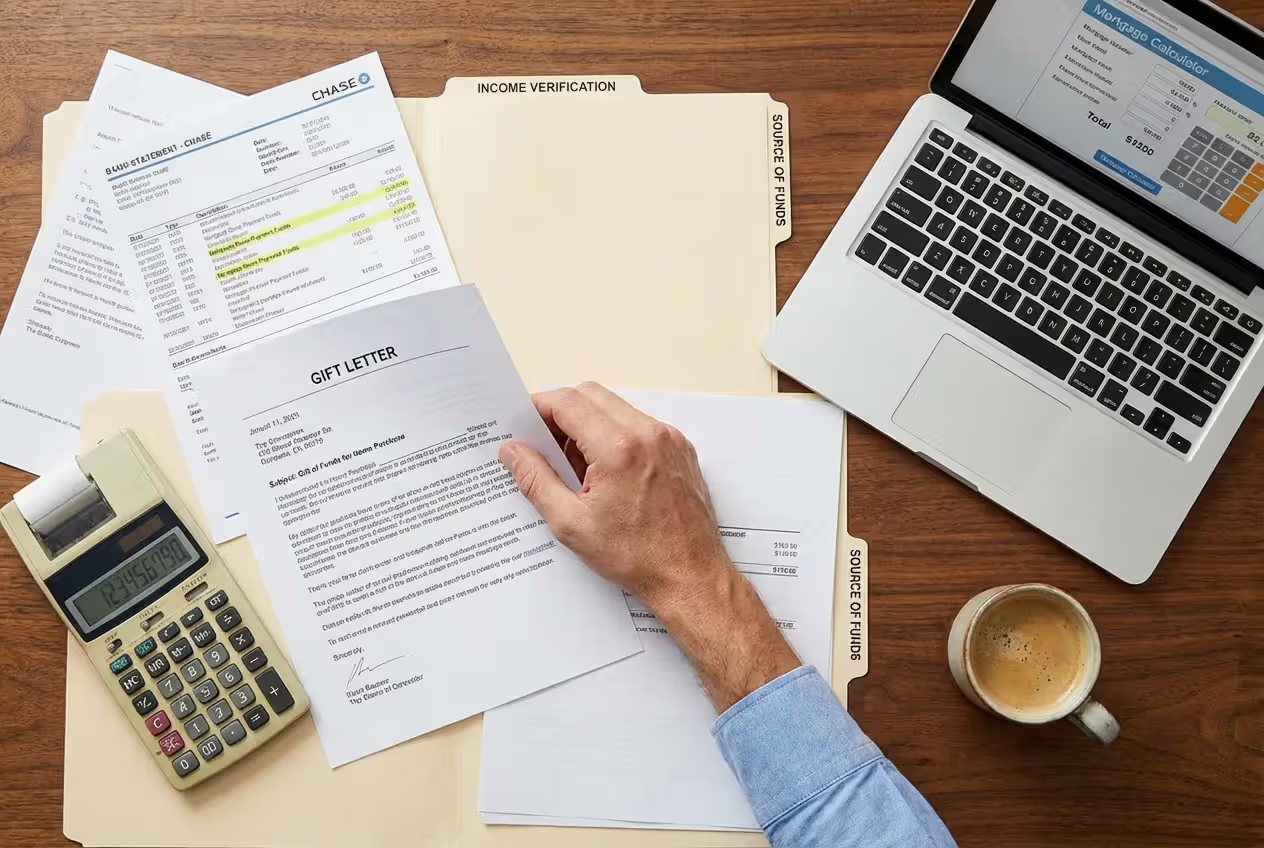

Now comes the paperwork avalanche. Every dollar must have a provable origin story. Lenders want 60 days of bank statements showing your down payment slowly accumulating, not appearing overnight. Acceptable money sources include:

- Your checking or savings accounts that you've had for months

- Pulling from your 401(k)—though you'll owe taxes and possibly penalties, making this expensive

- Selling your Toyota Camry and using the proceeds

- Gifts from relatives, your employer, or approved charitable groups

- State or local down payment assistance programs, which have exploded in recent years

- Legitimate grants from housing nonprofits

Gift funds trip up countless buyers because documentation requirements are strict. Your mom can't just hand you $8,000 cash. She needs to write a letter saying "This is a gift, not a loan. I expect zero repayment." You need bank records showing the money leaving her account and landing in yours. She needs to prove she actually had $8,000 sitting around—usually with her own bank statements. Sounds paranoid? Lenders are hunting for disguised loans that would affect your debt ratios and therefore your ability to repay.

