Person comparing personal loan options at home with laptop and financial documents

What Is a Personal Loan and How Does It Work

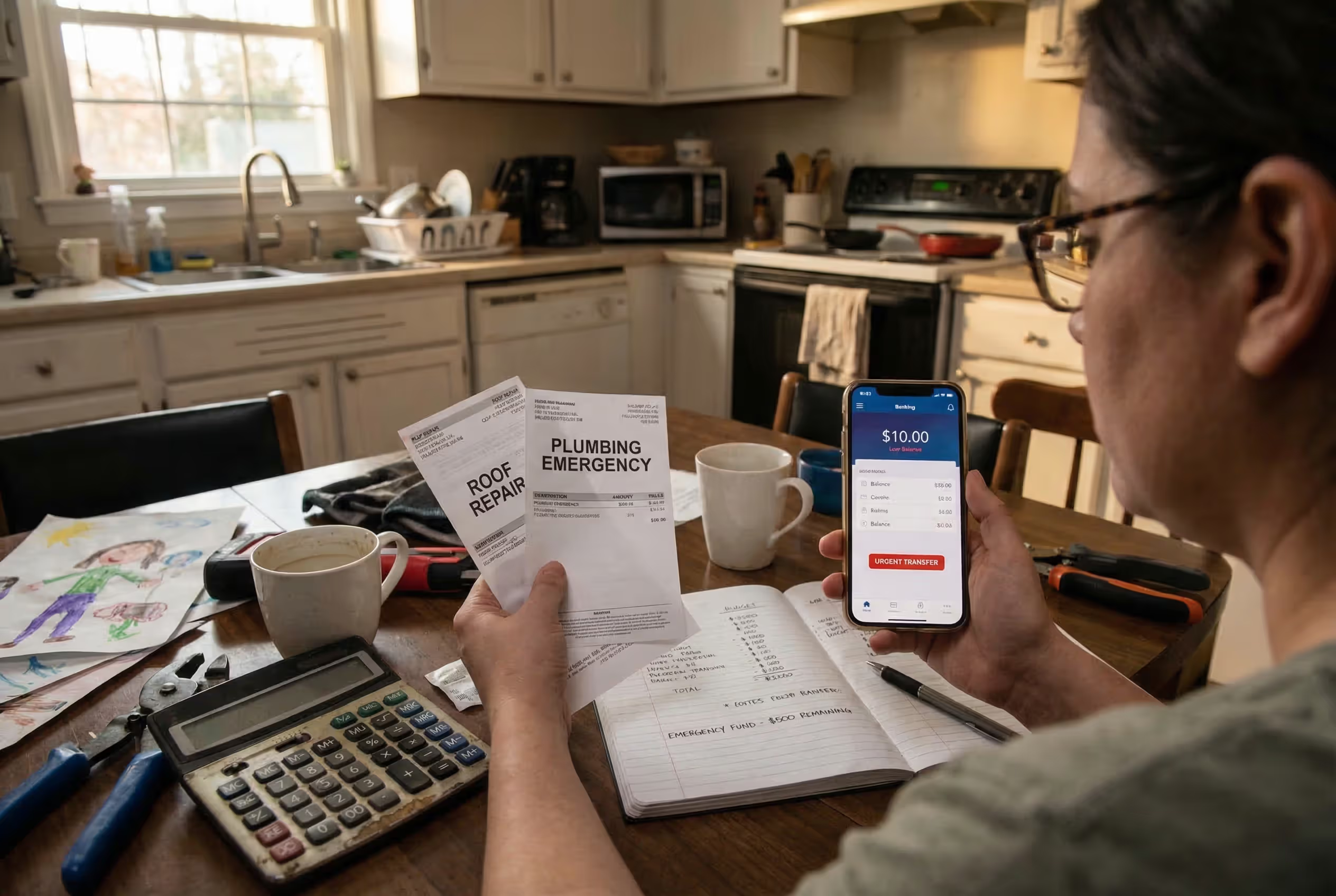

Stuck with $15,000 spread across three maxed-out credit cards? Your bathroom desperately needs an $8,000 overhaul? Personal loans can drop money straight into your checking account—sometimes in under two business days—and nobody's checking your home equity or policing how you spend it.

