Veteran reviewing VA home loan documents in front of a house

How to Qualify for a VA Loan in 2026

Content

For veterans and active military members, few financial benefits match what a VA mortgage brings to the table. You can purchase a home without putting anything down, skip the monthly mortgage insurance premiums that conventional borrowers pay, and often lock in better interest rates than civilian buyers get. Yet thousands of eligible service members pass on this opportunity every year, either because they don't realize they qualify or they assume the application process is more complicated than it actually is.

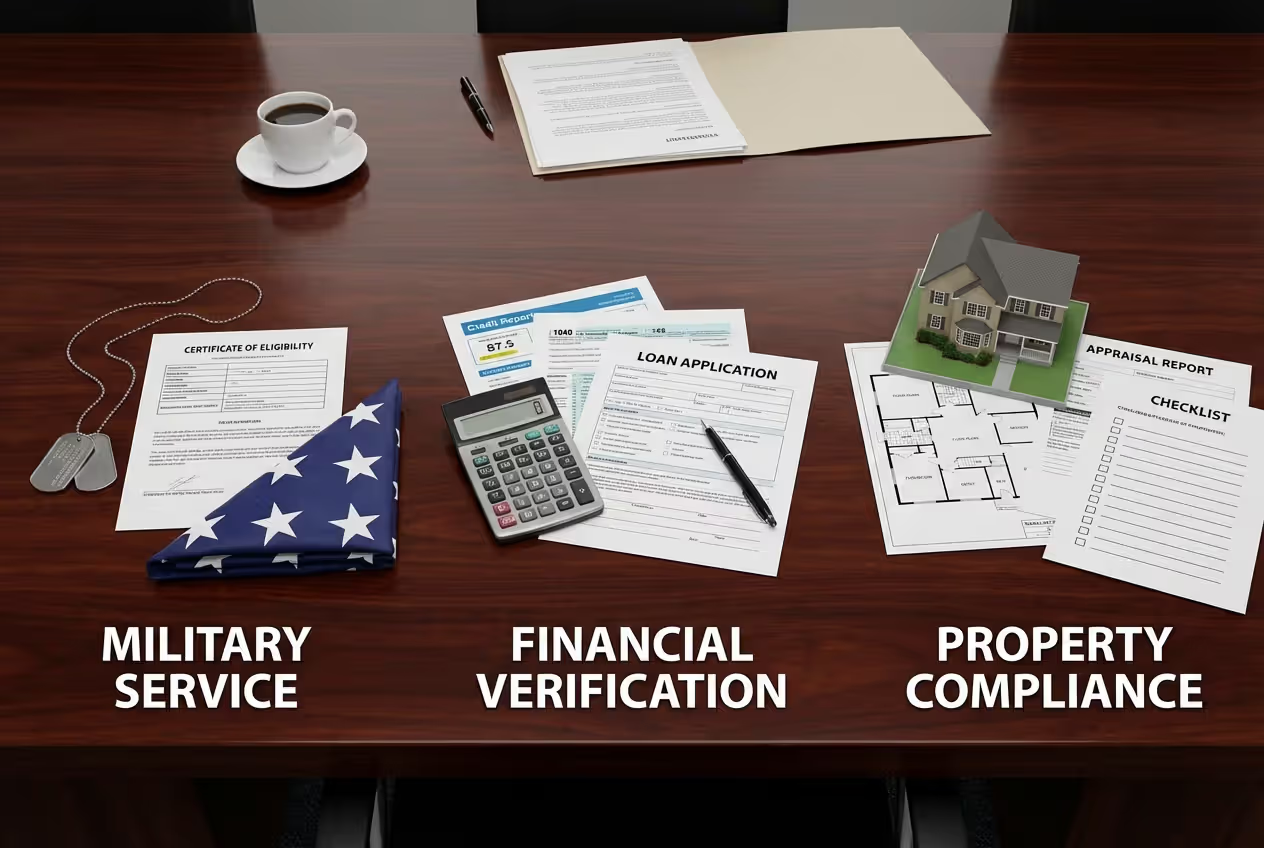

Getting approved requires meeting standards in three separate areas. First, your military record needs to show the right type and duration of service. Second, lenders will examine your finances—credit scores, monthly income, existing debts, and a unique VA calculation called residual income. Third, the home you want to buy must pass a VA appraisal and meet specific safety and livability standards. Miss any one of these three, and your application stalls.