Buyers increasingly blend multiple sources. Maybe you've got $6,000 saved, your parents kick in $4,000, and a state first-time buyer program provides $3,500. Stack them up, document each separately, and you're good. Just don't try explaining a mysterious $13,500 deposit that appeared yesterday—that'll grind your approval to a halt.

Down payment assistance has mushroomed beyond recognition. Ohio offers forgivable loans to teachers buying in certain zip codes. California runs programs for healthcare workers. Texas targets veterans. Many require income caps—say, 80% of area median income—and completion of homebuyer education classes. Some offer pure grants; others provide second mortgages that disappear if you stay five years. Research your state housing finance agency website; there's likely more help available than you realize.

One mistake derails deals constantly: large unexplained deposits. If you deposit anything exceeding roughly 1% of the purchase price within 60 days of applying, expect interrogation. Your aunt's $5,000 birthday check? Better get her gift letter ready. Sold concert tickets for cash and deposited $1,200? You'll need to explain that too.

Income and Debt-to-Income Ratio Limits

Author: Hannah Kingsley;

Source: nayiyojna.com

Underwriters calculate two ratios from your gross monthly income. The "front-end" ratio covers housing costs only: mortgage principal, interest, property taxes, homeowners insurance, HOA fees, and mortgage insurance. If you gross $6,000 monthly and your housing payment totals $1,800, that's a 30% front-end ratio. The "back-end" ratio adds every other monthly debt—your Kia payment, Discover card minimum, student loans, and that personal loan from when your furnace died. If those add $900 to your obligations, you're at $2,700 total, or 45% back-end.

FHA traditionally prefers 31% front and 43% back. But—and this is crucial—these aren't concrete walls. They're more like guidelines that bend with the right pressure. Compensating factors that push ratios higher include:

- Minimal debt outside the mortgage

- Fat cash reserves—say, six months of payments sitting in savings

- Putting down 15% instead of 3.5%

- Proven track record of paying rent exceeding your proposed mortgage

- Credit scores above 680

- Conservative credit use with cards carrying low balances

- Verifiable income growth—maybe you just finished your nursing degree and received a significant raise

I've seen approvals at 52% back-end ratios when borrowers brought multiple compensating factors. A teacher with a 730 score, $30,000 in savings, 15% down, and virtually no consumer debt got approved despite high housing costs relative to income. Every situation gets evaluated holistically rather than through rigid formulas.

Documentation requirements shift by employment type. W-2 employees provide recent pay stubs, two years of W-2s, and verification that they're still employed. The self-employed face tougher scrutiny: two years of personal tax returns plus business returns if you've incorporated, profit and loss statements for the current year, and occasionally a CPA letter confirming everything's legitimate. Lenders average your self-employment income across 24 months, which can hurt if you're on an upward trajectory. Earned $40,000 in year one and $70,000 in year two? They'll use $55,000 for qualification purposes, ignoring your actual current income.

Irregular income creates complications. Commission salespeople, freelancers working gigs, and seasonal workers must demonstrate two-year histories. If your income bounces wildly—$80,000 one year, $45,000 the next—lenders get nervous about consistency. They'll probably average it, maybe even weight it toward the lower number if they're conservative.

Some debts vanish from your ratios under specific conditions. Car payments with nine months remaining? Many lenders exclude those. Student loans in deferment still count, but underwriters can use your actual payment amount if deferment extends twelve months past closing. This changed from older rules requiring calculation of 1% of the total balance as a hypothetical payment, which was brutal for borrowers with $80,000 in deferred student debt.

The FHA program continues to serve as a critical bridge to homeownership for working families who play by the rules but lack generational wealth for large down payments. Our 2025 data shows FHA loans consistently deliver lower default rates than their risk profiles would predict, proving that responsible lending combined with proper counseling creates successful homeowners

— Adriana Gutierrez

FHA Occupancy and Residency Rules

Here's a non-negotiable requirement that's caused legal problems for buyers who didn't take it seriously: you must actually live in the property as your main residence. Not your weekend place. Not your rental property. Your primary home where you sleep most nights.