Here's the deal: You get one fat deposit from a bank or online lender. In return, you commit to fixed monthly payments for anywhere from two years to seven. Your interest rate? Locked the minute you sign—no surprises, no adjustments. Compare that to credit cards that bounce from 22% to 28% depending on what the Fed does, or mortgages that literally attach to your house. Personal loans sit in this middle zone where you get structure without putting up collateral.

The Federal Reserve counted about 24 million Americans juggling personal loan balances last year. Why so many? You know exactly when you'll be debt-free from day one. Your rate usually beats credit cards by 10 to 18 percentage points. And the money shows up faster than you can schedule an appointment at your local branch.

But here's what nobody mentions upfront: miss the hidden fees and you might borrow $10,000 only to hand back $17,000 over the loan's life. Understanding real costs, knowing when these loans actually help, and spotting the trap scenarios keeps you from joining the regret club.

Personal Loan Meaning and Key Features

Think of personal loans as installment debt with flexibility baked in—you get unsecured money to use however you want. Lenders wire anything from $1,000 to $100,000 in one shot. You're stuck with identical monthly bills until you hit zero, typically across 24 to 84 months.

The unsecured versus secured split: About 85% of these loans don't touch your stuff—your car title stays put, your house deed remains yours. Lenders bet on your job stability, credit history, and their gut feeling you'll pay up. If you ghost on payments, your credit tanks and lawsuits might arrive, but nobody's repossessing your Toyota. Secured personal loans exist where you hand over savings accounts, CDs, or vehicle titles as insurance. That gamble might shave 3 to 6 percentage points off your rate. Whether risking your assets for a discount makes sense depends on how confident you feel about consistent payments.

Why locked interest rates matter: In 2026, you'll find fixed APRs on basically every personal loan out there. Your rate gets stamped at approval—could land at 7.5%, might hit 22%, depends entirely on your profile—and stays frozen until your final payment. Your March installment matches what you'll pay 18 months later, down to the penny. Credit cards shift rates every quarter when prime moves. HELOCs jump around after each Fed announcement. Personal loans kill that uncertainty completely.

The one-and-done disbursement model: Once you're approved, expect one electronic transfer to your checking, usually landing within one to seven business days based on the lender's speed. Your payment clock starts ticking immediately—interest piles up the second funds arrive, and your first bill shows up roughly 30 days later whether you've touched the cash or it's just sitting there. Credit cards only charge interest on balances you actually roll month to month, which works differently.

Origination fees that slice your proceeds: Plenty of lenders subtract 1% to 8% before sending your money, and this trips up borrowers constantly. You request $10,000 from a lender charging 5% origination? $9,500 hits your account, but you're repaying the full $10,000 plus interest calculated on that complete sum. Always crunch total dollars paid across different lenders—sometimes a slightly higher rate with zero upfront fees destroys a lower rate carrying a 6% origination hit.

Author: Hannah Kingsley;

Source: nayiyojna.com

How Personal Loans Work

Whether you're tapping through an app at midnight or sitting across a desk from a loan officer, the mechanics follow similar beats with wildly different speeds.

Pre-qualification comes first: Start here every single time. Most lenders run tools where you punch in basics—annual income, rough credit score, how much you want—and they'll spit out potential rates without dinging your credit. This creates just a soft inquiry. You can check five lenders in three hours, compare who's offering what, then formally apply to whoever looks best.

The full application stage: After picking a lender, you'll upload proof: recent paystubs, last year's tax return, bank statements from the past 90 days, driver's license photos. Now they run a hard credit pull—this one knocks your score down a few points temporarily, though the damage fades across several months.

What actually drives approval: Lenders weigh five main factors. Your credit score carries massive weight—a 780 opens doors that slam shut at 630. They calculate debt-to-income ratio by adding all monthly debt obligations (car payment, student loans, minimum credit card bills, this new proposed payment) and dividing by gross monthly earnings. Most want this under 36%, though some approve borrowers at 43% when everything else shines. Job stability counts—24 straight months in your field beats hopping between three jobs across three years. Your total income needs to realistically cover existing bills plus this new monthly hit. Finally, your stated purpose influences decisions. "Consolidating $15,000 across four maxed cards" gets warmer reception than "miscellaneous stuff I haven't figured out yet."