Think of qualification as a three-legged stool. Service requirements prove you've earned the benefit. Financial requirements show you can handle the monthly obligations. Property requirements protect you from buying a home with serious defects. Let's break down exactly what you need in each category.

Author: Brandon Ellery;

Source: nayiyojna.com

What Are VA Loan Eligibility Requirements?

Three main qualifications determine whether you can use a VA mortgage. Your military background must include enough service time with the right discharge status. Your financial picture needs to show stable income, manageable debt levels, and sufficient leftover money each month after paying all bills. The property can't have safety hazards or major system failures that would make it unsuitable for financing.

Here's what trips people up: the VA doesn't actually lend you money. Private mortgage companies make VA loans, and the Department of Veterans Affairs backs a portion of each loan if something goes wrong. This guarantee lets lenders take on more risk, which translates to those zero-down-payment offers you've heard about. But "guaranteed" doesn't equal "automatic approval."

Lenders add their own requirements on top of the VA's baseline rules. One lender might approve borrowers with 580 credit scores while another won't go below 620. The VA itself doesn't set a minimum credit score—individual lenders do. Same story with income requirements and how they calculate your debt ratios.

Two myths keep coming up. First, some veterans think any honorable discharge automatically qualifies them. Not quite—you also need sufficient service time, which varies based on when you served. Second, plenty of applicants assume they need perfect credit. Wrong again. I've seen approvals for borrowers with past bankruptcies, foreclosures, and credit scores in the 500s. The key is understanding what lenders actually require versus what you've heard through the rumor mill.

VA Service Requirements Explained

Service requirements vary wildly depending on your branch, service dates, and duty status. A Reserve component member faces different thresholds than someone who served on active duty. Wartime service has different minimums than peacetime service. And surviving spouses have their own set of qualification rules.

Active Duty and Veteran Service Standards

If you're currently on active duty, you hit eligibility after serving 90 straight days during designated wartime periods or 181 consecutive days during peacetime. For separated veterans, those same timeframes apply—90 days with at least one day falling within an official war period, or 181 days of uninterrupted active service during peace.

The VA recognizes several wartime eras: World War II, Korea, Vietnam, and the Persian Gulf War (which technically never ended and includes current operations). Now here's where it gets tricky. If you joined after September 7, 1980, or became an officer after October 16, 1981, you generally need 24 continuous months of active duty or the full period you were called up, whichever is less.

Early separations create exceptions. Got discharged early because of a service-connected disability? You may qualify even if you didn't hit the standard time requirements. Same goes for hardship discharges or separation due to force reductions. On the flip side, a dishonorable discharge pretty much eliminates eligibility, though the VA does review individual circumstances. Bad conduct discharges and other-than-honorable characterizations also create problems, but they're not automatically disqualifying.

One scenario that confuses people: multiple short active duty periods. You can't always add them together. The service generally needs to be continuous unless specific exceptions apply.

National Guard and Reserve Member Requirements

Guard and Reserve members typically need six years in the Selected Reserve to qualify. That's six years of satisfactory participation—drilling one weekend per month and two weeks annual training. Get discharged before six years due to a service-connected disability? You might still qualify with less time.

Here's a workaround many don't know about. If you were activated under Title 10 orders and served enough active duty time to meet the active duty standards I mentioned earlier, you could qualify that way instead of waiting for six years of Guard or Reserve time. Some members end up with two potential paths to eligibility.