The timeline is firm—move in within 60 days after closing. That window accommodates reasonable delays like finishing a current lease, completing minor renovations, or coordinating a job relocation. But you can't buy a property in March, leave it vacant until September, and claim you intended to occupy it. That's mortgage fraud, which carries federal penalties nobody wants to experience.

FHA requires you to maintain primary residency for at least one year. After twelve months, life happens and you gain flexibility. Need to relocate for work? Fine. Want to buy a bigger home because you had twins? Go ahead. The critical milestone is that first year of genuine occupancy.

Several legitimate exceptions exist before that one-year mark. Military personnel receiving PCS orders can move immediately—the government doesn't expect you to refuse deployment to satisfy a mortgage requirement. Job relocations beyond 100 miles trigger similar exceptions. Major family size changes might justify early moves; nobody expects you to cram four people into a one-bedroom condo if you had triplets.

Co-borrower scenarios work differently than many assume. If two people take out the loan together, just one must occupy the property. This allows adult children to buy homes with parental co-borrowers who live elsewhere, or unmarried partners where only one will actually occupy the property. The occupying borrower must genuinely live there—you can't game this rule.

You can't simultaneously have two FHA mortgages except in narrow circumstances. Relocating for work more than 100 miles away and unable to sell your current FHA home? You might qualify for a second FHA loan. Legitimately outgrowing your home—maybe you've added three kids since buying that starter condo—could also justify a second loan before selling the first property. These aren't automatic approvals; expect documentation requirements and lender scrutiny.

Vacation properties and investment houses are explicitly off-limits. Dreaming of a ski condo in Colorado or a rental duplex that'll generate income? Great, but find conventional financing. FHA won't touch those transactions.

Property Standards and Appraisal Requirements

FHA property standards protect buyers from purchasing money pits while also protecting the insurance fund from properties likely to deteriorate rapidly. These requirements exceed what conventional loans demand, occasionally frustrating sellers but ultimately benefiting buyers who might not catch serious issues during excitement of purchasing.

Every purchase requires an appraisal from an FHA-approved appraiser. This professional does two jobs: determining market value and checking FHA compliance. They're not conducting a full home inspection—don't expect them to test every electrical outlet or check inside walls. But they evaluate visible conditions and major systems with a more critical eye than conventional appraisers.

Properties must provide safe, adequate housing conditions. The appraiser focuses on several key areas:

Foundation and structure: Cracks wider than a quarter-inch, sagging rooflines, or visible structural movement trigger repair requirements. The appraiser won't tear into walls, but obvious problems can't be ignored.

Roofing: Roofs need at least two years of remaining useful life. Missing or damaged shingles, visible wear, or evidence of leaks require fixes. If the roof looks questionable, appraisers call for replacement or a licensed contractor's certification that it'll last another 24 months.

Water and plumbing: Wells must be tested for flow and water quality. Septic systems need inspection and certification. City water and sewer make this simpler, but private systems face extra scrutiny.

Heating: A permanent heating system is mandatory—space heaters don't count. The system must actually work; appraisers often request sellers demonstrate functionality during cold weather inspections.

Safety issues: Peeling paint on homes built before 1978 raises lead-based paint red flags. Exposed electrical wiring, missing stair handrails, or damaged steps require correction. Properties with obvious hazards won't pass until fixes are completed.

Access: Properties need legal access via public roads or recorded easements. Landlocked parcels without proper access rights don't qualify. Driveways or pathways must be passable year-round, not washed out by rain or impassable in snow.

Property types: Single-family homes qualify easily. Condos must be in FHA-approved projects—the whole building gets certified, not individual units. Townhouses work fine. Multi-family properties up to fourplexes qualify, potentially offering house-hacking opportunities. Manufactured homes need specific construction certifications and must be permanently attached to land you own. Co-ops rarely qualify due to ownership structure complexities.