Funding timelines vary wildly: Online platforms like SoFi, Upstart, or LendingClub frequently wire money one to three business days after you e-sign documents. Traditional banks—Wells Fargo, Chase, Bank of America—often burn seven to fourteen business days between final approval and cash landing. Credit unions typically need three to seven days to move through their process. Need money by Friday for a Monday deadline? Online lenders usually smoke everyone else on pure speed, though comparing rates still matters more unless you're facing a genuine crisis.

Credit score reality check: Minimum requirements swing dramatically between lenders. Some accept scores down at 580, but they'll hammer you with 28% to 36% APR—barely better than credit cards. Want genuinely competitive pricing under 10%? You need 720 minimum. Scores between 640 and 719 typically land mid-tier rates around 12% to 20%. Drop below 640 and you're either facing premium rates or straight rejection.

Common Uses for Personal Loans

You can legally blow personal loan money on basically anything, but certain uses make way more financial sense than others.

Consolidating existing debt: This drives roughly 40% of all applications. Here's the real-world math: You're carrying $18,000 across three credit cards averaging 23%. Monthly minimums barely touch principal. You qualify for a four-year personal loan at 11.5%. Take the loan, nuke all three cards immediately, then make fixed monthly payments. You'll save approximately $6,800 in interest while shortening your debt-free date by multiple years. The fatal screw-up? Paying off cards, then gradually running them back up over 18 months. Now you've got the personal loan payment plus refreshed credit card debt. Only consolidate when you're simultaneously fixing whatever spending patterns created the mess originally.

Funding home repairs: Your HVAC completely dies—replacement costs $7,000. Kitchen renovations run $15,000 to $40,000. New roofing averages $12,000. Personal loans finance these faster than home equity products—no appraisal appointment, no closing costs eating 2% to 5% of borrowed amounts. The tradeoff: you'll pay 9% to 16% instead of the 6% to 9% typical for home equity loans. When does this exchange work? You need the work done immediately, you haven't built 20%+ equity yet, or you're planning to sell within a few years and don't want equity tied up in a HELOC you'll just pay off at closing anyway.

Covering medical expenses: Hospitals often pitch payment arrangements, but their "interest-free" deals contain landmines—miss paying the complete balance within 24 months and retroactive interest slams you at 18% to 22% calculated back to day one. Personal loans beat medical credit cards (CareCredit and similar products relying on deferred interest traps) and immediately stop collection agencies from harassing you. Before borrowing anything though, call hospital billing directly and negotiate. Many will slash total bills 20% to 40% for lump-sum payments or establish genuine zero-interest monthly plans if you just ask.

Major item purchases: Furniture sets, appliance packages, electronics—retailers aggressively push store financing. "90 days same as cash!" sounds amazing until you read fine print and discover missing the payoff deadline by even one day triggers 27% APR calculated retroactively from purchase date. When you're financing a purchase (though saving first always beats borrowing), a personal loan with transparent 12% fixed rate destroys the store card's deferred interest trap every time. That said, delaying the purchase six months to save cash instead beats both by eliminating all interest.

Emergency situations: Your transmission explodes three days before you absolutely must drive to a family emergency five states away. A burst hot water heater sends water cascading through your basement at 2 AM. These scenarios occasionally justify borrowing, and personal loans obliterate payday loans (averaging 400% APR) or title loans (averaging 300% APR) by massive margins. Real talk though: even a modest $1,000 emergency fund prevents most emergency borrowing. If you're grabbing a personal loan for an emergency, commit to building savings immediately after, even if that's only $50 per paycheck initially.

Author: Hannah Kingsley;

Source: nayiyojna.com

Personal Loan Repayment Structure

How your payments split between interest and principal determines both total cost and your eventual debt-free date.

