Person reviewing unsecured loan options on a laptop with financial documents and calculator

What Is an Unsecured Loan and How Does It Work

Content

Borrowing money without putting up your house or car as backup might sound risky—for the lender, anyway. That's exactly what happens with an unsecured loan. These financial products don't require you to hand over your car title or put a lien on your property, but they come with their own set of trade-offs that every borrower should understand before signing on the dotted line.

Understanding Unsecured Loans

Think of an unsecured loan as the lender's vote of confidence in you. They're handing over cash based purely on your track record and promise to pay it back. No collateral changes hands. The unsecured loan meaning boils down to this: you're borrowing against your reputation and credit history rather than against physical property.

Here's what makes these loans different. With a mortgage, your house secures the debt—stop paying and the bank forecloses. With an auto loan, they repossess your car. Unsecured lenders? They can't just show up and take your stuff if you fall behind. They're out there flying without a safety net, which is exactly why they charge more in interest and scrutinize applications more carefully.

So why do banks and credit unions bother offering these higher-risk products? Simple economics. Plenty of people either don't own valuable assets yet or refuse to gamble their homes on a $15,000 loan. Young professionals, renters, and anyone who wants to keep their property off the table create massive demand. Lenders price in the risk through higher rates—sometimes double or triple what secured loans cost—and make it work.

Your financial snapshot matters intensely for these loans. Lenders dig into credit scores, job history, how much you already owe, and whether your income holds steady month to month. Someone with a 780 credit score and five years at the same company gets very different treatment than someone with a 620 score and three job changes in two years.

Author: Brandon Ellery;