Common deal-killers include:

- Peeling exterior paint on older homes (pre-1978 paint might contain lead)

- Missing or damaged handrails on stairs

- Broken or cracked windows

- Non-functioning appliances if they're included in the sale

- Evidence of termites or other wood-destroying insects

- Standing water or poor drainage near foundations

- Missing smoke or carbon monoxide detectors

Author: Hannah Kingsley;

Source: nayiyojna.com

When appraisers identify required repairs, someone must complete them before closing. Your purchase contract usually determines financial responsibility—buyer pays, seller pays, or you split costs. After repairs, re-inspection confirms completion. Minor repairs sometimes get escrowed with funds held at closing until work finishes, but major structural or safety issues require pre-closing resolution.

Condominiums face additional hurdles beyond the individual unit's condition. The entire condominium project must carry FHA approval. The association needs adequate insurance, specific owner-occupancy ratios, and demonstrated financial stability. Many associations choose not to pursue FHA certification, inadvertently excluding buyers who need FHA financing.

Fixer-uppers typically don't work with standard FHA loans because properties must meet all standards at closing. However, the FHA 203(k) rehabilitation loan finances both purchase and renovation in a single mortgage. This program demands more documentation and oversight—contractor bids, work specifications, draw schedules, inspections throughout renovation—but it unlocks properties needing significant work that wouldn't otherwise qualify.

FHA vs. Conventional Loans: Requirement Breakdown

| Requirement | FHA Financing | Conventional Financing |

| Credit Score Floor | 580 for 3.5% down; 500 for 10% down (though lender overlays often raise this) | Generally 620-640 minimum depending on lender |

| Down Payment | As low as 3.5% with 580+ score; 10% for 500-579 scores | 3-5% available but triggers PMI; 20% avoids PMI entirely |

| Debt Ratio Limits | Typically 31/43 but flexible to 50%+ with compensating factors | Usually 36-45%; less flexibility at higher ratios |

| Mortgage Insurance | 1.75% upfront plus 0.55-0.80% annually; permanent if under 10% down | PMI required under 20% down but cancels at 78% LTV |

| Property Condition | Strict safety and habitability inspection; must meet detailed standards | Basic valuation; far fewer condition requirements |

| Borrowing Limits | $498,257 to $1,149,825 based on county costs | Conforming cap: $766,550 standard areas; $1,149,825 high-cost counties |

| Occupancy Rules | Primary residence only; must move in within 60 days | Primary residence, second home, or investment property all permitted |

Frequently Asked Questions About FHA Loans

FHA financing opens homeownership doors for buyers who'd otherwise wait years building savings or repairing credit. The trade-offs—permanent mortgage insurance with small down payments, strict property condition requirements, and occupancy mandates—matter less than the fundamental opportunity to purchase rather than rent.

Start with brutal honesty about your current position. Pull credit reports from Experian, Equifax, and TransUnion at least three months before applying, giving yourself time to dispute errors or address fixable problems. Calculate your current debt-to-income ratios using online calculators to understand realistic affordability. Document your down payment sources meticulously—don't wait until you're under contract to realize you can't prove where your money came from.

Shop among multiple FHA-approved lenders since overlay policies vary dramatically. One might demand 620 while another accepts 580. Interest rate quotes will differ. Customer service quality ranges from stellar to abysmal. Don't assume your current bank offers competitive FHA terms—mortgage broker relationships sometimes unlock better pricing.

Property selection deserves strategic thinking beyond just finding a home you love. Older properties, homes with obvious deferred maintenance, or those showing visible damage might fail FHA appraisals or require expensive repairs before closing. Working with a real estate agent experienced in FHA transactions prevents pursuing properties that won't qualify, saving emotional energy and wasted earnest money.

Mortgage insurance costs merit long-term planning beyond just getting approved. That permanent annual premium on loans under 10% down translates to tens of thousands over 30 years. Many buyers use FHA as an entry strategy, then refinance to conventional loans after building equity and improving credit scores to eliminate ongoing insurance premiums. Run the numbers—refinancing often makes financial sense within 3-5 years.

The FHA program's mission hasn't changed since the 1930s: expanding homeownership access to creditworthy borrowers facing conventional lending barriers. Understanding specific requirements—credit thresholds, documentation standards, property conditions, occupancy mandates—positions you to navigate the process smoothly rather than encountering surprises that derail your plans. With proper preparation and realistic expectations, FHA financing can launch your homeownership journey years earlier than traditional mortgages would allow.