Homeowner reviewing home equity financing in front of a suburban house

What Is a Home Equity Loan and How Does It Work

Content

Your home's worth $380,000 on paper. You've paid down the mortgage to $220,000. That $160,000 difference? It's equity you actually own—and you can borrow against it.

Thousands of homeowners tap this equity every year. Maybe you're staring at a $45,000 quote to replace your entire HVAC system. Or consolidating $30,000 in credit card balances charging you 24% interest. Perhaps your son got into an out-of-state college and financial aid fell short.

Here's the core advantage: borrowing costs run dramatically lower than credit cards or personal loans. We're talking 8% versus 18% or higher. But—and this matters—your house secures the debt. Miss payments long enough, and foreclosure becomes reality, not just a theoretical risk.

Let me walk you through exactly how these loans function, what they'll cost you, and whether tapping your equity actually makes sense for your situation.

Author: Olivia Stratfor;

Source: nayiyojna.com

Home Equity Loan Meaning and Basic Definition

Picture taking out a second mortgage that sits alongside your original one. The bank cuts you a single check for the full amount—say, $65,000—deposited straight into your account. Then you pay it back monthly, just like your first mortgage, usually over 5 to 20 years.

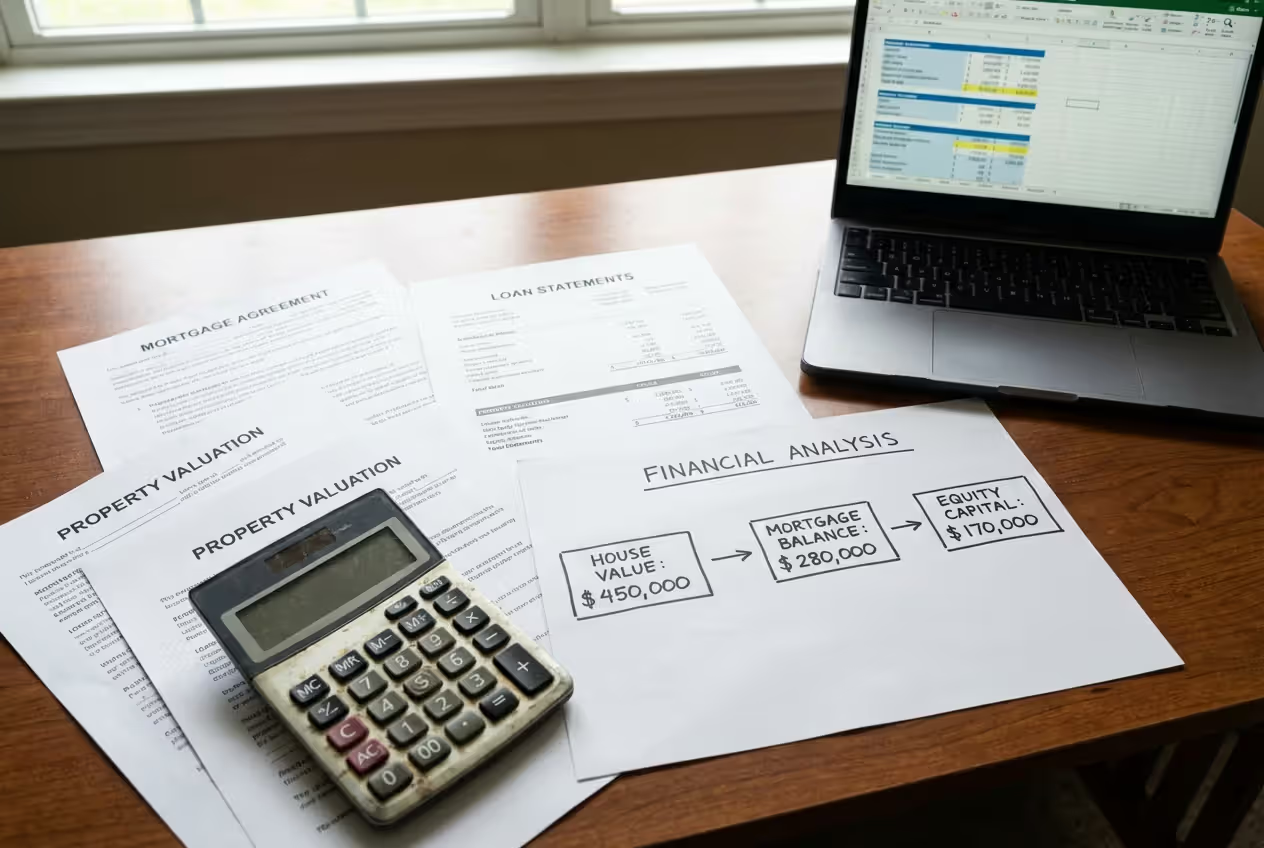

Your equity is simple subtraction. Current home value minus what you owe equals equity. Own a $450,000 house with a $280,000 mortgage? You've got $170,000 in equity built up through a combination of paying down principal and (hopefully) property appreciation.