Don't make this mistake: counting all your military time as qualifying service. Your regular drill weekends don't count toward active duty minimums. Only specific activation orders meet that threshold. If you're going the six-year route, you need documentation showing satisfactory participation in the Selected Reserve, not just your initial training orders.

Surviving Spouse Eligibility

If your spouse died while serving or from a service-connected disability, you may qualify for VA loan benefits. The main catch? You can't have remarried. The VA does make exceptions if you remarried after turning 57, or if the remarriage happened after December 16, 2003—the rules changed that year.

Spouses of service members listed as MIA or POW can also qualify. Documentation gets more complex for surviving spouses. Expect to provide a DD Form 1300 (Report of Casualty) or a determination letter from the VA confirming the service-connected nature of the death.

Author: Brandon Ellery;

Source: nayiyojna.com

How to Get Your Certificate of Eligibility for a VA Loan

Your Certificate of Eligibility proves two things: you've met the service requirements, and here's how much entitlement you have available. The process has gotten significantly easier in the past few years, with most applicants now able to generate their COE instantly online.

The fastest approach uses the VA's web portal at VA.gov (which replaced the older eBenefits system for most functions). Log in with your DS Logon Premium, My HealtheVet, or ID.me credentials. If the VA's database already has your service records, you'll get a downloadable PDF certificate within minutes—literally five to ten minutes in most cases. The system cross-checks your information with DOD databases automatically.

When automated verification fails—which happens frequently for older veterans, Guard members, or anyone with complicated service histories—you'll need manual processing. Fill out VA Form 26-1880 and gather your discharge papers (DD Form 214 for veterans, NGB Form 22 for Guard members, or a Statement of Service from your commander if you're still serving). Mail everything to the Atlanta Eligibility Center. Processing typically takes one to two weeks, though volume spikes during spring homebuying season can push it to three weeks.

Your third option lets your lender handle it. Most experienced VA lenders prefer requesting COEs themselves through the WebLGY system. They have direct access to VA lender service representatives who can troubleshoot problems faster than you can working through regular channels. You'll still complete the same form and provide the same service documents, but your lender manages the submission.

Pay attention to what your COE actually shows. It displays your available entitlement, not your maximum loan amount. Thanks to 2020 changes, veterans with full entitlement can now borrow any amount a lender will approve without requiring a down payment. If you've used VA loan benefits before without restoring your entitlement (by selling the property and paying off the loan), your COE reflects your remaining entitlement. Depending on the loan amount and local conforming loan limits, this might require a down payment on expensive properties.

VA Credit and Income Guidelines

Financial qualification goes way beyond checking whether your credit score hits some minimum number. Lenders want your complete financial story—how you've handled credit historically, whether your income can cover the new mortgage payment plus your other obligations, and whether you'll have enough money left over each month to actually live on.

Minimum Credit Score Standards

The VA doesn't mandate any specific credit score. Individual lenders set their own minimums, typically ranging from 580 to 640. Most lenders cluster around 620 as their baseline. Drop below 600 and you're almost certainly getting manual underwriting, where an actual person reviews your complete file rather than relying on automated systems.

Your score matters less than what's behind it. An underwriter might prefer a borrower with a 610 score from high credit card balances but perfect payment history over someone with a 640 who's missed payments recently. Medical collections get treated more leniently than unpaid credit cards. Many lenders now ignore medical collections entirely after industry guidance shifted.

Past financial disasters carry specific waiting periods. Chapter 7 bankruptcy? You're waiting two years from the discharge date. Chapter 13 bankruptcy allows qualification after just 12 months of on-time plan payments if the court approves. Foreclosures normally require a two-year wait, though you can reduce this to 12 months if you can prove the foreclosure resulted from circumstances beyond your control—sudden disability, job loss from base closure, that sort of thing.

Debt-to-Income and Residual Income Requirements

Your debt-to-income ratio divides your total monthly debt payments by your gross monthly income. Most VA lenders want to see 41% or less, though automated systems sometimes approve ratios up to 50% when other factors compensate—high credit scores, significant savings accounts, or a track record of paying housing costs higher than your proposed mortgage.