Source: nayiyojna.com

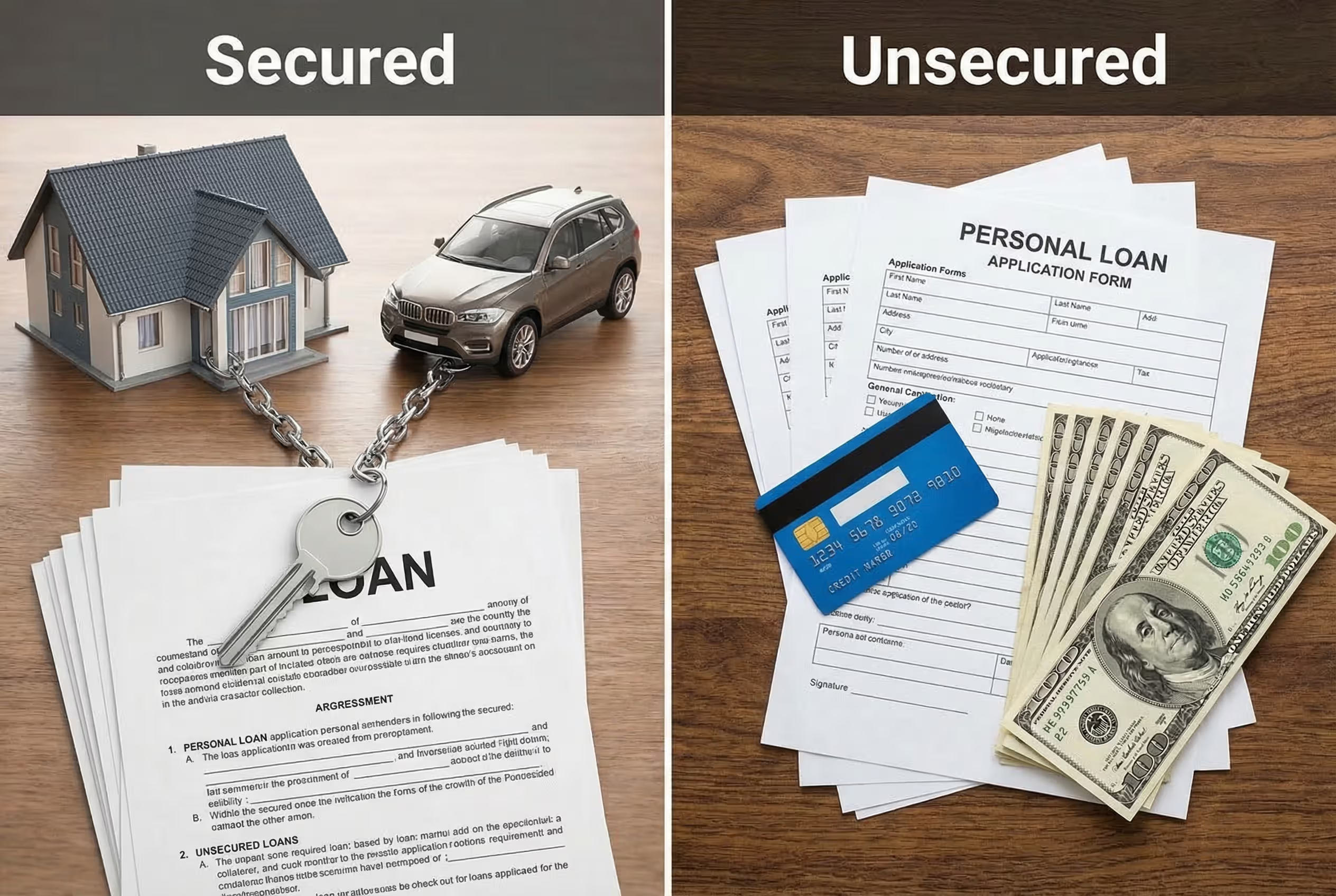

Secured vs Unsecured Loans: Key Differences

The gap between secured and unsecured borrowing runs deeper than just collateral. These two loan categories operate under completely different rules.

Secured loans mean you're pledging something valuable—your Honda Civic, your four-bedroom house, even your certificate of deposit at the credit union. Default on payments and the lender follows a well-established legal path to claim that asset. The secured vs unsecured loan difference shows up in almost every aspect of borrowing.

Check out how they stack up:

| Feature | Secured Loan | Unsecured Loan |

| Collateral Requirement | Must pledge specific property | Nothing required upfront |

| Interest Rates | Generally 3%–8% APR range | Typically runs 6%–36% APR |

| Approval Difficulty | Easier with collateral backing | Demands stronger credit profile |

| Loan Amounts | Frequently $10,000–$500,000+ | Usually capped around $1,000–$50,000 |

| Risk to Borrower | Losing whatever you pledged | Lawsuits, credit destruction, garnishments |

| Common Examples | Home mortgages, car financing, HELOCs | Credit cards, personal installment loans, most student loans |

Beyond what fits in a comparison chart, these loan types differ in timeline and process too. Secured loans often stretch across decades—think 30-year mortgages—while unsecured products rarely exceed seven years. Getting approved for a secured loan means appraisals, title searches, and property evaluations. Unsecured applications skip all that, which speeds things up considerably.

What happens when you can't pay? Secured lenders file repossession paperwork or foreclosure notices through relatively quick legal channels. Unsecured lenders must file lawsuits, win judgments, then chase you through wage garnishments or bank levies—expensive and uncertain, explaining why they demand premium interest rates.

When to Choose Each Type

Go secured when you're borrowing big money, want rock-bottom rates, and feel absolutely certain about your repayment ability. Mortgages and auto financing make perfect sense as secured products since you're buying the exact thing that backs the loan.

Pick unsecured when you need cash quickly, refuse to gamble your assets, or you're borrowing a smaller sum. Paying off medical bills, consolidating credit cards, or covering your sister's surprise wedding in Cabo—these situations fit unsecured personal loans nicely. You'll pay extra in interest, but your car stays yours even if things go sideways.

Here's a trap people fall into constantly: taking a home equity loan (secured) to wipe out credit card balances (unsecured) because the rate looks so much better. Sounds smart until you realize you just converted debt that couldn't touch your house into debt that absolutely can. If your spending habits haven't changed, you'll run those cards back up and now you're juggling both the equity loan and fresh credit card balances. Your house is on the line for what used to be just a credit score problem.

Author: Brandon Ellery;

Source: nayiyojna.com

Common Types of Unsecured Loans

Examples of unsecured loans show up all over your financial life, sometimes in obvious ways and sometimes hiding in plain sight.