Banks won't let you borrow every dollar of that equity, though. They typically cap you at 80-85% of your home's total value, minus your existing mortgage. Run those numbers on our example: 80% of $450,000 equals $360,000. Subtract your $280,000 mortgage, and you can borrow up to $80,000. At 85%, that ceiling jumps to $102,500.

This differs completely from a home equity line of credit (HELOC), which works like a credit card secured by your house—you draw what you need, when you need it. Cash-out refinancing replaces your entire first mortgage with a bigger one. Each option fits different scenarios, and choosing wrong can waste thousands in fees or interest charges you didn't need to pay.

Author: Olivia Stratfor;

Source: nayiyojna.com

How Home Equity Loans Work

Borrowing Against Your Home's Equity

Lenders evaluate your combined loan-to-value ratio—CLTV in industry speak. They add your current mortgage balance to your proposed new loan, then measure that total against your home's appraised value. Most stop at 80-85% CLTV, though some stretch to 90% if your credit's exceptional.

Here's a real-world example. Your property just appraised at $525,000. Your current mortgage sits at $315,000. With an 80% CLTV limit, your total debt can't exceed $420,000. You're already carrying $315,000, leaving $105,000 available. Push that to 85% CLTV, and you could access up to $131,250.

The lender files a second lien on your property. If foreclosure happens (worst-case scenario), your original mortgage lender gets paid first from the sale proceeds. The equity lender collects from whatever's left. This subordinate position creates slightly more risk for them, which explains why these rates run a bit higher than first mortgages—but still way below unsecured debt like credit cards.

Interest Rates and Loan Terms

Rates stay fixed for the entire repayment period—that's the defining feature. Your payment amount never changes, regardless of what the Federal Reserve does or where markets head. As of 2026, expect rates between 7.5% and 10%, depending on your credit score, how much you're borrowing, and which lender you pick.

Got a 760 credit score? You'll land near the bottom of that range. Sitting at 640? You're looking at the higher end, if you even get approved.

Most lenders offer 5, 10, 15, or 20-year terms. Shorter terms mean fatter monthly payments but massive interest savings. Borrow $60,000 at 8.25% over 10 years, and you'll pay roughly $733 monthly with about $27,960 in total interest. Stretch that same loan to 20 years, and monthly payments drop to $511—but you'll shell out approximately $62,640 in interest over the loan's life. That's paying an extra $34,680 for the privilege of lower monthly obligations.

Author: Olivia Stratfor;

Source: nayiyojna.com

Rate predictability helps you budget with confidence. Unlike variable-rate HELOCs that can spike when the Fed raises rates, your payment stays identical month after month. The downside? If rates plummet to 5%, you're still stuck at 8.25% unless you refinance—which means paying closing costs all over again.

The Application and Approval Process

Think of it as your original mortgage process, condensed. You'll submit recent pay stubs (last 30 days), your previous two years of W-2 forms or full tax returns if self-employed, two months of bank statements, and details about your current mortgage. The lender orders a professional appraisal—budget $450 to $650 for this, depending on your area and property size.

Underwriters calculate your debt-to-income ratio obsessively. They total up every monthly debt payment you make (mortgage, car loans, student debt, minimum credit card payments), add the proposed equity loan payment, then divide by your gross monthly income. Most want that number under 43%. Some stretch to 50% for borrowers with 740+ credit scores and rock-solid income history.

They'll pull your credit reports from all three bureaus. Recent late payments, collections accounts, or bankrupties within the past seven years can derail your application fast.

Timeline runs about three to six weeks from application to closing. Closing day brings a stack of documents and fees typically totaling 2-5% of your loan amount. You're paying for origination charges, title searches, recording fees, and possibly discount points if you're buying down your rate. Some lenders advertise "no closing costs," but they're just baking those expenses into a higher interest rate instead.

Home Equity Loan Repayment Structure

Payments start immediately—usually within 30 days of closing. Every payment gets split between principal and interest through amortization. Early on, most of each payment goes toward interest. As you chip away at the principal, that ratio flips.