Residual income is where VA loans differ dramatically from conventional mortgages. Instead of just confirming you can make the mortgage payment, the VA wants proof you'll have sufficient funds left after paying all debts and basic living expenses. The VA publishes minimum residual income amounts based on your geographic region, loan size, and household size.

| Region | 1 Person | 2 People | 3 People | 4 People | 5+ People |

| Northeast | $492 | $823 | $990 | $1,025 | $1,062 |

| Midwest | $459 | $755 | $909 | $940 | $973 |

| South | $492 | $823 | $990 | $1,025 | $1,062 |

| West | $547 | $902 | $1,086 | $1,117 | $1,158 |

These amounts apply to loans exceeding $79,999. Loans under $80,000 have requirements roughly 20% lower.

Calculating residual income means subtracting everything from your gross monthly income: total debt payments, estimated property taxes, homeowners insurance, utilities, basic maintenance costs, and other living expenses. Whatever remains must equal or exceed the table amount for your situation.

Let me show you how this plays out. Say you're bringing home $5,500 monthly with a family of four in the South. Under DTI rules, you could potentially handle an $1,800 mortgage payment (41% of $5,500 is $2,255, leaving room for the mortgage plus existing debts). But run the residual income calculation: $5,500 minus $1,800 (housing) minus $400 (other debts) minus $700 (taxes/insurance) minus $200 (utilities) minus $1,350 (living expenses) leaves just $1,050. You're only $25 above the $1,025 minimum requirement. That razor-thin margin might prompt your underwriter to request additional documentation or suggest a smaller loan amount.

Income verification follows standard mortgage protocols. W-2 employees submit two recent pay stubs plus two years of tax returns. Self-employed borrowers need two years of personal tax returns and business tax returns, with income averaged across both years unless trending downward. VA disability compensation counts as income. So do retirement checks and military pensions. You'll just need documentation showing these income sources will continue for at least three years.

Author: Brandon Ellery;

Source: nayiyojna.com

Steps to Qualify for a VA Mortgage

The qualification process follows a logical sequence, though your timeline will compress or stretch based on how organized your documentation is and how efficient your lender operates. Smart move? Start this process before you even begin looking at houses.

First, verify your eligibility and request your COE. Even if you're 100% certain you qualify, get that certificate now. The online process takes minutes. Having it early reveals your available entitlement and prevents surprises later when you're trying to close quickly on a property you love.

Second, find a VA-approved lender and get pre-approved. Not every mortgage company handles VA loans. Among those that do, experience levels vary dramatically. A lender who closes 50 VA loans monthly will navigate quirks and problems far more smoothly than someone who does five per year. During pre-approval, they'll pull your credit reports, verify your income, review your assets, and issue a letter stating how much you qualify to borrow.

Author: Brandon Ellery;

Source: nayiyojna.com

Third, start house hunting with that pre-approval letter. Sellers and listing agents treat offers backed by solid pre-approval more seriously, especially in competitive markets where multiple offers are common. Work with a real estate agent who knows VA loans and their property requirements inside and out. Some homes won't qualify due to safety issues, needed repairs, or property type restrictions.

Fourth, make an offer and move toward contract. Once the seller accepts your offer, your lender orders the VA appraisal. This serves two purposes: establishing the home's market value and verifying it meets VA minimum property requirements. The appraiser inspects for safety problems—peeling paint, missing handrails, malfunctioning heating systems, that kind of thing. Unlike conventional appraisals, VA appraisers must flag required repairs. The seller either completes these before closing or agrees to fund them through an escrow holdback.

Fifth, navigate the underwriting phase. Your complete loan file goes to an underwriter who verifies every detail you've provided: employment history, income sources, bank accounts, credit profile, property condition. Underwriters almost always issue conditions—requests for additional paperwork or explanations. Respond immediately. Every day of delay pushes back your closing date.