Personal loans are the straightforward version. You get a chunk of cash—anywhere from $1,000 to $50,000 typically—and pay it back in equal monthly installments for two to seven years. People tap these for everything from debt consolidation to bathroom remodels to cross-country moves. In 2026, rates range from roughly 6% if your credit shines to 36% if it's battered and bruised.

Credit cards work as revolving unsecured credit lines. Your $10,000 limit lets you borrow, pay back, and borrow again without filling out new applications each time. Making minimum payments keeps you current, but carrying balances month after month means paying interest rates frequently above 20% APR. Convenience costs money.

Private student loans (different from federal programs) rarely require collateral. They fill gaps when federal aid doesn't cover full tuition costs. Since most college kids lack established credit, lenders usually demand a parent or relative co-sign. Rates swing wildly based on creditworthiness and whether you lock in fixed or variable rates.

Medical financing plans help patients afford procedures insurance won't touch. Dentists and plastic surgeons often partner with finance companies offering promotional deals—maybe 0% interest if you pay everything within 18 months. Miss that deadline by a day and deferred interest slams you for the entire original amount.

Signature loans are just personal loans with a different name, emphasizing that only your John Hancock backs the debt. Credit unions love this term for smaller loans to existing members.

Payday alternative loans from federal credit unions deliver $200–$1,000 at rates capped at 28% APR—far better than predatory payday lenders charging 400% APR. These help members cover short-term cash crunches without falling into debt traps.

Author: Brandon Ellery;

Source: nayiyojna.com

How Lenders Evaluate Unsecured Loan Applications

Understanding how unsecured loans work means peeking behind the approval curtain. Without property to claim if things go wrong, lenders become extremely picky about who gets approved.

Credit scores dominate the decision. Most lenders draw hard lines—you'll need at least 580 to 600 just to get considered, while accessing competitive rates requires 700 or higher. Your score condenses your entire credit history into three digits: payment patterns, how much you owe, how long you've had credit, recent applications, and account variety. Score 760 or above? You'll see the best rates available. Below 640? Prepare for limited choices and painful interest rates.

Income confirmation proves you actually earn enough to cover the payment. Lenders want recent pay stubs, last year's tax returns, or several months of bank statements showing deposits. Run your own business? Expect extra scrutiny since self-employment income bounces around. Most lenders prefer seeing at least six months at your current job, ideally two years in the same industry.

Your debt-to-income ratio compares what you already owe monthly against what you earn monthly before taxes. Below 36% looks great; above 43% raises serious questions. Say you bring home $5,000 monthly before taxes but already send $2,000 to existing debts—that 40% DTI limits how much new debt lenders approve. Some cap DTI at 40% for unsecured products, others stretch to 50% for exceptionally qualified applicants.

Job stability signals reliable income. Hopping between employers every eight months concerns lenders. Conversely, a decade with one company or steady career progression suggests you're a safe bet.

Approval timelines typically run one to seven business days. Online lenders often deliver instant soft-pull pre-approvals that don't ding your credit. Full approval needs hard credit inquiries and document verification. Some fintech companies now fund same-day while traditional banks might take a full week.

Lenders also check your banking behavior through ChexSystems or Early Warning Services. A history of overdrafts, bounced checks, or accounts closed for negative balances can tank your application even with a decent credit score.

Author: Brandon Ellery;

Source: nayiyojna.com

Interest Rates and Costs of Unsecured Borrowing

Unsecured borrowing costs more than secured borrowing for one simple reason: lenders eat bigger losses when borrowers bail. No collateral to grab and auction off means unsecured lenders must write off entire balances or spend thousands chasing you through courts—rarely recovering much either way.

Current APRs for unsecured personal loans in 2026 span about 6% to 36%. Where you land in that range depends on your credit score, income, amount borrowed, and repayment term. Excellent credit (750+) might snag 6%–10% rates. Fair credit (640–699) typically sees 15%–24%. Below 640? Expect rates pushing that 36% ceiling many states enforce.

Credit cards charge even more—often 18%–28% APR on purchases. Cash advances frequently exceed 29%, and penalty APRs for late payments can hit 29.99%. Store-branded cards sometimes charge north of 30% APR.

Interest tells only part of the cost story. Watch for these fees:

Origination fees ranging from 1%–8% get subtracted from what you receive or added to what you owe. Borrow $10,000 with a 5% origination fee? You'll get $9,500 deposited but owe the full $10,000.