Check out an amortization schedule (your lender provides this). On an $80,000 loan at 8.5% over 15 years, your first payment of $788 breaks down to roughly $567 in interest and just $221 reducing your actual debt. Jump ahead to payment 150, and about $550 attacks principal with only $238 going to interest.

Selling your house before the loan's paid off? You'll need to satisfy the balance at closing. The title company pays your first mortgage, then your equity loan, from the sale proceeds. Whatever remains goes into your pocket. If you're underwater—owing more than the sale price—you'll either bring cash to closing or negotiate a short sale with both lenders.

Refinancing your primary mortgage doesn't automatically wipe out your equity loan. You've got options: pay it off as part of the refinance, leave it in place as a continuing second lien (assuming your new lender allows this), or roll it into your new first mortgage if your finances support larger borrowing. Each path changes your rate, fees, and monthly payment in different ways.

Common Reasons Homeowners Use Equity Loans

Home improvements top the list by a wide margin. New roof? That's $15,000 to $30,000 depending on size and materials. Outdated electrical panel creating fire hazards? Another $3,000 to $8,000. Adding a bathroom in your three-bedroom, one-bath house? Budget $25,000 to $50,000 minimum.

The calculation that matters: will improvements add value matching or exceeding their cost? Kitchen remodels typically return 60-80 cents per dollar spent when you sell. Bathroom additions can return 50-70%. But that backyard pool you've always wanted? Most markets see 30-50% return—sometimes less. You're paying for lifestyle, not building wealth.

Debt consolidation makes compelling mathematical sense when executed properly. Carrying $35,000 across five credit cards at 19-24% APR? Your minimum payments probably run $1,200+ monthly, and you're barely touching principal. Consolidate into a 10-year equity loan at 8.75%, and your payment drops to around $445 while guaranteeing you're debt-free in exactly 120 months. The danger: running up fresh credit card balances afterward. You've just swapped unsecured debt for secured debt against your house, then added new unsecured debt on top. That's financial quicksand.

Author: Olivia Stratfor;

Source: nayiyojna.com

Large one-time expenses sometimes justify equity borrowing. Emergency medical procedures insurance won't cover. A daughter's wedding (though maybe reconsider that $50,000 budget). Business startup capital when you've exhausted SBA loan options. College tuition after maxing out federal student loans—especially since private student loans can charge 11-14%.

What doesn't make sense: vacations, new cars, routine living expenses, or anything discretionary. You're putting your home at risk for items that don't build wealth or solve genuine emergencies.

These loans work best when you need a specific amount for a defined purpose, your income's stable, and you've mapped out clear repayment. They work terribly when covering ongoing expenses, when your job's shaky, or when you're already stretching financially. Adding a $650 monthly payment when you're already tight? That's asking for trouble.

Home Equity Loan Requirements and Eligibility

Credit score minimums typically start at 620, but that's barely getting your foot in the door with lousy rates. Cross 700, and pricing improves noticeably. Hit 740+, and you access the best rates available. A 640 score might lock you at 10.25%, while a 770 score could secure 7.5%—that spread costs you roughly $8,500 in extra interest on a $70,000 loan over 15 years.

You'll need minimum 15-20% equity already built up. Recent homebuyers often don't qualify unless they made substantial down payments (20%+ at purchase) or bought in markets that have appreciated rapidly. Bought two years ago with 5% down? You probably don't have enough equity yet unless your local market's exploded value-wise.

Lenders verify equity through professional appraisals, not Zillow or Redfin estimates. Those online tools can miss by 10-15% or more, especially in neighborhoods with diverse housing stock.

Debt-to-income thresholds usually max out at 43%, though some lenders stretch to 50% for stellar credit profiles. Here's the math: monthly gross income of $8,500, current debts totaling $2,800, proposed equity loan payment of $625. Your DTI hits 40.3% ($3,425 ÷ $8,500). You're probably getting approved. Push that to 45%, and you'll face either rejection or demands for additional documentation proving income stability.

Documentation requirements include complete tax returns (both years) if you're self-employed or earn commission income, 60 days of bank statements showing all pages, your most recent pay stubs, and written explanations for any large deposits over $1,000. Lenders want confirmation that money flows consistently and sufficiently. Employment gaps in the past two years, frequent job hopping, or declining income trends all trigger extra scrutiny.