Sixth, receive final approval and close. Once underwriting issues clear-to-close, the closing department prepares final documents and schedules your signing appointment. You'll review and sign a stack of papers, the seller transfers title, and you get your keys.

During this entire timeline, maintain the status quo financially. Opening new credit cards, financing a car, switching jobs, or moving money between accounts can all trigger new underwriting conditions. Some changes can even get your approval pulled at the last minute.

Common VA Loan Qualification Mistakes to Avoid

Certain mistakes appear in application after application, causing delays or outright denials that could have been avoided with better preparation. Learn from others' errors.

Failing the residual income test catches people off guard. Applicants who easily pass DTI calculations sometimes can't meet residual income minimums, particularly in expensive markets or with larger families. Before you fall in love with a house at the top of your budget, run the residual income numbers yourself using the VA's published tables. Coming up short? Consider a less expensive property or wait for a raise or promotion.

Property condition problems kill deals regularly. The home must satisfy VA minimum property requirements, which set a higher bar than conventional loan standards. Peeling exterior paint, damaged roof shingles, broken HVAC systems, or safety hazards all require correction before closing. In hot markets, sellers frequently reject VA offers to avoid making repairs. Combat this by offering to cover certain repair costs (within VA limits) or by targeting homes in good condition.

Author: Brandon Ellery;

Source: nayiyojna.com

Credit report errors can destroy otherwise solid applications. Pull your reports from Equifax, Experian, and TransUnion at least 60 days before applying. Found errors? Dispute them immediately—the correction process often takes 30-45 days. I know a veteran who got denied because his credit showed a car loan he'd never taken out. By the time the credit bureaus corrected their mistake, someone else had bought the house.

Submitting the wrong COE documents happens constantly with Guard and Reserve members. Trying to qualify based on six years of Selected Reserve service? You need an NGB Form 22 or a current Statement of Service from your unit commander, not your basic training orders from six years ago. Wrong documentation adds weeks to COE processing.

Changing jobs mid-application requires careful handling. Switching employers doesn't automatically disqualify you, but it requires extra documentation and will likely delay closing. If you must change jobs, stay in the same career field with equal or higher pay, and tell your lender the same day you accept the offer. Never quit a job before closing without consulting your lender first—that could kill your approval entirely.

Hiding debts from your lender damages your credibility. Making payments on student loans in deferment? Paying child support? Borrowed money from family? Disclose everything upfront. Underwriters will discover these debts during verification anyway, and finding undisclosed obligations makes them scrutinize every other aspect of your application with suspicion.

The residual income requirement is the most protective feature of VA loans, yet it's the one borrowers understand least. I regularly see veterans who could technically afford the monthly payment but would be house-poor without sufficient funds for emergencies or quality of life expenses. That residual income cushion is what keeps VA loans performing better than conventional mortgages even during economic downturns

— Michael Torres

Frequently Asked Questions About VA Loan Qualification

Qualifying for a VA loan in 2026 requires meeting specific service, financial, and property standards, but millions of veterans successfully navigate this process every year. Your military service earned you this benefit—understanding the qualification requirements ensures you can actually use it when you're ready to buy a home.

Start by requesting your Certificate of Eligibility to confirm your service qualifications and check your available entitlement. Pull your credit reports to catch errors and see where your score stands. Calculate both your debt-to-income ratio and residual income before shopping for homes, establishing a realistic price range that won't leave you stretched financially.

Partner with a lender who has significant VA loan experience and can anticipate potential obstacles before they become deal-killers. Keep your employment stable and avoid major financial changes during the application process. Target properties in good condition that will pass VA minimum property requirements without extensive repairs.

VA loan benefits offer extraordinary advantages—zero down payment capability, no monthly mortgage insurance, competitive interest rates, and limited closing costs. Understanding the qualification process and organizing your documentation properly transforms these advantages from theoretical benefits into actual homeownership.