Fixed monthly obligations: You'll owe identical amounts every month—could be $287, could be $433, whatever your loan terms specify. Early on, most of each payment covers interest with just a sliver reducing actual principal. As months pile up, this ratio gradually flips until you're paying mostly principal near the end. This amortization pattern means watching your balance decrease by only $180 despite making a $400 payment, which feels awful but reflects standard installment loan math.

Term length tradeoffs: Shorter repayment windows strain monthly budgets but dramatically slash total cost. Borrow $15,000 at 12% APR: A three-year term requires $498 monthly and generates $3,346 in total interest. Stretch that same loan to six years and your payment drops to $289—way easier on tight budgets—but total interest nearly doubles to $6,170. You're spending an extra $2,824 just for the convenience of smaller monthly bills. Choose the shortest term that doesn't force you to skip groceries or risk missed payments.

How interest piles up: Most lenders calculate simple interest accruing daily. Your outstanding principal generates fresh interest every 24 hours. Want to hack the system slightly? Split your monthly payment in half and send biweekly instead. Over a year, you'll make 26 half-payments (equivalent to 13 full payments rather than 12), cutting months off your repayment term and hundreds off total interest. This works because you're chipping away at principal faster, meaning less balance sitting there accumulating daily interest.

Prepayment rules and penalties: About 70% of current lenders permit prepayment without fees, but roughly 30% still include early payoff penalties—typically 2% to 5% of whatever you haven't repaid yet. This clause hides in loan agreement fine print. Before signing anything, search documents for "prepayment penalty" or ask the loan officer directly. Even without explicit penalties, some lenders use the Rule of 78s or similar front-loaded calculation methods that pack more interest into early payments, diminishing your savings from aggressive payoff strategies. Ask directly: "If I clear this loan in 18 months instead of 36, exactly how much will I save in total interest?"

Autopay rate discounts: Authorizing automatic withdrawals from checking typically shaves 0.25% to 0.50% off your rate. On a $20,000 loan, that's $75 to $150 annually—not life-changing, but it compounds over several years. Bonus advantage: you'll never miss a payment because you forgot or got slammed at work. Schedule autopay for two to three days after your regular paycheck deposits to dodge overdraft scenarios.

When a Personal Loan Makes Sense

Personal loans elegantly solve specific financial problems while creating expensive nightmares in other situations.

Author: Hannah Kingsley;

Source: nayiyojna.com

Strong credit unlocks actual value: Once your score crosses 700, you access rates competitive enough to rationally justify borrowing for planned expenses. That 7% to 13% APR range makes debt consolidation, home improvements, or emergency borrowing defensible. Below 700, especially under 640, rates spike so aggressively you're often better served exploring alternatives or investing a few months rebuilding credit before applying.

Beating your other options: Calculate actual numbers for your specific situation. Carrying $12,000 on cards averaging 24% APR? A 13% personal loan slashes your annual interest expense by roughly $1,320 while enforcing structured repayment instead of endless minimums. But when you own a home with available equity and qualify for a 6.5% home equity loan, choosing the 13% personal loan means unnecessarily overpaying. Run total cost comparisons across every available option—include origination fees, closing costs, and miscellaneous charges, not just headline rates.

Needing payment predictability: Fixed payments suit people who budget multiple months ahead. You know your December 2028 payment amount today. That certainty helps many borrowers psychologically more than the financial flexibility revolving credit provides. Credit card minimums can stretch repayment across 20+ years when you only pay minimums. Personal loans force completion within the original term.

Personal loans deliver the best value when borrowers lock in rates below 15% and maintain a realistic repayment plan fitting comfortably within their budget. Above 15%, you're typically better investing six months improving your credit profile, then refinancing or borrowing after your score climbs. The lone exception: consolidating existing debt charging 22% to 29%, where even a 17% personal loan represents substantial savings while you simultaneously work on credit repair

— Marcus Chen

Red-flag scenarios: Never grab a personal loan to patch cash flow problems—borrowing because you consistently run out of money before your next paycheck signals a budget crisis that additional debt will only worsen. Skip personal loans for wants instead of needs (vacations, entertainment purchases, luxury items) unless you're genuinely comfortable paying 10% to 20% premiums for immediate gratification. And when you're considering a personal loan to cover routine living expenses like rent or groceries, stop immediately—you need income solutions or serious spending adjustments, not more debt.