Expert Perspective

I tell homeowners their equity represents financial insurance, not a spending account waiting to be tapped. Before borrowing a dime, ask yourself whether this loan strengthens your financial position five years from now. Consolidating debt? Have you actually addressed the spending habits that created that debt in the first place? Planning renovations? Will these improvements add lasting value, or are you just upgrading to your personal taste? The absolute lowest rate available becomes completely meaningless if you're borrowing for wrong reasons or can't sustain payments during job loss or medical emergencies

— Jennifer Martinez

Risks and Considerations Before Borrowing

Foreclosure represents the nightmare scenario, but it happens to real people every year. Your property secures both mortgages. Default on either one, and the lender can foreclose. Unlike credit card debt—where consequences include damaged credit and maybe wage garnishment—equity loan default can literally render you homeless.

The 2008 financial crisis burned millions who'd borrowed heavily against equity, then couldn't sustain payments when income dropped or property values collapsed. Housing markets can decline. Jobs can disappear. Medical emergencies can drain savings. Adding a second mortgage payment reduces your financial cushion for handling these shocks.

Closing costs typically run $2,500 to $6,000 depending on loan size and location. Borrowing $55,000? That's 4.5-11% of your loan disappearing into fees you'll never recoup. Some borrowers roll these costs into the loan principal, but then you're paying interest on fees for the next 10-20 years. A $4,000 closing cost financed at 8.5% over 15 years actually costs about $6,900 after interest.

Author: Olivia Stratfor;

Source: nayiyojna.com

Property value drops can trap you. Borrow today when your home's worth $400,000, and suppose values decline 15% over two years (it happened in 2008-2010 in many markets). You might owe more than the house is worth, making selling impossible without bringing substantial cash to closing. This "underwater" situation destroys mobility if you need relocating for a job transfer or face life changes like divorce requiring asset liquidation.

Opportunity cost deserves serious thought. That $575 monthly payment over 15 years totals $103,500. Could that money compound better in retirement accounts? A consistent $575 monthly investment earning 8% annually grows to approximately $197,000 over 15 years. Borrowing only makes financial sense when benefits exceed what you're sacrificing in investment growth.

Comparing Your Borrowing Options

| Loan Type | How You Receive Funds | Rate Structure | How You Pay It Back | Works Best For |

| Home Equity Loan | Single lump sum deposited at closing | Fixed rate throughout entire term | Identical monthly payments over 5-20 years | One-time expenses with known costs; borrowers prioritizing payment predictability |

| HELOC | Draw what you need during 10-year access period | Variable rate tied to prime rate | Interest-only during draw period, then principal + interest | Projects with uncertain or phased costs; borrowers comfortable with payment fluctuations |

| Cash-Out Refinance | Single lump sum at closing (difference between new and old mortgage) | Fixed rate on entirely new first mortgage | Identical monthly payments over 15-30 years | Large borrowing needs combined with high existing mortgage rate; consolidating multiple liens |

Frequently Asked Questions About Home Equity Loans

Equity loans deliver powerful access to capital at rates that beat credit cards and personal loans by massive margins. But you're fundamentally changing your risk profile—converting unsecured obligations or unfunded needs into debt secured by your home. That trade makes sense when investing in lasting value: property improvements boosting market value, education enhancing earning capacity, or debt consolidation that genuinely improves your financial trajectory.

The math must work in your favor decisively. Calculate total costs including all interest and fees, compare against alternatives like personal loans or 0% promotional credit cards for smaller amounts, and ensure monthly payments fit comfortably within your budget with cushion for unexpected expenses. General guideline: if this payment plus other debts pushes your DTI above 40%, you're stretching dangerously thin.

Timing matters considerably. Borrowing when income flows steadily, you've maintained emergency savings covering three to six months of expenses, and your job seems secure reduces risk substantially. Borrowing when already financially stressed, facing potential layoffs, or lacking savings amplifies foreclosure danger dramatically.

Consider your long-term plans carefully. Selling within three to five years? Closing costs may not justify themselves—you'll pay $3,000-5,000 in fees and barely reduce principal before selling. Planning to stay put for 10+ years? Those costs spread across many years of benefit and use.

Finally, shop aggressively across at least three lenders. Rates and fees vary shockingly between institutions. A 0.5% rate differential on a $75,000 loan over 15 years costs approximately $3,800 in additional interest—real money you could keep instead. Get quotes from your current mortgage servicer, a local credit union, and an online lender, then compare not just rates but closing costs, prepayment terms, and customer service reputation through independent reviews.

Equity loans serve millions of homeowners effectively each year, funding improvements, consolidating obligations, and covering major expenses at rates dramatically below credit cards or unsecured alternatives. But they demand rigorous analysis, honest assessment of financial stability, and complete understanding of what happens if things go wrong. Your home represents likely your largest single asset—borrowing against it should never constitute a casual decision made without considering alternatives and long-term consequences.