Late payment penalties typically hit $25–$50 each time. Repeated lateness also triggers penalty rates and trashes your credit score.

Prepayment penalties occasionally pop up, charging you for paying off early. Lenders lose anticipated interest income when you prepay, so some claw it back through these penalties. Always verify before signing.

Application fees are rarer in 2026 but still appear with sketchy subprime lenders. Legitimate lenders almost never charge upfront before approval.

NSF fees strike when your automatic payment bounces—usually $15–$35 per occurrence.

The annual percentage rate (APR) rolls interest plus most fees into one number for honest comparisons. A loan advertising 10% interest with a 5% origination fee might actually carry a 12% APR over three years.

Risks and Drawbacks of Unsecured Loans

The risks of unsecured borrowing stretch beyond expensive interest rates. Knowing these dangers helps you dodge common mistakes.

Credit score destruction happens fast when payments slip. Just one payment 30 days late can crater your score by 60–110 points depending where you started. Multiple late payments, charge-offs, or collection accounts inflict severe, long-lasting damage that hampers your financial options for years.

The debt spiral starts when borrowers use unsecured loans to patch other debts without fixing spending habits. You consolidate $15,000 in credit card debt with a personal loan, then run those cards right back up. Now you're stuck with the personal loan payment plus new credit card balances—dramatically worse than your starting point.

Collection escalation begins when you stop paying. After 90–180 days of silence, lenders typically charge off your account and dump it to collection agencies for pennies on the dollar. Collectors can sue, win judgments, and garnish up to 25% of your take-home pay or freeze your bank accounts. Some states even let them slap liens on homes despite the loan being unsecured originally.

Bankruptcy implications change with unsecured debt. While these debts often get discharged in bankruptcy, the process annihilates your credit for 7–10 years and costs thousands in legal fees and emotional turmoil.

Opportunity cost hurts too. High-interest unsecured debt devours money that could build emergency savings, fund retirement accounts, or make investments. A $10,000 loan at 20% APR bleeds roughly $3,300 in interest over three years—money that could've grown in investments instead.

Relationship destruction occurs when co-signers enter the picture. Your default becomes their nightmare, wrecking their credit and potentially triggering lawsuits against them. Co-signing unsecured loans for friends or relatives frequently destroys relationships when repayment falls apart.

Skip unsecured loans when you're already drowning in debt, your job feels shaky, or you lack a concrete repayment plan. They're terrible choices for discretionary spending you can't really afford—vacations, luxury items, or lifestyle inflation beyond your actual income.

The biggest mistake I see borrowers make with unsecured loans is treating them like free money. Just because you're approved doesn't mean you should borrow. Calculate the total interest cost over the loan's life, not just the monthly payment. If that number shocks you, you're probably borrowing too much or paying too much in interest. A good rule of thumb: if the loan doesn't either save you money, make you money, or prevent a genuine emergency from becoming a disaster, reconsider whether you really need it

— Jennifer Martinez

Frequently Asked Questions About Unsecured Loans

Unsecured loans deliver financial flexibility when you need funds without gambling specific assets. They work best for borrowers with solid credit needing moderate amounts for purposes improving their financial situation—consolidating expensive debt, covering legitimate emergencies, or making investments generating returns exceeding loan costs.

Skipping collateral requirements creates both advantages and risks. You won't lose your car or house directly through default, but credit destruction, collection lawsuits, and potential garnishments create serious consequences affecting your financial life for years. Higher interest rates mean these loans cost substantially more than secured alternatives, making careful comparison shopping essential.

Before applying, calculate total interest costs over the loan's entire life, not just monthly payments. Verify you can comfortably afford payments even if income dips slightly or expenses jump. Check your credit score and shop multiple lenders finding competitive rates. Read fine print for origination fees, prepayment penalties, and other costs affecting true expense.

Unsecured loans serve legitimate purposes in consumer finance, but they demand financial discipline and honest assessment of repayment ability. Used wisely, they solve genuine financial challenges. Used carelessly, they create debt burdens compounding existing problems. Your circumstances, credit profile, and repayment capacity should guide whether an unsecured loan makes sense for your situation.