Personal Loan Costs and Comparison

The advertised rate reveals only part of the genuine cost picture, and comparing different loan types exposes important tradeoffs.

Rate ranges in 2026: Personal loan APRs span roughly 6% to 36%—a massive spectrum driven primarily by credit scores. Credit unions frequently deliver the lowest rates to members maintaining good standing, sometimes starting around 5.99% for members with excellent credit and existing deposit relationships. Online lenders cluster between 8% and 24% depending on applicant credit profiles. Traditional banks typically land somewhere in middle ground. Where you fall within any particular lender's range depends entirely on your credit score, documented income, and existing debt obligations.

Upfront origination charges: These fees reduce what actually deposits into your account. One lender advertises 10% APR but deducts a 5% origination fee. Another offers 11% APR with zero origination charges. Which costs less over the loan's complete life? You must calculate total dollars repaid, not simply compare headline rates. Some lenders add the origination fee to your loan balance rather than subtracting it from proceeds—now you're paying interest on the fee itself, which increases total cost even more substantially.

Late payment penalties: Most lenders assess $15 to $50 per late payment once grace periods of 10 to 15 days expire. The real financial damage happens at 30 days late—lenders report to all three credit bureaus, triggering score drops of 60 to 110 points that require months to recover. Those score hits increase your costs on future credit applications for years afterward.

Returned payment charges: Automatic payments that bounce due to insufficient funds generate $15 to $30 fees from lenders, plus separate overdraft penalties from your bank—frequently $35 or more. One unsuccessful payment can cost $50 to $65 across both institutions combined. Set up autopay timing carefully relative to when your paycheck deposits.

| Loan Product | APR Range | Repayment Period | Collateral Needed | Ideal Use Case |

| Personal Loans | 6%–36% | 2–7 years | Usually none | Consolidating expensive debt, funding planned major expenses, borrowers with solid-to-excellent credit who rent or recently purchased homes |

| Credit Cards | 16%–29% | Revolving (no set term) | None | Borrowing under 6 months, purchases you'll clear quickly, scenarios where rewards value exceeds interest costs |

| Home Equity Loans | 6%–12% | 5–30 years | Your residence | Large expenses exceeding $20,000, borrowers seeking lowest available rates, homeowners with 20%+ equity comfortable risking their property |

This breakdown shows why personal loans occupy middle ground. They cost more than home equity products but demand no collateral, making them accessible to renters and recent homebuyers without substantial equity. They beat credit cards for any borrowing extending beyond several months. Fixed terms enforce repayment discipline that revolving credit inherently lacks, but you sacrifice the flexibility to pay down balances and reborrow as changing needs dictate.

Frequently Asked Questions About Personal Loans

Personal loans deliver structured, predictable financing when applied to appropriate situations. They excel at consolidating expensive debt, funding necessary expenses your savings can't cover, or bridging short-term gaps with transparent repayment paths.

Before clicking "submit application," calculate your total cost including every fee and all interest charges across the complete loan life. Compare three to five lenders—mix online platforms, traditional banks, and credit unions—to surface genuinely competitive rates. Utilize pre-qualification tools to examine offers without triggering hard credit inquiries that ding your score.

Match your loan term to your actual budget capabilities, not your wishful thinking. Shorter terms demand higher monthly payments but save substantially on total interest paid. Longer terms ease immediate cash flow pressure but significantly increase total cost. Never finance something across a period exceeding its useful life—don't take a five-year loan for expenses you'll forget about within months.

Most critically, address the underlying financial patterns creating your borrowing needs. Build even a modest emergency fund—$50 monthly grows to $1,800 across three years. Monitor where your money actually goes for 30 consecutive days to identify wasteful spending. Explore income increases through side work, overtime opportunities, or career advancement. Personal loans solve immediate problems, but your daily financial habits determine long-term stability.

Treat personal loans as tools, not permanent solutions. Borrow deliberately, repay aggressively, and build the cash reserves that make future borrowing unnecessary.